Macro Extremes (week ending June 19, 2026)

June 21, 2026 Leave a comment

A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) either registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

n.b. pricing of (commodity) futures contracts is only considering the immediate front month.

* denotes multiple week inclusion

Extremes above the Mean (at least 2.5 standard deviations)

U.S 3-month bill yield

COP/USD

XBI biotech ETF

Overbought (RSI > 70)

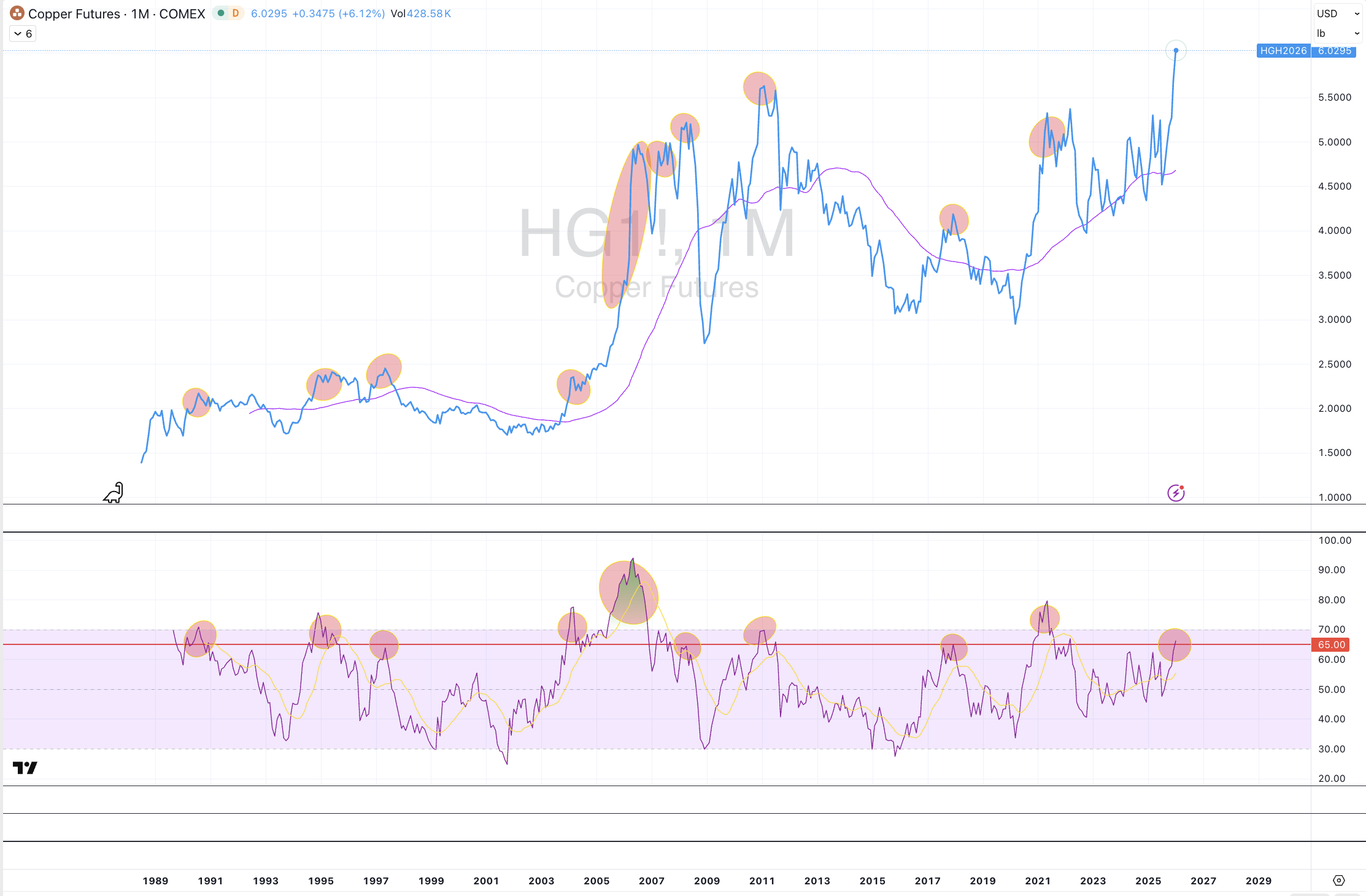

Copper/Gold Ratio

Russian 10-year government bond yields *

Rubber *

AUD/CHF

USD/IDR

Austria’s ATX Index *

Italy’s MIB *

Spain’s IBEX

Taiwan’s TAIEX *

South Korea’s KOSPI *

Nasdaq 100

Nikkei 225 *

SOX *

And Poland’s WIG Index *

The Overbought Quinella (Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

U.S. 5-year bond yield minus U.S. 5-year breakeven inflation rate

Singapore’s Strait Times

Extremes below the Mean (at least 2.5 standard deviations)

