Iron Ore still not taking me higher

January 21, 2022 Leave a comment

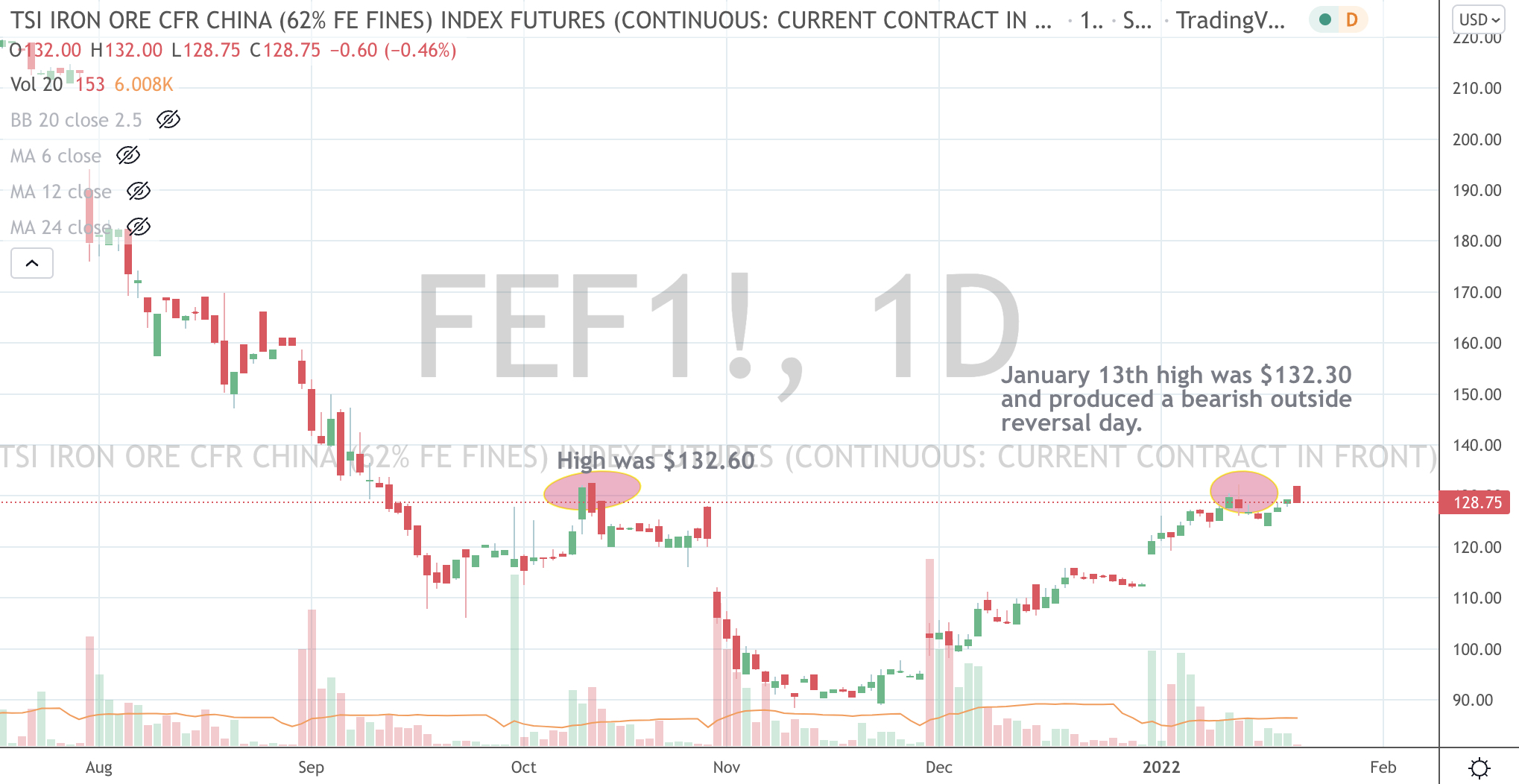

As the week progressed, Iron Ore still didn’t / couldn’t make the higher high highlighted in my post earlier this week.

Trying to hear what's not being said

January 21, 2022 Leave a comment

As the week progressed, Iron Ore still didn’t / couldn’t make the higher high highlighted in my post earlier this week.

September 2, 2021 Leave a comment

A ton of Iron Ore is now 25% cheaper than a ton of Jarrah firewood.

With all my writing about extremes and mean reversion, Iron Ore is reaching an interim point which increases probability of a ‘buying’ moment.

Currently, it is trading at US$145 per ton.

The chart below circles an area between US$124 and $132 which I think (in conjunction with my other indicators) present an opportunity for a ‘trading buy’.

Incidentally, that upward sloping line is Iron Ore’s 100 week moving average.

