Mean reversion doesn’t apply to NVIDIA

September 25, 2024 Leave a comment

NVIDIA is miles above its 200 week moving average.

September 25, 2024

Trying to hear what's not being said

September 25, 2024 Leave a comment

NVIDIA is miles above its 200 week moving average.

September 25, 2024

September 22, 2024 Leave a comment

A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) either registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

* denotes multiple week inclusion

Extremes above the Mean (at least 2.5 standard deviations)

Palladium

Sugar

AUD/CAD

ZAR/USD

IBEX

Copenhagen

PSE

Nasdaq Transportation Index

Thailand’s SET Index *

And Australia’s ASX 200

Overbought (RSI > 70)

U.S. 10 year minus U.S. 2 year government yield

U.S. 10 year minus U.S. 5 year government yield

Arabica and Robusta Coffee *

Gold as priced in AUD, CAD, EUR & USD *

MYR/USD *

NIFTY *

SENSEX *

And the ASX Financials Index *

The Overbought Quinella (Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Singapore’s Strait Times Index

Extremes below the Mean (at least 2.5 standard deviations)

None

Oversold (RSI < 30)

U.S. 2 year government bond yield *

Australian Coking Coal *

U.S. Midwest Hot Rolled Coil Steel *

North European Hot Rolled Coil Steel *

Lithium Carbonate *

Lithium Hydroxide *

CFR China Iron Ore *

USD/CNH

USD/IDR

USD/SGD *

Shanghai Composite *

The Oversold Quinella (Both Oversold and Traded at < 2.5 standard deviations below the weekly mean)

U.S. 3 month bill yield

Notes & Ideas:

During a week when the investors were awaiting a lowering of the American central bank interest rates…….. Global government bond yields rose.

Chilean and Swiss 10’s yields aren’t oversold anymore.

Short dated Japanese yields bucked the global weekly trend. They fell.

The U.S. yield curve remains overbought (10 year – 2 year) as is the U.S. 10Y – 5Y spread.

The U.S. 5 year minus 5 year breakeven inflation rate is nearing an oversold extreme.

And incidentally, Brazil’s central bank hiked their policy interest rate.

Equities rose again.

We are seeing more indices entering overbought territory.

At this stage, most of them are in Asia driven by their stronger currencies.

Singapore’s Strait Times is in a 6 week winning streak.

Some Australian indices also feature in this week’s list.

The Shanghai Composite and CSI 300 broke their 4 week losing streaks.

And any of those which were oversold last week have bounced, such as the KOSPI.

Commodities mostly rose.

Gold and Palladium remain in overbought territory.

Sugar soared 19% for the week.

Lumber and Heating Oil moved out of overbought territory.

U.S. Henry Hub Natural Gas has risen 14% over the past 3 weeks.

Wheat broke its 3 week winning streak.

U.S.Midwest Hot Rolled Coil Steel has spent 17 weeks being oversold.

And Lithium Hydroxide has now spent 62 consecutive weeks in weekly oversold territory.

Currencies feature heavily in this week’s entrants of extremes.

The Aussie rose while the Canadian Loonie fell, again. Confusing perhaps?

The decline in the CAD juxtaposed the risk-on feeling for the week.

While the Yen’s decline of 2%-3% across a range of pairs and weakness in the Swissie confirmed the ‘risk-on’ mood.

The USD was generally weaker and is prominently oversold against various Asian currencies.

And the British Pound is nearing an overbought level again the USD.

The larger advancers over the past week comprised of;

Bloomberg Commodity Index 2.1%, Baltic Dry Index 4.6%, WTI Crude Oil 5.3%, Cotton 5.3%, Lean Hogs 4.8%, Copper 2.5%, Heating Oil 3.5%, Lumber 2.3%, Cattle 2.5%, LNG JKM in Yen 4.4%, Newcastle Coal 2.9%, Natural Gas 5.6%, Nickel 4.1%, Gasoline 5.3%, Sugar 19.2%, S&P GSCI 2.8%, CRB Index 3.1%, Brent Crude 3.6%, Gasoil 2.5%, Gold in CHF 1.8%, Gold in USD 1.7%, Rice 1.9%, KBW Bank Index 4.7%, DJ Industrials 1.6%, HSCEI 5.1%, Hang Seng 5.1%, IBEX 1.9%, IDX 1.6%, S&P Small Cap 600 2.3%, MOEX 3.9%, Russell 2000 2.2%, TAEIX 1.8%, Nasdaq Composite 1.5%, KSE 3.5%, S&P MidCap 400 2%, Nikkei 225 3.1%, Stockholm 2.1%, PSI 3.3%, South Africa 2%, Sensex 2%, SET 1.9%, S&P 500 1.4%, STI 1.7%, ASX Financials 2.4%, ASX Small Caps 1.8% and Turkiye’s BIST rose 2.2%.

