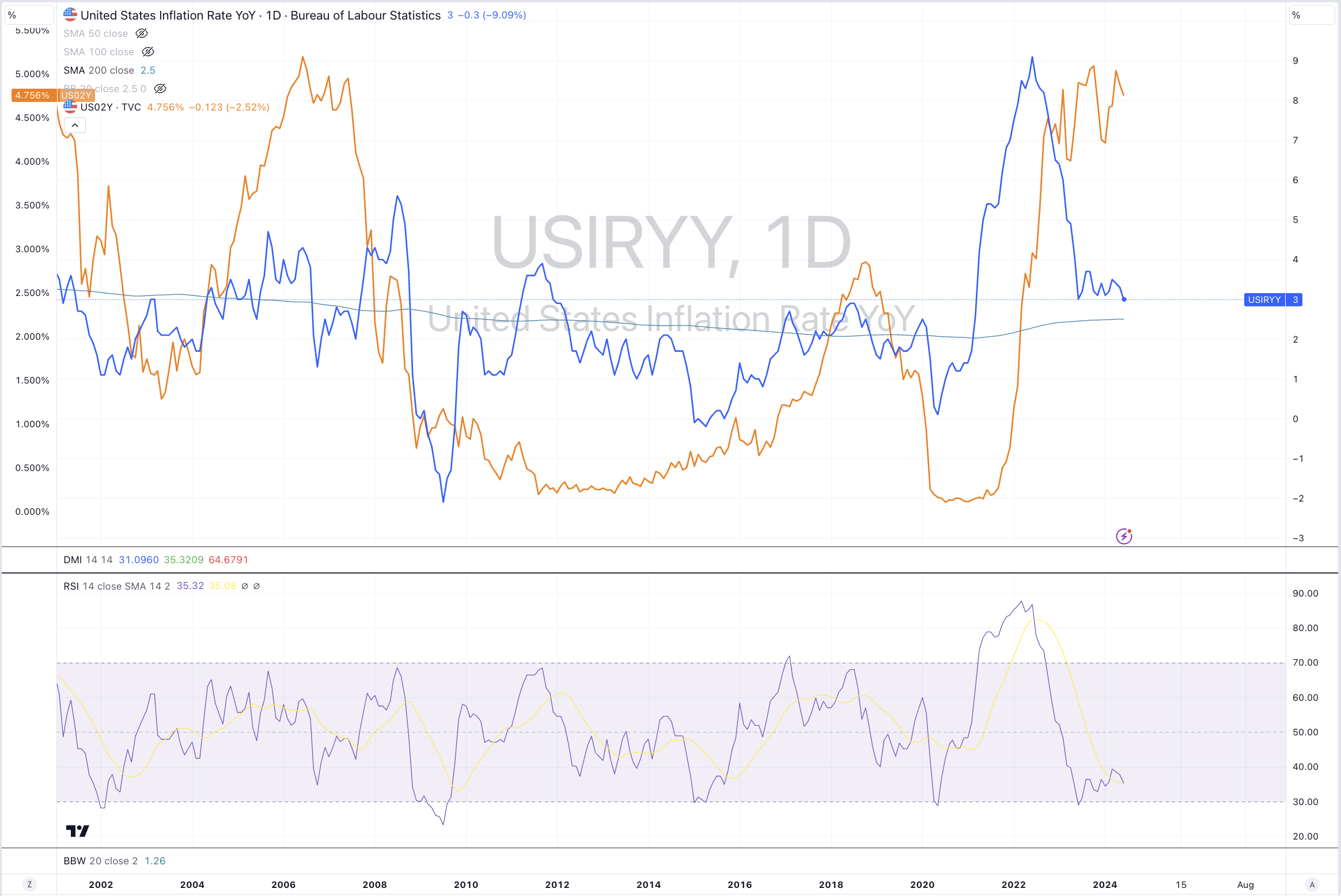

Broadly, interest rates (2 year government bond yields) are now between 20% and 25% below their peaks and are trading at levels last seen 18-24 months ago.

I think it’s near time for many to re-finance their debt.

From here on in, those companies still carrying much debt, better be seen to pay lower interest expenses over the coming years.