U.S. 5-year breakeven inflation rate

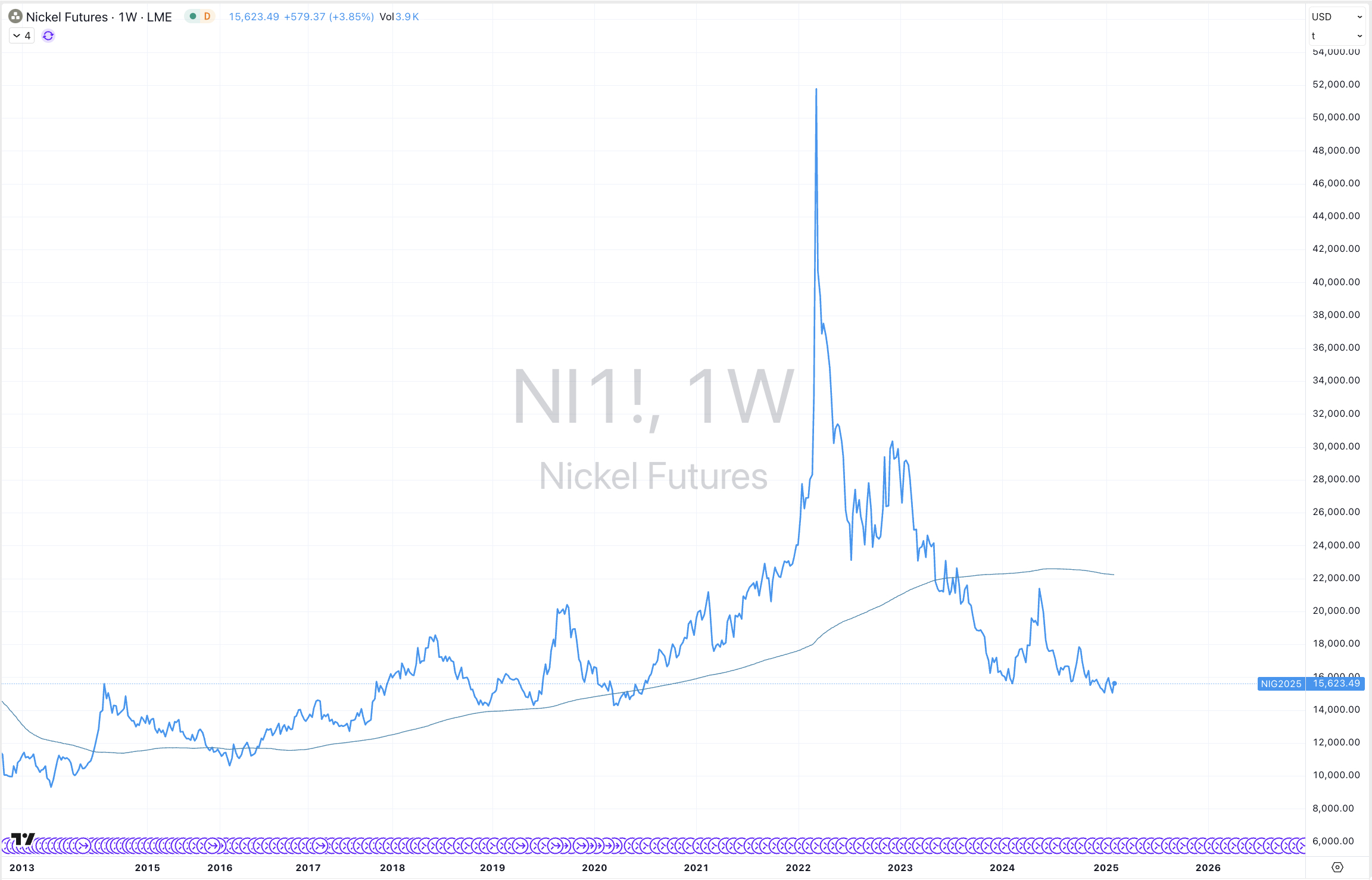

Nickel

Corn *

CAD/USD

MYR/USD *

HSCEI Index

Hang Seng Index *

Oversold (RSI < 30)

U.S. 10-year bond yield minus U.S. inflation rate *

North European Hot Rolled Coil Steel *

Lean Hogs *

CHF/AUD

Russia MOEX Index

The Oversold Quinella (Both Oversold and Traded at < 2.5 standard deviations below the weekly mean)

U.S. 10-year minus U.S. 2-year bond yield spread

U.S. 10-year minus U.S. 5-year bond yield spread

Notes & Ideas:

Government bond yields were mixed and quiet.