The group of largest decliners from the week included;

JKM LNG (2.7%), Arabica Coffee (3.4%), Platinum (2.5%), Robusta Coffee (4%), Dutch TTG Gas (3.4%), Corn (2.8%), Oats (2.7%), Wheat (4.4%), BOVESPA (2.8%), Copenhagen (2.6%) and the Tel Aviv 35 fell 2.8%

September 22, 2024

by Rob Zdravevski

September 19, 2024 Leave a comment

Last week WTI Crude #Oil traded down to $64.04.

I’ve been calling $64 for sometime as its first stop.

While its downtrend needs to be respected for now, it is not yet exhibiting the required strength to send it lower.

No action for now.

Pause and Watching before I call $46.

September 19, 2024

by Rob Zdravevski

rob@karriasset.com.au

September 19, 2024 Leave a comment

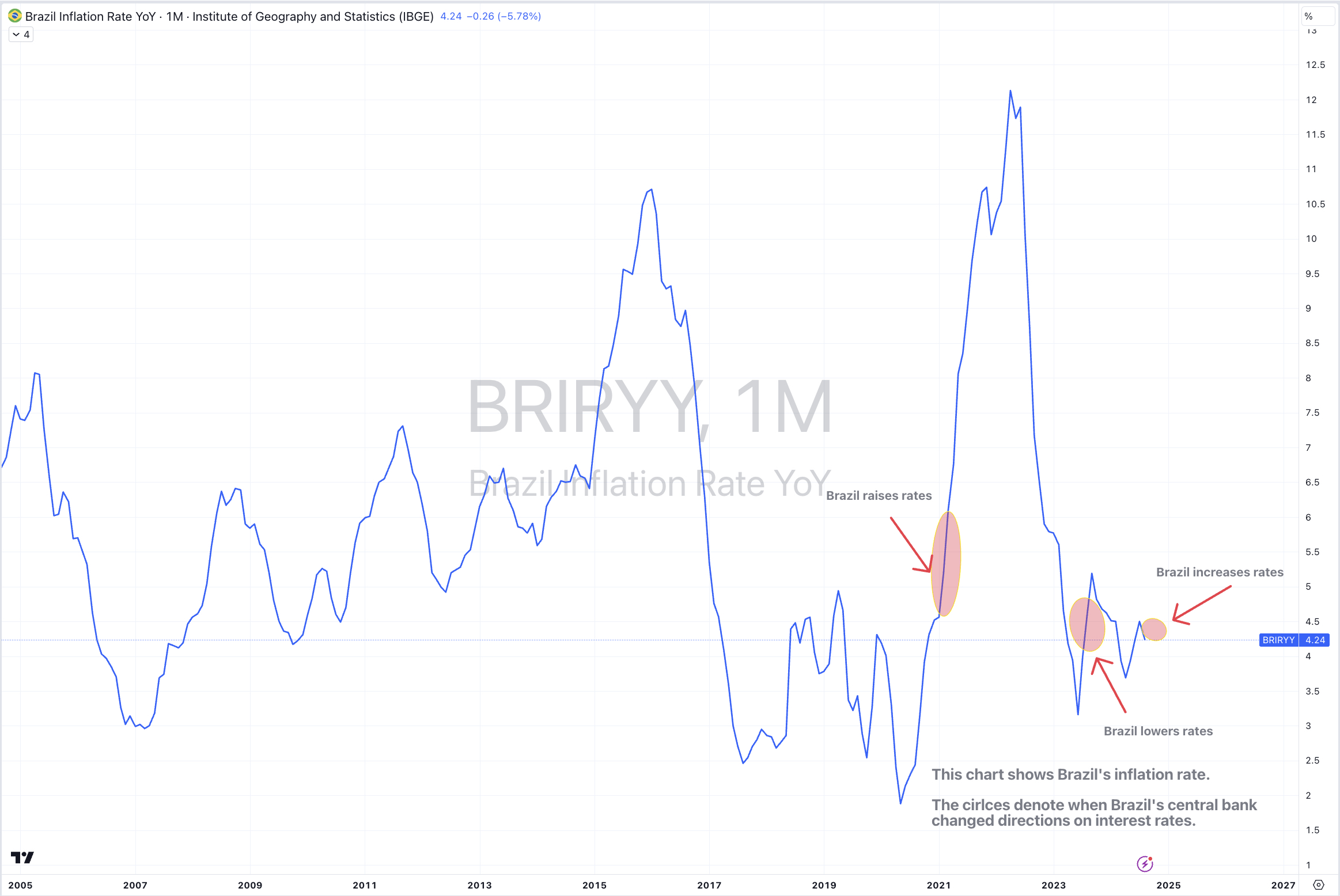

#Brazil (and #Chile‘s) central banks see #inflation before the rest of them.

Today, Brazil’s central bank raised interest rates.

They changed direction.

Forget what the U.S. is doing.

It pays to queue off their moves.

The circles in the chart below denotes when Brazil’s central bank

changed interest rates direction compared to where the Brazil’s inflation rate was, at the time.

September 19, 2024

by Rob Zdravevski

rob@karriasset.com.au

September 18, 2024 Leave a comment

As wage rates in China increase, more of its labour intensive manufacturing have shifted to Indonesia, Mexico and Vietnam.

When that happens, other parts of its manufacturing sector advance up the value chain mainly as its technology processes improve.

For example, China has overtaken Japan as the world’s largest exporter of automobiles.

Keep in mind that China still has a working population of nearly 1 billion.

That is 3 times larger than the combined working population of Indonesia, Mexico and Vietnam.

September 18, 2024 Leave a comment

I read somewhere that the average age of U.S. commercial buildings are approximately over 50 years old.

and according to Joint Center of Housing Studies of Harvard University;

in 2021, that the median American home age was 43 years. It has never been older.

That average was 27 years old in 1991.