I would like a reduction in interest rate please……

even though the world’s stockmarkets have risen between 25% and 50% over the past 3 years……

Following such wonderful investment returns, why are equity investors are so hinged on whether central banks will lower their interest rate policy or target?

This wish from ‘collective’ equity investors is most perverse.

What is the genesis and motivation behind this story-telling derived by the strategists and pundits from the investment houses?

Something must not be working well enough for ‘them’ when money is priced at 5.25%.

Are companies and individuals still too leveraged?

Perhaps corporate profits are still under pressure even following the rounds of jobs cuts and cost-cutting measures?

Or maybe, banks can’t make enough of a spread between the interest they need to pay on deposits and the amount they can loan out?

I’d argue that a fair cost of money is around 5%-6%.

And rate cuts are often used to flog a dead horse back into life……

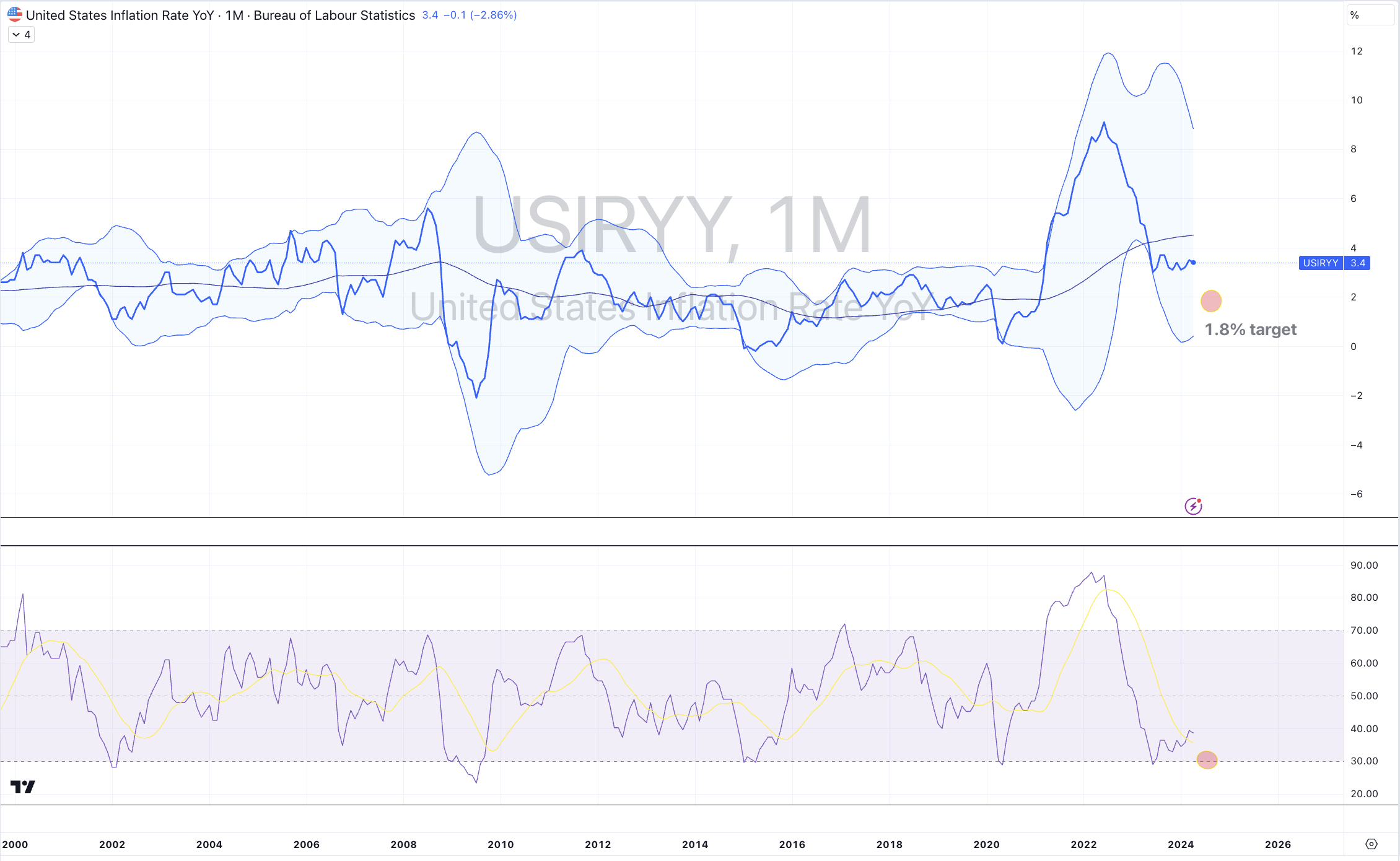

I keep reiterating that what is more important about where interest rates have traded up to isn’t about the nominal rate, but rather the quantum or factor which the nominal rate have risen by.

Yes, the numbers look bigger when rates are rising from 0.5%…..but people, households, companies, governments etc etc don’t necessarily temper their borrowing when rates are low…..We tend to become accustomed to the ‘going rate’.

In general, the piggies are always at the trough.

When a family is seeking a mortgage of $600,000 but their credit provider announces the good news that they have been approved for $680,000, I suspect that they accept all of the $680,000. After all, they can use it for the landscaping etc etc.

We are happy to continue taking as much we can get or is available.

If my mobile phone plan allows for 20GB of data, I’m sure I’ll use it up and then ask for an upgrade to 40GB. Soon after, I’ll be requesting for an upgrade to 60GB of data.

When the Australian cash rates were 0.25% in last 2020, I was asked if I thought the Reserve Bank of Australia would cut rates at the next meeting.

My response was, “who cares”. The questioners were often shocked by my seeming flippancy.

At this point, I would add by asking, “How much debt do you have and how pressure are you under, that you need a further 15 or 25 basis points of relief”.

Today, if your cost of borrowing has risen from 3% to 6% and you are now speculating whether interest rates go up a further 1% receives the same response from me with the difference being, are you still carrying so much debt that you may ‘break’.

Is it the Fed that is possibly going to ‘break something’ or have we simply kept taking on more debt?

