I heard of import tariffs but not export tariffs

Is exporting inflation, China’s new ‘weapon’?

Maybe this is part of China’s net zero emission plan?

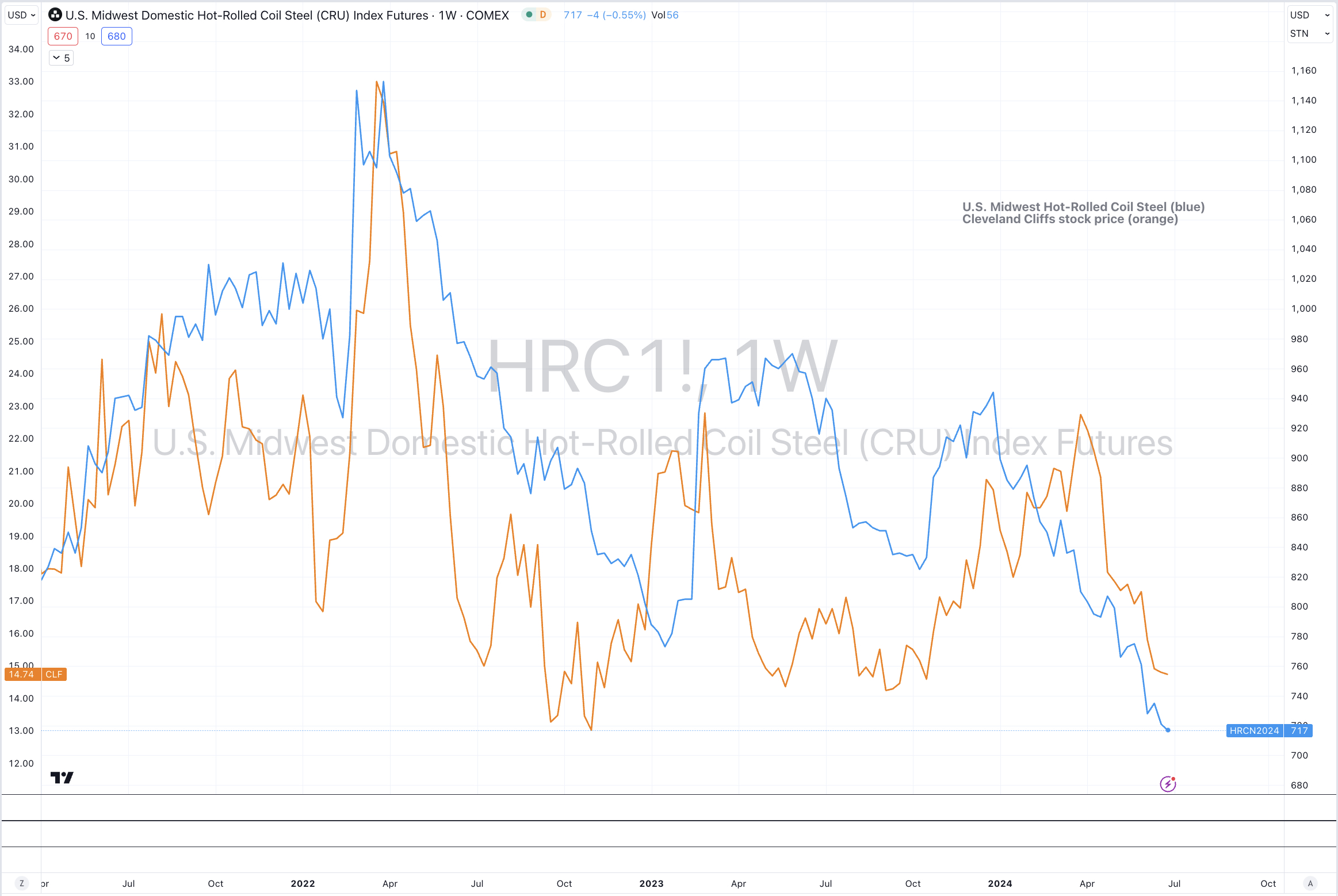

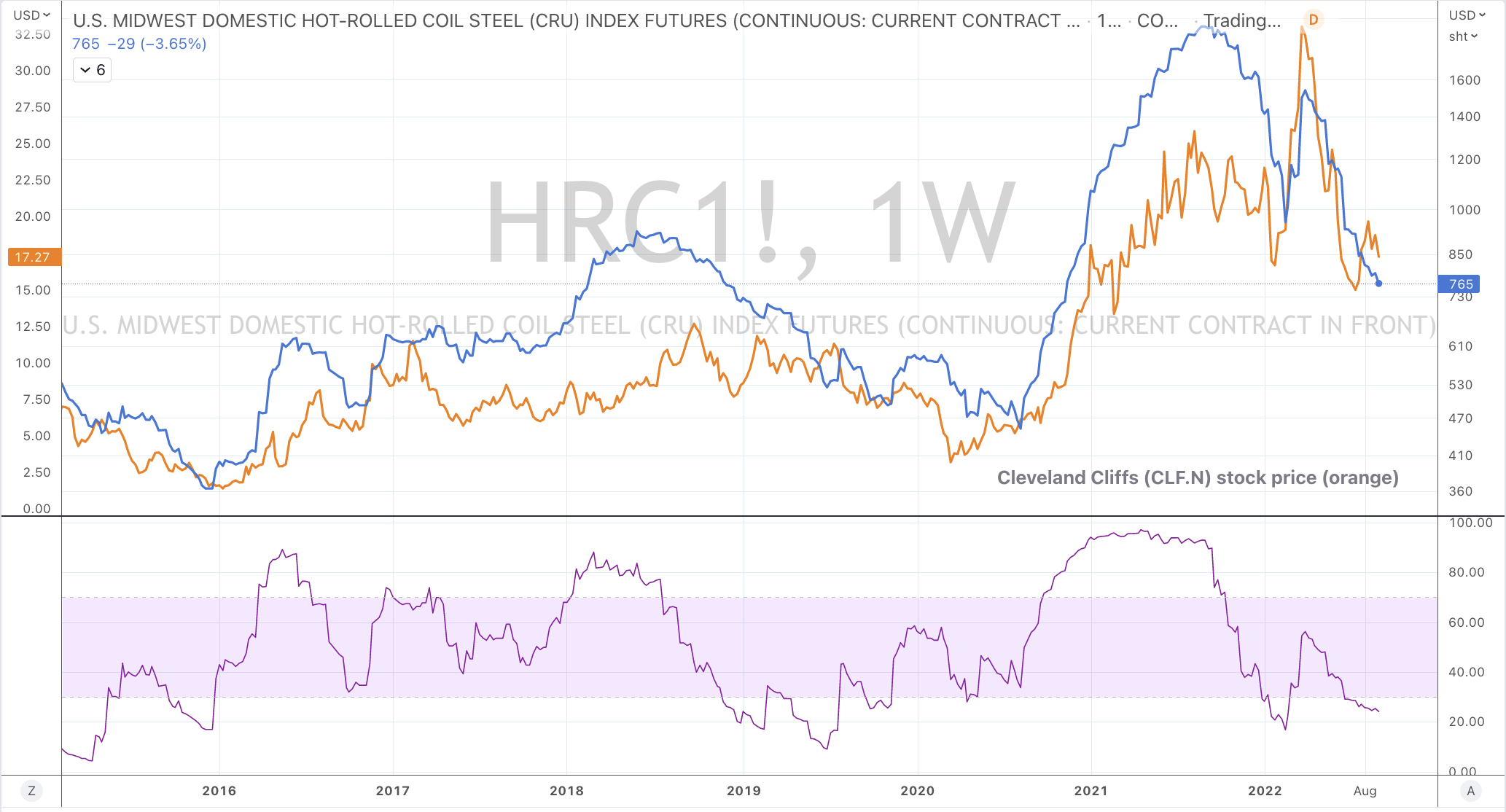

Would you like to know why HRC (hot rolled coil steel) prices have quadrupled in the past year?

The world’s largest steel producing nation has been imposing and increasing tariffs on its own steel exports.

I’ll repeat, Chinese companies are required to pay a tariff in order to export their product.

High purity Pig Iron exports attract a 20% tariff while Ferrochrome stands at 40%.

Furthermore, China has removed export tax rebates for 23 steel products including flat and rolled steel)

This is quite incredible.

It is quite normal for nations to impose a tariff on goods being imported onto their shores and limit ‘product dumping’ but to ‘discourage’ your own corporations from global competition and profits is an extraordinary tactic.

In 2020, total world crude steel production was 1877.5 million tonnes (Mt). The biggest steel producing country is currently China, which accounted for 57% of world steel production in 2020.

The next 6 countries (regions) account for a combined 28.4%.

They are:

#1 EU 7.4%

#2 India 5.3%

#3 Japan 4.4%

#4 U.S. 3.9%

#5 Russia 3.8%

#6 South Korea 3.6%

.

.

.

.

#29 Australia 0.3%

Australia’s annual steel production is 5.5Mt, ranking behind the production of Bangladesh, Austria, Malaysia and Belgium.

One-third of Australia’s steel needs (nearly 2Mt) are imported, with most it coming from China. The rest is supplied by local manufacturers such as Bluescope Steel.