#construction #remodelling

September 16, 2024 Leave a comment

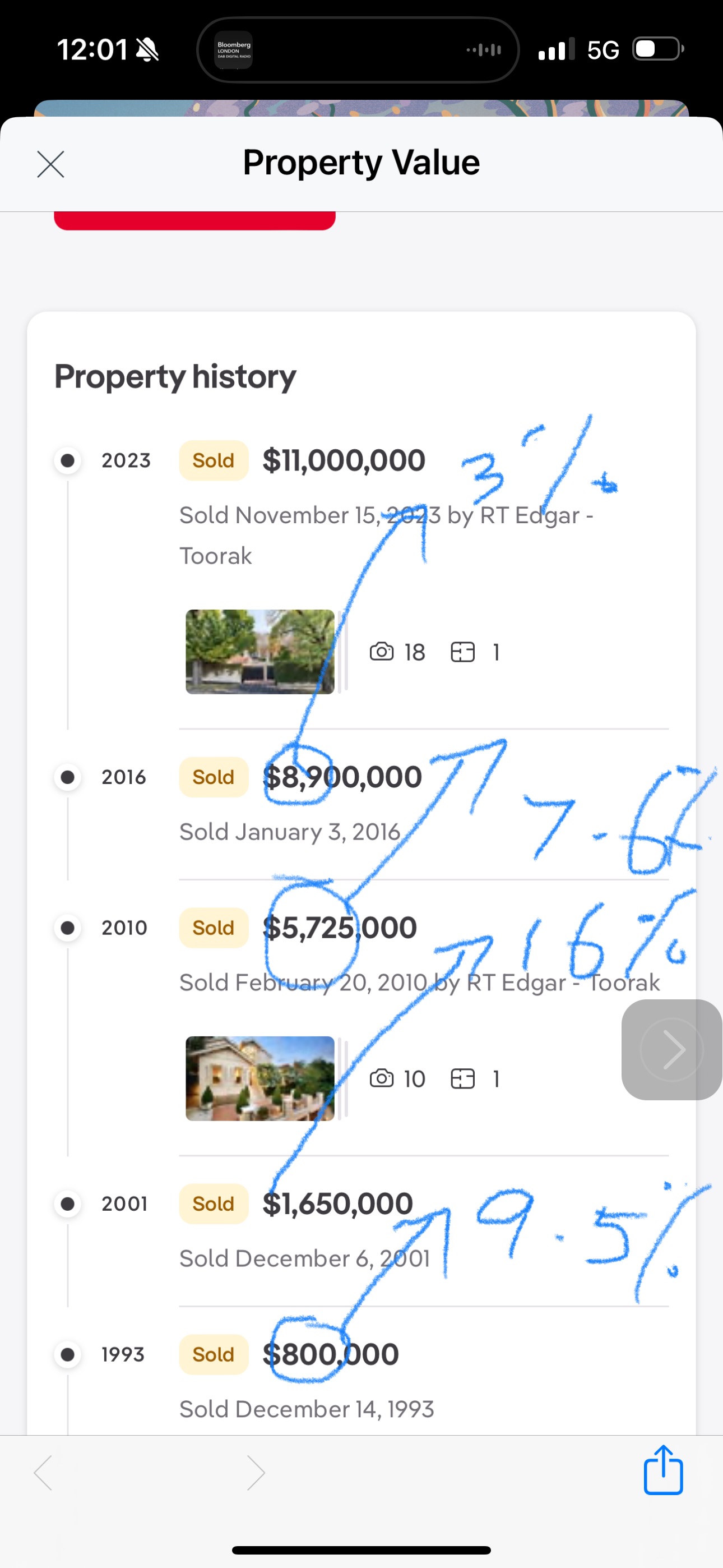

I was recently asked my view about real estate valuations.

My response was wasn’t brief and it had many variables.

Today, I walked past a house in South Yarra (which is a really nice inner-city suburb in Melbourne, Australia) which caught my eye.

Then I looked up the specific property’s transaction history.

Over 30 years, the gross annual compounded return for this property has been 9% (without any considerations made for any financing, maintenance or carrying costs) that the various owners may have incurred.

And this gross 9% p.a. capital return is from a property in a seriously fancy street, in a sought after suburb within one of the world’s most hottest real estate markets over that time.

My scribbles below are showing the gross annual compounded return achieved from each transaction to the other.

There is nothing like doing the numbers….

September 15, 2024 Leave a comment

A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) either registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

* denotes multiple week inclusion

Extremes above the Mean (at least 2.5 standard deviations)

Palladium