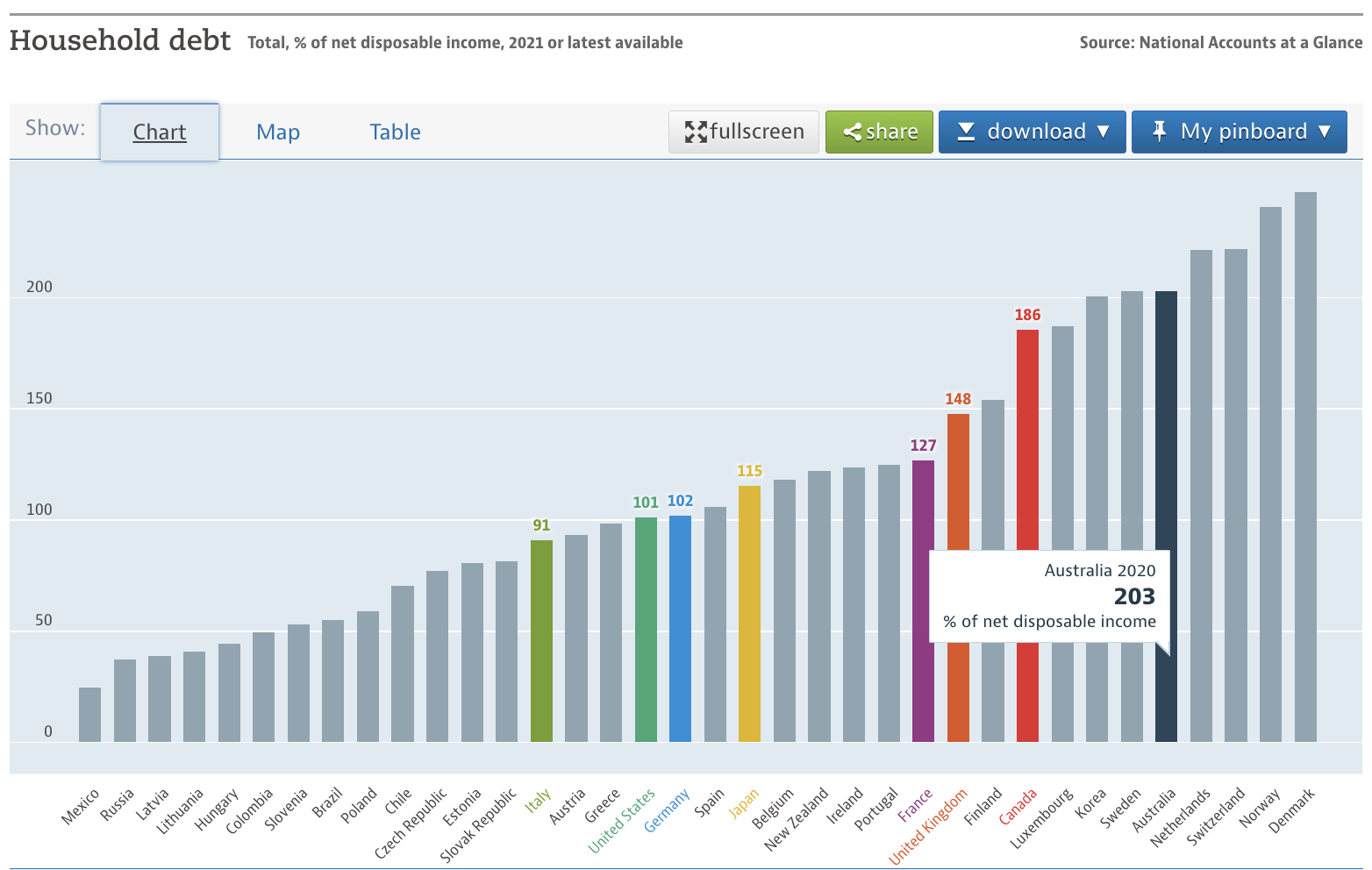

In the graphics below, you can see where the citizens of various nations sit in the indebted stakes.

Look at those frugal and financial responsible Latvians and Hungarians.

Household Debt as % of net disposable income source: OECD

Let me get back to the illustrating the ‘factor’ of the rise.

When rates went from 6% to 8%, it was only a 33% increase.

When rates went from 8% to 16%, it was ONLY a 50% increase.

Mortgage rates in Australia have nearly doubled. In the U.S., they have easily doubled.

The U.S. 2 years Treasury Bond yield has risen 10 fold.

When your interest repayments or the total cost of capital increase by such a factor, it is the quantum of the rise from the previous levels where you were comfortable with, that hurts the most.

My studies show that government bond yields have never risen by factors of 3 or 4 from their lows within any credit cycle.

At these extremes, as the chart within the below shows, the 2 year bond yield is miles above its 200 week moving average.

Why doesn’t mean reversion matter now, when it has many times prior?

Expecting rates to go higher and challenge gravity, probability and mathematics is a very foolish and crowded trade.

This is not about calling doom and whether the Fed ‘breaks something’……but rather it’s about thinking independently and reading the market tape as it is.

Behind the talk of where rates go to, sits speculative or investing opportunity.

If you have a view….then make the trade and take a position.

Those who shorted bonds when rates were 1% have made a fortune.

Today, if you think rates go up noticeably more……enough to tempt you into a trade, then short bonds and ride the expectation of whether the Fed keeps hiking rates to a point where ’they break something’.

If you think interest rates will fall, you could buy bonds.

Although, this is not a binary choice and the bond market may not be your natural business.

You can express you trade idea in many different manners.

For example, if interest rates keep rising, then you could short the equity of heavily indebted companies or technology stocks which aren’t profitable and have negative free cash flow, or

If you think rates are going to decline, then perhaps owing shares in high growth companies may see their prices ‘catch a bid’.

Of course, this is not personal advice and it’s important to do your research and analysis.

I don’t know why people make it so difficult for themselves.

The bond market is ‘more correct’ than the rhetoric or ‘tough talk’ that central bankers provide.

The former isn’t emotional while the latter is and susceptible to biases.