So, I’m looking for a 14% drop in the coming 15 days to satisfy a buying criteria and this will have an effect of your listed iron ore sensitive equities.

BHP at $40.45 perhaps?

September 2, 2021

by Rob Zdravevski

rob@karriasset.com.au

October 28, 2020 Leave a comment

During a client call yesterday, I was trying to give an example of what I thought was a ‘marginal trade’ and Fortescue Metals (FMG.AX) came to mind.

Coupled with my quick view of the iron ore supply and demand landscape, an iron ore price trading at the upper end of its historical range and a technical analysis snapshot, my opinion was that FMG either trades up or down $4, from its current price of $16.30.

Albeit a 25% return is enticing, an even money bet of perhaps losing 25% renders it a ‘marginal trade’.

To some extent, this can also be example where the investor needs to quantify or understand how much risk they are taking, compared to the return they are seeking.

Incidentally, in June 2020 I published an article (see link below) titled, “Iron Ore – As Good As It Gets”

#riskadjusted

#fmg

October 28, 2020

by Rob Zdravevski

rob@karriasset.com.au

June 23, 2020 Leave a comment

June 23, 2020

by Rob Zdravevski

Iron Ore – As Good As It Gets ?

Over the past 6 weeks, the price of 62% grade Iron Ore has risen 25%. It’s now trading around $102.

Prices have risen due to a combination of China’s factories and manufacturing returning to a “normalised” utilisation and Brazil shipping less ore.

The previous spike, in January 2019, saw Iron Ore price climb from $75 to $95 within 2 weeks and a subsequent surge to $125 occurred over the next 3 months.

This was mainly due to the collapse of a tailings dam in Brumadinho (owned by VALE), which also tragically resulted in lives being lost.

I can’t quite reason about the cause of the 2nd lurch higher as economies were at the tail-end of a 7-8 year economic cycle.

However, the price normalised back to over the next 4 months as Australian suppliers filled the gap.

<see chart below>

Today, the price of Iron Ore has risen again due to a Brazilian supply disruption aided by “newer news” that Brazil’s COVID-19 environment is worsening.

Once again, Australian iron ore miners seized the supply opportunity yet prices have continued to roar ahead.

It is at this point in time, that I now think, that this is as “good as it gets” for the Iron Ore price.

But I also have the following questions;

If the answer to these 3 questions is “Yes”, they then qualify for two of the three “cheaper, better and faster” categories.

Brazil could also be “faster” getting ore to the port, although overall we need to keep in mind that it does take 45 days to ship Brazilian Iron Ore to China when compared to the 12 day journey for Australian suppliers.

Anecdotally, I can’t help speculate that Brazil is feeling the strain of lower export receipts and may start to push product through its ports with less hesitation.

Inversely, it’s naive to think that China’s importers are submissive “price-takers” of sensitively priced commodities.

And so, my analysis of the price action in the Singapore traded 62% TSI contract suggests the strength of the advance is waning, as it makes a “rounding top” of lower highs and lower lows, a change in trend is near and the price traded to extremes on various measures.

The “fat part of the trade” has been seen and I expect it to retrace and trade down to $92.

For those who disagree, I am curious what you think will “drive” the price higher from here and how much risk are you taken when compared to the reward on offer when looking at the whole picture?

Until next time,

Rob

Subscribe to my blog: www.robzdravevski.com

Drop me an email: rob@karriasset.com.au

Some extra reading.

https://en.wikipedia.org/wiki/Brumadinho_dam_disaster

If you’d like to have a chat to me about some of our best stock ideas for your portfolio, feel free to call me on 0438 921 403.

Rob Zdravevski is the proprietor of Karri Asset Advisors, a specialist in the provision of investment advice and equity recommendations for clients’ portfolios.

January 31, 2015 Leave a comment

Once upon a time mining companies were making a lot of money by extracting ore from Australia’s crust.

Soon after, the government needed some money to pay for the debts they incurred as a result of the spending promises they made to the Australian public, in their attempt to remain elected to power.

They thought that they could invent a tax which charged mining companies for how much resources that they dig up and sell.

The tax was created. Some were happy and others weren’t. They was lobbying, protests, crying and demanding. The tax had a short life. The new government had mates in the mining sector. The tax was no longer alive.

It was OK ’cause the government still earned some sort of money from whatever businesses the large mining companies conducted, providing that they didn’t cleverly use their offshore subsidiaries to move around and book profits into.

The price of coal had already fallen, but nobody likes them anyway ’cause their industry is a visibly polluting one.

But oh oh – recently the price of Iron Ore has fallen.

This is how I see it,

Government let off the iron ore miners off the hook with the mining tax, less money for the government, then global demand slowed, the giants continued to increase supply, the price of iron ore fell, the companies made less profit but them increasing supply (coupled with falling commodity prices) also pressured the smaller miners, thus the giants are growing their market share, but government still needs more cash, there is no capital gains tax being paid of share profits because the stock prices of the major iron ore companies are the same as 5 years ago, thus shareholder return is poor, but hundreds of employees are making more than $400,000 per year.

