Macro Extremes (week ending July 19, 2024)

July 21, 2024 Leave a comment

A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) either registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

* denotes multiple week inclusion

Extremes above the Mean (at least 2.5 standard deviations)

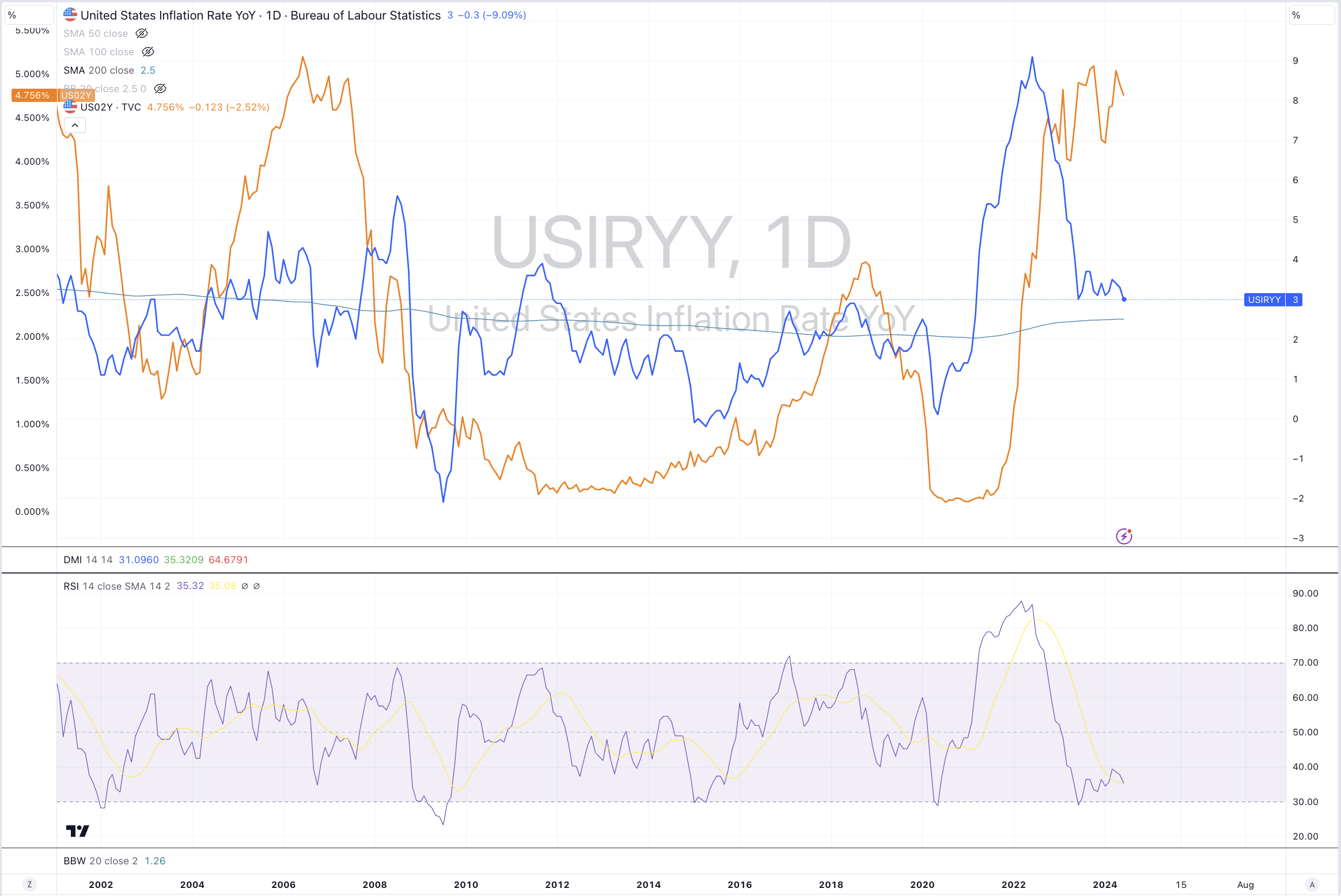

U.S. 10 year minus U.S. 2 year government bond yield spread *

U.S. 10 year minus U.S. 5 year government bond yield spread *

U.S. 30 year minus U.S. 10 year government bond yield spread *

GBP/EUR

GBP/USD *

KBW Bank Index

DJ Industrials *

S&P Small Cap 600 Index

Russell 2000 *

KRE Regional Bank Index *

S&P MidCap 400 Index

Nasdaq Biotechnology Index *

Toronto’s TSX

Israel’s Tel Aviv 35 index

And Australia’s ASX 200

Overbought (RSI > 70)

Russian 10 year government bond yields *

Robusta Coffee *

Hungary’s BUX *

Pakistan’s KSE *

NIFTY *

SENSEX *

And Turkiye’s BIST 100 *

The Overbought Quinella (Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

None

Extremes below the Mean (at least 2.5 standard deviations)

British 2 year government bond yield

New Zealand and Swedish 10 year government bond yield

CAD/GBP *

CAD/EUR

Oversold (RSI < 30)

Cotton

North European Hot Rolled Coil Steel *

U.S. Midwest Hot Rolled Coil Steel *

Lumber *

Lithium Hydroxide *

Corn *

BRL/USD

And the Chinese RMB *

The Oversold Quinella (Both Oversold and Traded at < 2.5 standard deviations below the weekly mean)

Soybeans *

Notes & Ideas:

Government bond yields were mixed.