The U.S. 2 year bond yield started rising and forecasting higher interest rates in October 2021, when it passed the 0.30% level.

By the time the Federal Reserve announced its first rate hike on March 17th, 2022, the U.S. 2 year bond yield was 2.20%

I think it is a waste of time speculating or debating if the Fed will ‘pivot’ and change direction.

Firstly, a reversal of current direction is not an automatic occurrence. The Fed can keep rates where they are for a little more.

Secondly and more importantly, the bond market will tell you more.

Currently, 2 year bonds are yielding 4.15%.

Much is priced in and now poised at stretched levels.

The chart below shows the Fed raising rates by a factor of 12 from the 0.25% low.

This is in belated sync with the 11 to 13 fold hikes seen in many other economies while those commodity sensitive nations (where the citizens are least indebted compared to those in the G10) such as Brazil, Chile and Mexico all started hiking rates (trying to fight inflation) between March 2021 and June 2021.

The most crowded trade, thesis and belief is still – for higher rates.

Not many are calling lower rates.

I am.

For various reasons, I think this U.S. 2 year bond yield falls back to the 2.30%-2.60% range in the coming 10-20 months.

Does this mean that the Fed cuts rates into the next year?

Perhaps, Yes. Maybe taking the Fed Funds Rate to 2.75%

But I can’t see how they can raise rates another 1% with out ‘breaking something’.

In the April 15, 2022 edition of Macro Extremes, I noted that until that moment, the U.S. 10 year bond yield had never registered an Overbought reading on a Monthly basis…….and it stayed there for the past few months.

Furthermore, it coincided with the yield trading up to 2.5 standard deviations above its monthly rolling mean.

The chart below shows circles and boxes when it has hit both 2.5 and 3 standard deviations.

Why the reprise of this topic?

I don’t believe Jerome Powell’s 2022 Jackson Hole declaration that the Fed will earnestly raise rates higher will actually happen.

I won’t bother speculating whether rates are raised once or twice as 2022 comes to a close but I think Mr Powell is now trying to increase the rhetoric and use as much media messaging to help manufacture a slowdown or a decline in demand, if you will.

Yesterday’s note touches on the quantum of the rate increases from the troughs.

Goldman Sachs joins the others below, where they think the Fed will raise rates 5 times this year.

“Bank of America Corp. now predicts seven rate hikes in 2022 and BNP Paribas SA forecasts six, while JPMorgan Chase & Co. and Deutsche Bank AG see five.”

Personally, I think their views are ridiculous and far-fetched.

My view is quite different.

I think the Fed raises rates twice this year and then corrects their actions with a rate cut.

My playbook suggests the Fed will hike and react to what the U.S. 2 year treasury note has done, which paints them as being behind the curve. They may be trying to temper inflation, which is mainly being driven by high commodity prices, disrupted supply chains and oddly, a tight labour market.

Politically, they will will feel pressure to do so, if at least to put a lid on U.S. gasoline prices.

But they won’t put rates up too much, for finally, inflation has reached the target rate that they have been wishing it would reach for many years.

As the government’s teat is removed from many and workforce participation increases (possibly because they lose money in their crypto portfolios), supply chains are rectified and commodity prices seriously mean revert, we should see inflation peaking (about now) and a lower GDP print for the March quarter, all without any meaningful rate hikes.

Excessive hikes will hurt GDP growth.

hint: mid term elections are coming in November 2022.

This may not sink in until after the May 4th Fed meeting.

More on the positioning of the investment playbook later.

Let’s get one thing straight…. The Federal Reserve is hopeless at trying to produce inflation.

It’s had bandied about some fantastical 2% inflation target for years. M2 Money Supply has risen by $6 trillion in 5 years, with half of that occurring in the past 3 months (and more to come) and still isn’t any sign of inflation.

It’s advisable to read up on Debt Deflation. That seems a more probable outcome.

Having said that, inflation could well rear its head as a result of something such an oil shock. Incidentally, the energy complex has a significant weighting when calculating inflation.

I don’t say this because I’ve recently re-read the events of 1970’s but there is some merit of that occurring within the current landscape.

But the Federal Reserve won’t be the ones who “create” inflation.