India’s & Türkiye’s 10-year bond yield along with the U.S. 10-year inflation breakeven rate have declined for 4 weeks.

Chile’s 2-year bond yield has sunken for 6 weeks.

The U.S. 5-year inflation breakeven rates have fallen for 5 weeks.

Various inflation breakeven spreads appear in this week’s list.

Russia’s 10-year bond yield has climbed for 8 weeks.

And Japan’s 30-year yields rose to break 4 weeks of decline.

Equities were mostly higher.

A few indices swapped spots with those that departed.

Dubai’s DFM Index is in a 4-week winning streak.

CAC has risen for 5 weeks.

Indonesia’s IDX has risen 10% in 2 weeks.

Vietnan’s VN Index rose and broke its 4-week losing streak.

The Hang Seng has fallen for 6 weeks.

The Dow Jones Transports rose and snapped a 4-week winning streak.

And Thailand’s SET fell and broke its 7-week winning streak.

Commodities had a bias for weakness, again.

Cocoa, Coffee, Cocoa and Wheat were the notable gainers.

Coal, Oil, Gases, Distillates, Silver, Platinum and Urea were amongst the decliners.

Brent Crude has sunk 14% in the past fortnight.

Lumber has risen for 4 weeks.

Bloomberg Commodity Index, S&P GSCI, CRB Index and Lean Hogs have fallen for 5 weeks.

Cotton rose and snapped a 5-week losing streak.

Iron Ore rose and broke 6 weeks of consecutive decline.

Gold priced in AUD and ZAR have declined for 6 weeks.

Platinum and Middel Eastern Urea prices have declined for 7 weeks.

And U.S. Gulf Urea prices are in a 9-week losing streak.

Currencies were quiet, again.

The Aussie rose except against the IDR and INR.

Those latter pairs have eased from their recent overbought status.

The Loonie and Swissie were weaker, again.

COP/USD has risen for 5 weeks.

A few more currency pairs left the extreme list

Yen was mixed.

And the USD was firmer, again.

The larger advancers over the past week comprised of;

Aluminium 2.8%, Cocoa 9.5%, Cotton 4.3%, Palm Oil 3%, Arabica Coffee 5.7%, Lumber 1.5%, Cattle 2.3%, Dutch TTF Gas 3.8%, Oats 2.4%, Wheat 3.2%, Shanghai Composite 1.5%, CSI 300 3.4%, All World Developed ex USA 1.5%, ATX 4.3%, IDX 2.8%, DFM 3.5%, EGX 3.6%, FCATC 7.2%, MIB 2.6%, IBB 1.8%, IBEX 3.1%, Dublin 2.2%, TAIEX 5.2%, Nasdaq Composite 2.4%, KLSE 1.7%, KSE 3.8%, KOSPI 11.4%, Nasdaq 100 2.6%, Nikkei 225 7.9%, Nifty 1.7%, Stockholm 2.1%, PSE 3.8%, Sensex 1.7%, SOX 7.3%, STI 3.3%, SX5E 1.7%, Vietnam 1.8%, XBI 5.2%, ASX Financials 1.7%, ASX Small Caps 2.6% and Türkiye’s BIST rose 5.7%.

The group of largest decliners for the week included;

Richards Bay Coal (3.6%), Rotterdam Coal (3.7%), Bloomberg Commodity Index (1.9%), Brent Crude (7.8%), Baltic Dry Index (3.4%), Lean Hogs (2.6%), JKM LNG (14.8%), JKM in Yen (16.9%), Lithium Carbonate and Hydroxide (1.7%), Newcastle Coal (4.3%), Nickel (2.3%), Orange Juice (2.9%), Palladium (1.9%), Platinum (2.3%), S&P GSCI (3.8%), CRB Index (1.8%), Urea U.S. Gulf (3.7%), Gasoil (6.4%), Urea Middle East (8.8%), Silver (4.7%), Gold in USD (1.5%), DJ Transports (4.2%), HSCEI (4.8%), Hang Seng (3.2%), BOVESPA (1.6%), KRE (2.3%), OBX (2.2%), Helsinki (1.6%), TA35 (4.6%) and the Nasdaq Transports fell 1.7%.

June 21, 2026

By Rob Zdravevski

rob@karriasset.com.au