Thailand’s SET Index *

Singapore’s Strait Times

Overbought (RSI > 70)

SHY *

U.S. 10 year minus U.S. 2 year government yield

MYR/USD *

Arabica & Robusta Coffee *

Gold as priced in AUD, CAD and USD

NIFTY

SENSEX

ASX Financials Index *

And the ASX Industrials Index

The Overbought Quinella (Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Gold in EUR

Extremes below the Mean (at least 2.5 standard deviations)

WTI Crude Oil

Gasoline

S&P GSCI Index

Brent Crude Oil

Gasoil

KOSPI

Oversold (RSI < 30)

U.S. and German 2 year government bond yield

Australian Coking Coal *

U.S. Midwest Hot Rolled Coil Steel *

Lumber

Lithium Carbonate *

Lithium Hydroxide *

CFR China Iron Ore *

AUD/THB *

USD/THB

USD/SGD

Shanghai Composite

CSI 300

MOEX

The Oversold Quinella (Both Oversold and Traded at < 2.5 standard deviations below the weekly mean)

U.S. 3 month t-bill yield *

Swiss and Chilean 10 year government bond yield

North European Hot Rolled Coil Steel *

Heating Oil *

Notes & Ideas:

Global government bond yields fell, again, adding to the previous weeks decline.

Belgian, Brazilian and Finnish yields did the opposite.

The yield for the U.S. 10 year yields are at their lowest since May 2023.