It’s important to keep the gravy train going by any means you can, whether you manage to dupe government, the economy or shareholders.

Yet they still are on the look out for federal government help to assist them with their plight of iron ore prices being below their cost of production.

WTF?

January 26, 2014 Leave a comment

This is a periodical post about things that I see in the financial press, which I tend to interpret differently. When managing investors money, you need analyse the news and not just simply read it because you can’t assume you are getting to the truth.

Firstly, Jakarta warns Australia they are prepared to “clash” over border violations incurred by the Australian Navy. Australia best heed their warnings and wipe that smirk off your face because 300 million Indonesians should send your xenophobic fears into overdrive. I hope our government isn’t pinning all of our defensive hopes on U.S. Marines stationed in Darwin?

But equally Telstra is looking to form a 50/50 venture with Telekom Indonesia. Can David Thodey please be our next foreign minister?

I can’t believe why any company in the world wants to pay that much for a small insignificant business such as Warrnambool Cheese & Butter. Good luck to them.

Panic, Panic – protestors block Bangkok streets and the Thai Prime Minister is suspected of corruption. The Thai stock market has risen 9% in 10 days since this story picked up steam.

Alex Waislitz’s Thorney Group raises $68 million. Now I’m not sure what their raising target was but from a distance, their reputation could have easily raised 4 times that amount. My point is, would-be stockbroking firm geniuses should keep in mind that it’s difficult to raise money from the public.

With 65% domestic market share, Qantas still thinks it plays on an uneven playing field.

Franchisee of Australia’s 370 Burger King stores, Competitive Foods Australia, posts revenue of $1.03 billion for fiscal year 2013 and makes $21.4 million profit. That’s a lot of invoices and money to handle in order to make a 2% net profit margin. Last year, revenue was $935 million and profit was $8 million. Hey Jack, I see that cost cutting program is working?

Australian rail operators (in the Pilbra, Western Australia) are complaining that truckers have got an unfair price advantage when they transport iron ore. If trucking iron ore is cheaper than by rail, then the iron ore giants should then give their competitors access to their railroads. Umm, I didn’t think they would.

Various interviewees in newspapers are wishing for a weaker Australian Dollar. Be careful what you wish for. When you see commodity prices rise, it is usually accompanied by a higher Australian Dollar. In Australia we mainly export commodities, ’cause we don’t manufacture things such as cars, televisions or clothes anymore. So if the AUD remains weaker, we can sell US Dollar denominated commodities and receive a lot of AUD once its converted but it’s also good for overseas money to buy up Australian assets (see Australia is “on sale”).

Australia’s stock market falls due to weak Chinese data. Yup, heard this one before. Just like other brokers who actually ask me if I’m staying up late to watch the U.S. unemployment numbers. It doesn’t really affect the earnings of the shares in the companies that I and my clients own but if you need to justify a movement in the stock market with some sort of news, good luck and be my guest. Please continue to manage your investments on the basis of “jumping at shadows”.

Finally, this week, not a single economist who provided an estimate on the Australia Consumer Price Index reading got it correct and Deutsche Bank posted a “surprise” $1.15 billion quarterly loss.

Whether these professionals continually get their ‘calls” incorrect, can’t make money themselves or continue to pay fines for manipulation & price rigging, yet people still give these investment firms their money to manage.

November 14, 2013 Leave a comment

A country’s Foreign Affairs isn’t only about setting policy but you need to understand economics in order to achieve your diplomatic objective.

Having a few politicians who are certified Sinophiles isn’t an automatic pass either.

Unfortunately, politicians and their advisors often aren’t financially literate let alone considered to be business people and because of this, they fail to understand how to deal with other countries over the length of many economic cycles.

In Australia’s case, it was the only large developed economy to survive the 2008 Global Financial Crisis. The fact that it has hasn’t posted a year with negative economic growth for 22 years in another anomaly.

Over the past 10 years, Australia’s economy benefitted from China’s appetite for its commodity resources (see China’s stimulus) and we loved them for it but after a while Aussies weren’t happy with what panned out, as the social and financial divide was then blamed on a “Two-Speed” economy.

When a large trading partner saves your economy, you say “Thank You”.

You don’t;

Oh Australia, you just don’t get it.

October 27, 2012 Leave a comment

Did you know that over the past 6 weeks, the spot price of Iron Ore has risen 33% back to $120 per tonne?

Some investors may not believe this as they are still anchored to the bad news they saw last month with headlines such as ‘Iron Ore Prices Plummet”.

Credit to London’s Financial Times who did report the positive news this week.

source: Bloomberg