In the near-term, I think that the decline in U.S. bond yields should take a little pause.

They are now trading 2.5 standard deviations below their rolling 20 week moving average.

This will be mentioned in this week’s edition of my Macro Extremes newsletter.

In the April 19, 2024 edition of Macro Extremes, the U.S. 20 year bond yield appeared in the overbought extreme list and inversely, the iShares 20+ year treasury bond ETF (TLT) was in the oversold category.

The mid point for trading in the TLT around the last 2 weeks of April 2024 was ~ $88.46.

This week, the TLT is trading at 2.5 standard deviations above its 20 week moving average.

This week’s mid point price is $97.92.

Over the past 4 months……………that represents a capital return of 10.7% and when adding $1.22 per share of dividends received, the total return is a handsome 12%.

Who said bonds are boring.

Over the mid-term, I think bond yields will continue to fall.

Here are the 10 notable moments over the past 50 years when the U.S. 10 year bond yield had entered Monthly overbought territory while also being at a certain percentage above its 50 month moving average and also trading up to 2 standard deviations above its rolling monthly mean.

And today many are still betting that yields rise (and bond prices fall)…..

British 10 year government bond yields are seldom this distance above its 200 week moving average while simultaneously registering a weekly overbought reading.

Forgetting Bank of England policy rate setting, I can see these 10’s back down around 2.40% over the coming 9-15 months.

Demand destruction commensurate with decline in GDP will aide this thesis.

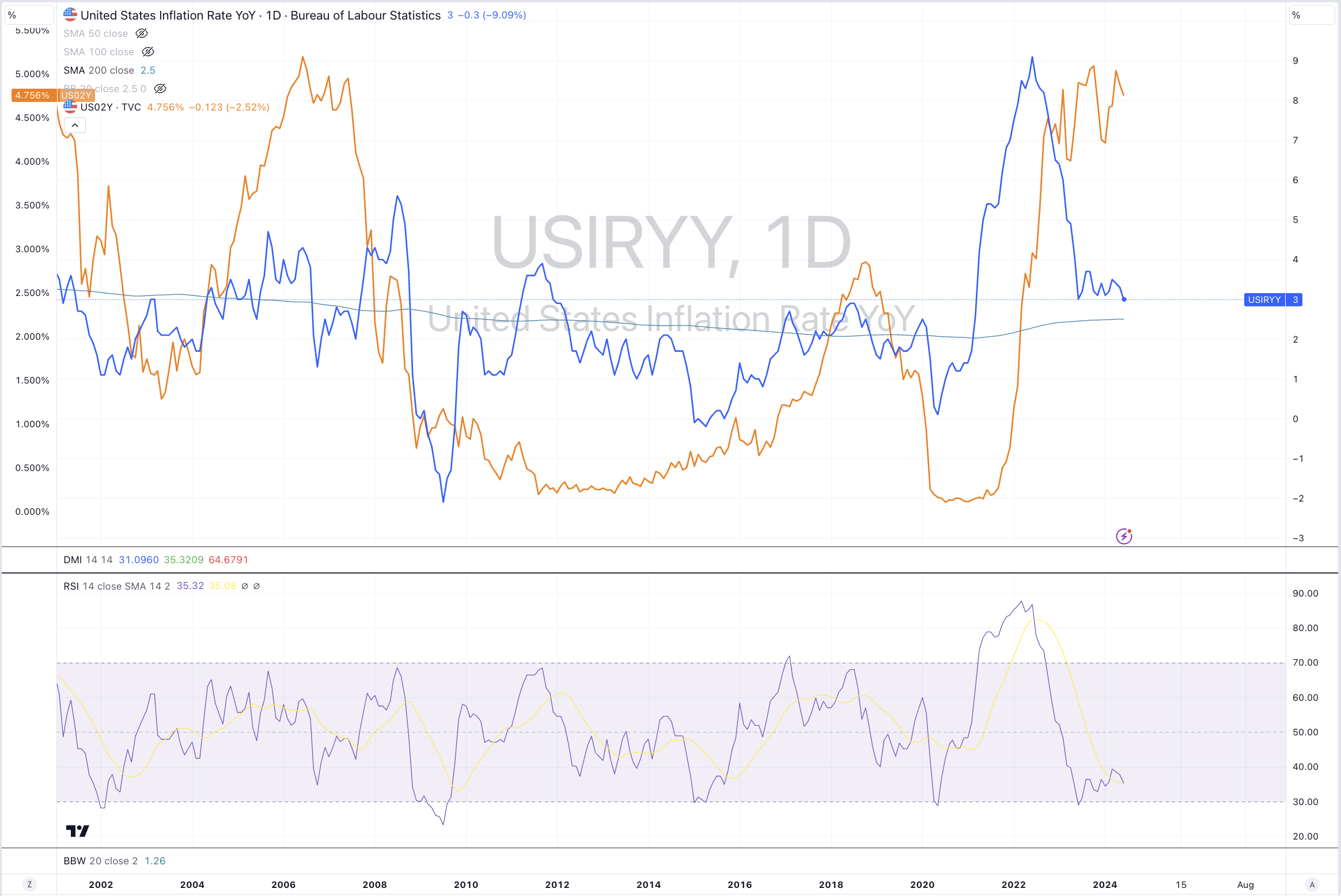

In this note on March 16, 2023 (March 15, U.S. time), I suggested that shorter-term interest rates would start to rise when the Copper/Gold Ratio trades 2.5 standard deviations below its weekly mean and implies a poor moment of timing for those buying bonds.