So, the news becomes even more alarming when the amount of steel imported from China has fallen by 50% in the past several months.

Can you see how half of 2Mt is a pittance of China’s 1,065Mt worth of annual production yet it has a pronounced effect on Australian business.

But what is China export tariff strategy telling us?

Firstly, China is ‘ring-fencing’ some its industrial production perhaps its seen as a form of ’nationalism’ but more so, I see it as securing or better yet, retaining its supply for its own consumption.

This could also be a measure of protectionism, but this is not new because western economies already do it themselves.

When you have a powerful (and enviable) position such global ‘market share’, you can withhold supply, causing localised prices to rise, thus hurting industry and consumers in far away locales.

Whilst imposing tariffs of steel exports will accentuate output gaps in all those other nations and higher prices may remain, by sacrificing some capitalist profits, this may be one aspect how China will reduce its carbon emissions…….

Have a think about that notion?

In addition, after decades of the global juxtaposition of China exporting deflation (and many enjoying lower prices), China may be now “exporting” inflation.

It may be the definition of being ‘careful what you wish for’.

With its own currency testing multi-year highs (helping put a lid on its own inflation rate), could China’s new export to the world actually become Stagflation?

Don’t forget to subscribe to my blog to receive other notes, the moment they are published or equally feel free to email with a question or comment.

Until next time,

Warm Regards,

Rob Zdravevski

rob@karriasset.com.au