Most of the European yields fell while yields in the America’s rose…..and many of them took a break from their fortnightly trends.

Except for the Belgium, Danish and Finnish 10’s.

The Australian 10 year minus U.S. 10 year bond yield spread broke its 5 consecutive weeks of advance.

And the Chilean 2’s are in a 5 week winning streak.

Equities were mostly lower.

The prominent risers for the week were U.S. banks, U.S. Transports and U.S. small and mid caps.

Last week’s edition alerted readers to the outside bullish outside reversal week performed by the Dow Jones Transports and Nasdaq Transports Indices. They rose impressively this past week.

The rotation from large caps into the smaller and mid cap companies continued.

China’s CSI 300 has risen 3% over the past fortnight.

While Indonesia’s IDX 30 has a 5 week winning streak intact and Philippine’s PSE has climbed for 4 straight weeks.

Indonesia’s main index has climbed 10% over the past 5 weeks and the U.S. KRE Regional Banks index has risen 20% over the same time.

And the DAX broke its 4 week winning streak.

Commodities continued its bias for lower prices.

Hogs, Lumber and oats were amongst the few winners.

Lean Hogs climbed 6%, nearly halving the 15% decline seen over the previous 13 weeks.

The losers were much more widespread, with Aluminium, Copper, Coking Coal, Oil, Gases, Grains, the PGM’s and Nickel.

Cocoa, Tin, Silver also joined the notable declining brigade.

Cotton is back in oversold territory.

Natural Gas has posted a 34% loss during the previous 5 weeks.

Heating Oil has fallen 7% in the past fortnight.

Aluminium has sunk 14% over the past 8 weeks.

Soybeans have declined for 7 of the past 8 weeks.

And Lithium Hydroxide has now spent 53 consecutive weeks in weekly oversold territory.

Currencies continue to provide action, again and again.

The Aussie and the Loonie were both weaker

The anomaly was the CAD rising against the AUD and breaking 5 consecutive weeks of declines.

Inversely, it broke its 5 week winning streak against the USD.

Some CAD pairs appear in this week’s list of extremes.

The AUD broke its 4 week rising streak against all, except versus the Kiwi.

And the British Pound continues to hold up.

The larger advancers over the past week comprised of;

Lean Hogs 6.3%, Lumber 3.2%, LNG in Yen 3.1%, Newcastle Coal 2.7%, Oats 2.4%, CSI 300 1.9%, KBW Banks 3.3%, Budapest 1%, DJ Transports 1.7%, S&P SmallCap 600 2.2%, Russell 2000 1.9%, KRE Regional Banks 7.5%, PSE 2.2% and the Nasdaq Transports rose 2.7%.

The group of largest decliners from the week included;

Australian Coking Coal (2.4%), Aluminium (5.2%), Bloomberg Commodity Index (3.2%), Baltic Dry Index (4.8%), Cocoa (7.6%), China Coking Coal (4.4%), WTI Crude Oil (2.7%), Copper (7.8%), Heating Oil (3.4%), Coffee (4.2%), Lithium (2.4%), Tin (8%), Natural Gas (8.6%), Nickel (3%), Orange Juice (3.7%), Palladium (7.2%), Platinum (3.9%), Gasoline (3%), Robusta Coffee (1.9%), Sugar (2.8%), SPGSCI (2.9%), Brent Crude Oil (2.8%), Gasoil (3.1%), Uranium (2.4%), Silver in AUD (3.7%), Silver in USD (5%), Corn (2.9%), Rice (2.7%), Soybeans (2.8%), All Developed World ex USA (2.1%), AEX 4%, DAX (3.1%), HSCEI (5.6%), Hang Seng (4.8%), IBEX (1.5%), Nasdaq Composite (3.7%), KOSPI (2.2%), Mexico (2.3%), Nasdaq 100 (4%), Nikkei 225 (2.8%), Copenhagen (2.9%), Helsinki (2.4%), Stockholm (2.3%), South Africa (2.4%), SOX (8.8%), S&P 500 (2%), Straits Times (1.4%), TAEIX (4.4%) and the S&P Materials Index fell 2.2%.

July 21, 2024

by Rob Zdravevski