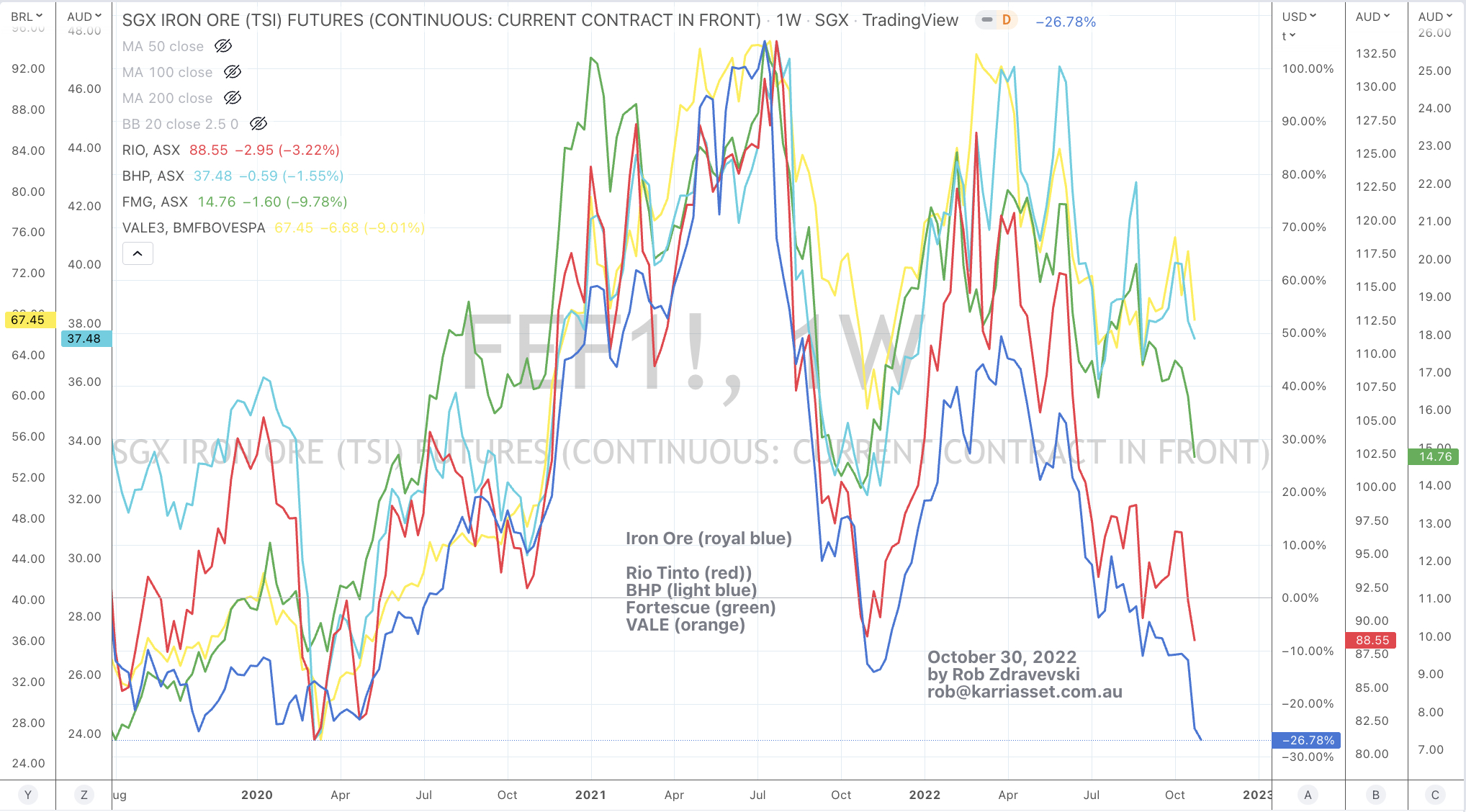

Lately, Australian iron ore miner, Fortescue Metals (FMG), has seen increasing speculating whether it will breach loan covenants or require more capital due to the fall its stock pice has suffered as a result of the decline in the spot iron ore price.

Depending what index you happen to watch, iron ore has fallen 40%-50% in the past 6 weeks.

Keeping with this blog’s mantra, “Trying to Hear What Is Not Being Said – It doesn’t matter what the iron ore price does week-to-week. The multi-year and decade demand for iron ore is stronger than the supply pipeline, especially with the scarcity of capital and expanding project costs to extract and ship it.

Furthermore, I don’t think that analysts fully take into account the iron ore reserves that FMG has. It seems they take the market capitalisation of $10 billion and look at its $8.5 billion of gross debt and start scaremongering. In fact, FMG has $2.3bn in cash, so it’s “net” debt is $6.2 billion.

Did you know that in the 2012 financial year, FMG had revenues of $6.7 billion and its EBITDA was$2.8bn? It’s net debt is less than 3 years worth of EBITDA, which is not a stretch considering its debt is priced at 600 basis points over the benchmark and is rated BB-.

FMG’s bonds aren’t trading at levels that indicate default or bankruptcy. I actually wish that they were trading at woefully large discounts as it would b a great investment opportunity. In fact, the upside for FMG’s debt is that their credit rating improves and their cost of borrowing drops and they subsequently re-finance.

I can’t say that FMG equity is dirt cheap but if you align yourself with its founder, owning the equity would be a more attractive than its “not quite cheap enough” debt.

Fortescue won’t fold or “go under”, irrespective of what ratings agencies have to say. In fact, Australia’s Labor government (who will most likely be re-elected in 2013) would be wise to stop bashing the iron ore miners and be prepared to shift their stance to being more supportive.

Imagine if Fortescue fails as a company? Directly and indirectly, FMG is responsible for (and has created) thousand of jobs. If government is bailing antiquated automobile manufacturers, it better get ready to support the iron ore industry.

Don’t they know that they would have a bunch of unhappy Chinese on their hands!