While the U.S. yield curve is overbought.

U.S. 5 year minus 5 year breakeven inflation rate is nearing an oversold extreme.

And Chile’s and Switzerland’s 10 year bond yield are oversold.

Equities had a tremendous week, recovering last week’s declines.

For example, the Nasdaq Composite recovered all of last weeks loss.

The Shanghai Composite and CSI 300 are in 4 week losing streaks.

South Korea’s KOSPI is unloved.

Russia’s MOEX broke its 7 week losing streak.

The SOX soared 10% to nearly offset last weeks 12% tanking.

Singapore’s Strait Times is in a 5 week winning streak.

And some Indian and Aussie indices are overbought.

Commodities mostly rose.

Gold returns to overbought territory.

Silver rose 10% while Palladium double that performance for the week.

The latter appears in this weeks list.

Other notable advancers included Cocoa, Oats, Wheat, Aluminium and Coffee.

Coffee is overbought again.

Wheat has risen 12% over the past 3 weeks.

Inversely, selected energy contracts are oversold.

Gasoline declines to complete a mean reversion.

U.S.Midwest Hot Rolled Coil Steel has spent 16 weeks being oversold.

And Lithium Hydroxide has now spent 61 consecutive weeks in weekly oversold territory.

Currencies set the mood for risk.

The Aussie rose while the Canadian Loonie fell.

The decline in the CAD juxtaposed the risk-on feeling for the week.

Adding to the mixed signals, we saw the Yen advance while risk assets prospered.

MXN/USD rallied 4% for the week and isn’t oversold anymore.

The USD is oversold agains the roaring Baht, Ringgit and Singapore Dollar.

And the Indonesian Rupiah broke its 6 weeks rising streak against the USD.

The larger advancers over the past week comprised of;

Australian Coking Coal 3.4%, Aluminium 5.4%, Bloomberg Commodity Index 2.6%, Cocoa 8.7%, WTI Crude Oil 1.5%, Cotton 2.9%, Copper 4%, Arabica Coffee 9.9%, Tin 3%, Palladium 19.2%, Gasoline 1.6%, Robusta Coffee 10.4%, Sugar 1.8%, S&P GSCI 1.6%, CRB Index 2.6%, Silver in AUD 9.4%, Silver in USD 10%, Gold in AUD 2.7%, Gold in CAD 3.3%, Gold in CHF 4%, Gold in GBP 3.3%, Gold in EUR 3.4%, Gold in USD 3.2%, Gold in ZAR 2.7%, Corn 1.7%, Oats 7%, Wheat 4.9%, AEX 2.3%, CAC 1.5%, DAX 2.2%, DJ Industrials 2.6%, DJ Transports 2%, IBEX 3.3%, IDX 1.7%, S&P SmallCap 600 3.5%, Russell 2000 4.3%, TAEIX 1.5%, Nasdaq Composite 6%, KRE Regional Banks 1.8%, FTSE 250 2%, S&P MidCap 400 3.3%, Mexico 1.8%, Nasdaq Biotechs 4.2%, Nasdaq 100 5.9%, Nifty 2%, Oslo 1.6%, Copenhagen 4.3%, Stockholm 1.8%, Sensex 2.1%, SOX 10%, S&P 500 4%, Chile 1.7%, STI 3.1%, TSX 3.5%, ASX 200 1.1%, ASX Materials 4.2% and ASX Small Caps rose 3.1%

The group of largest decliners from the week included;

Baltic Dry Index (2.6%), European Hot Rolled Coil Steel (2.1%), Lumber (2.2%), Newcastle Coal (4.5%), Dutch TTF Gas (2.3%), Urea Middle East (1.9%), CSI 300 and Shanghai Composite (2.2%), China A50 (1.8%), Egypt (1.7%) and Vietnam fell 1.8%

September 15, 2024

by Rob Zdravevski

September 14, 2024 Leave a comment

RBOB Gasoline prices have converged to its 200 week moving average.

It’s been a while since it has danced around there.

It is also closing in registering a weekly oversold reading.

That was last seen 4 years ago.

September 14, 2024

September 9, 2024 Leave a comment

My monthly newsletter has been published.

The link below is to enjoy, read, share and subscribe