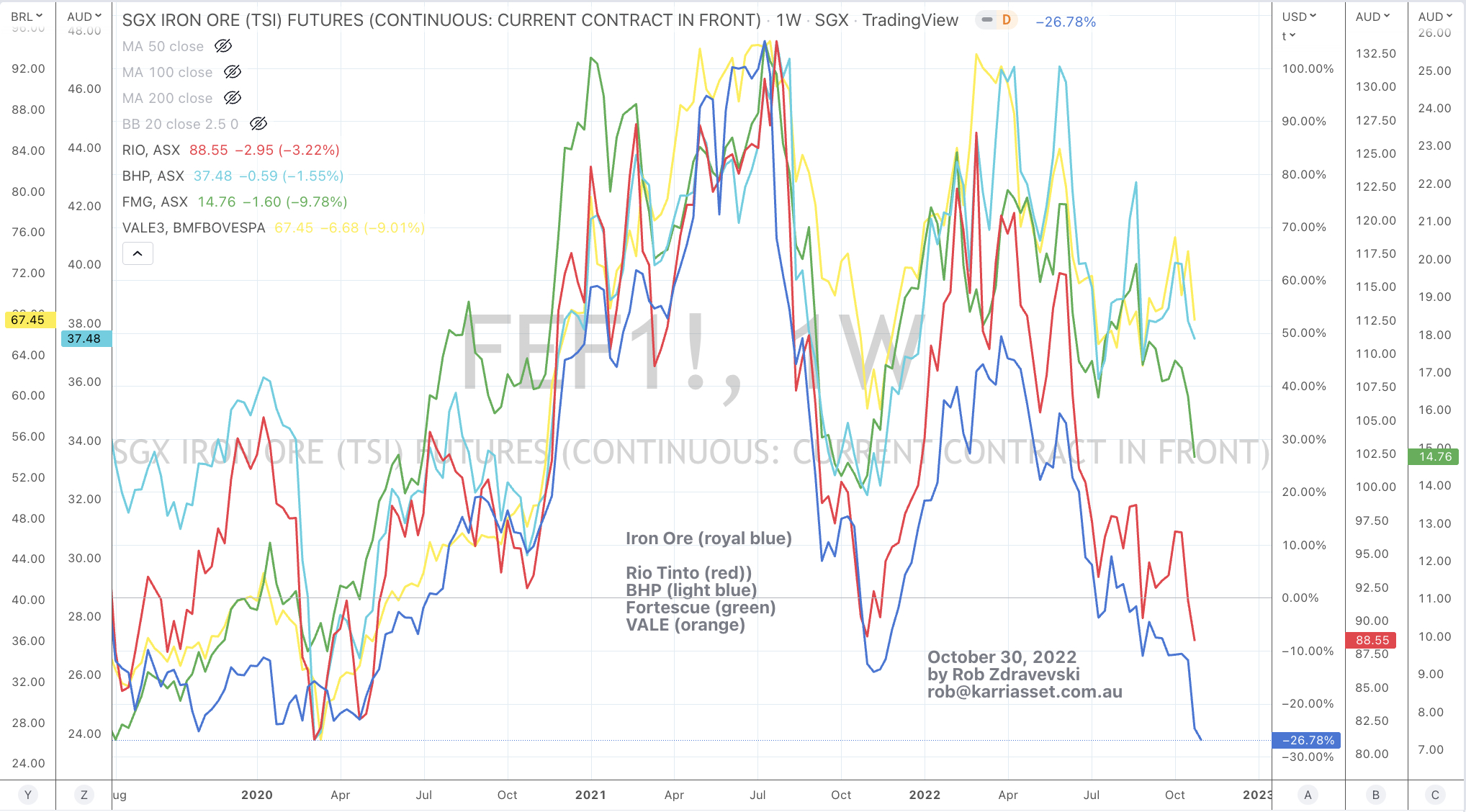

Here is a chart comparing the stock prices of Iron Ore’s Big 4 to the 62% grade Iron Ore price.

Rio Tinto is cuddling more sympathetically to iron ore’s recent decline.

Fortescue is next.

BHP less so.

VALE being the least.

The percentages that these stock prices are tracking Iron Ore’s price may be a representation of each company’s mine localities, corporate domicile, national allegiance or perhaps ‘politics’.

It may be a the market’s interpretation of who China may see as their preferred supplier?

Did you know that the price of Australian Premium Coking Coal has more than halved in the past 5 months?

The chart below shows it now reaching Oversold levels (on a weekly basis) and it has mean reverted to its 200 week moving average.

For the buyers of this coal (steel companies), this is good news. Their input prices are cheaper.

When you combine that with the price of shipping (as per the Baltic Dry Index) and Iron ore have both fallen 60% in the past 3 months…..then these cheaper ‘inputs’ bode well for steel producers.

However, the lower price being achieved for coking coal is carrying weight in the decisions of mining companies such as Australian headquartered, South 32, who has decided against proceeding spending $700 million to extend and expand the life at an existing metallurgical coal mine in New South Wales.

This follows its January 2021 decision to not develop a project in Queensland. It is now looking for a buyer of its 50% interest.

In both cases, South32 cited the allocation of capital didn’t support an adequate return nor making the projects financially viable.

Instead, they are opting to focus on North American projects, which is a ‘friendlier’ jurisdiction.

Beyond the ESG and political landscape, I also speculate the greatest risk comes from how the projects would be financed.

Furthermore, combine less supply of coking coal for local steel manufacturers, Australian tariffs on steel imports, China’s tariffs on its steel exports and a tight labour market…….domestic Australian steel prices aren’t about to decline anytime soon.

Here is an ongoing series of posts about Fortescue Metals (FMG.AX) and how it has traded at percentage extremes above it 200 week moving average. This helps tell you when chasing a stock higher becomes perilous in the face of a mean reversion, often when the tide and sentiment turns at its worst.

I don’t hate the stock nor the company. I’m just calling it as I see it.

For more than a year, FMG.AX has defied gravity.

If we see a break below $13.71, sees the stock visit $11.70 – $12.00, failing that it may test the $7.00 level.

A ton of Iron Ore is now 25% cheaper than a ton of Jarrah firewood.

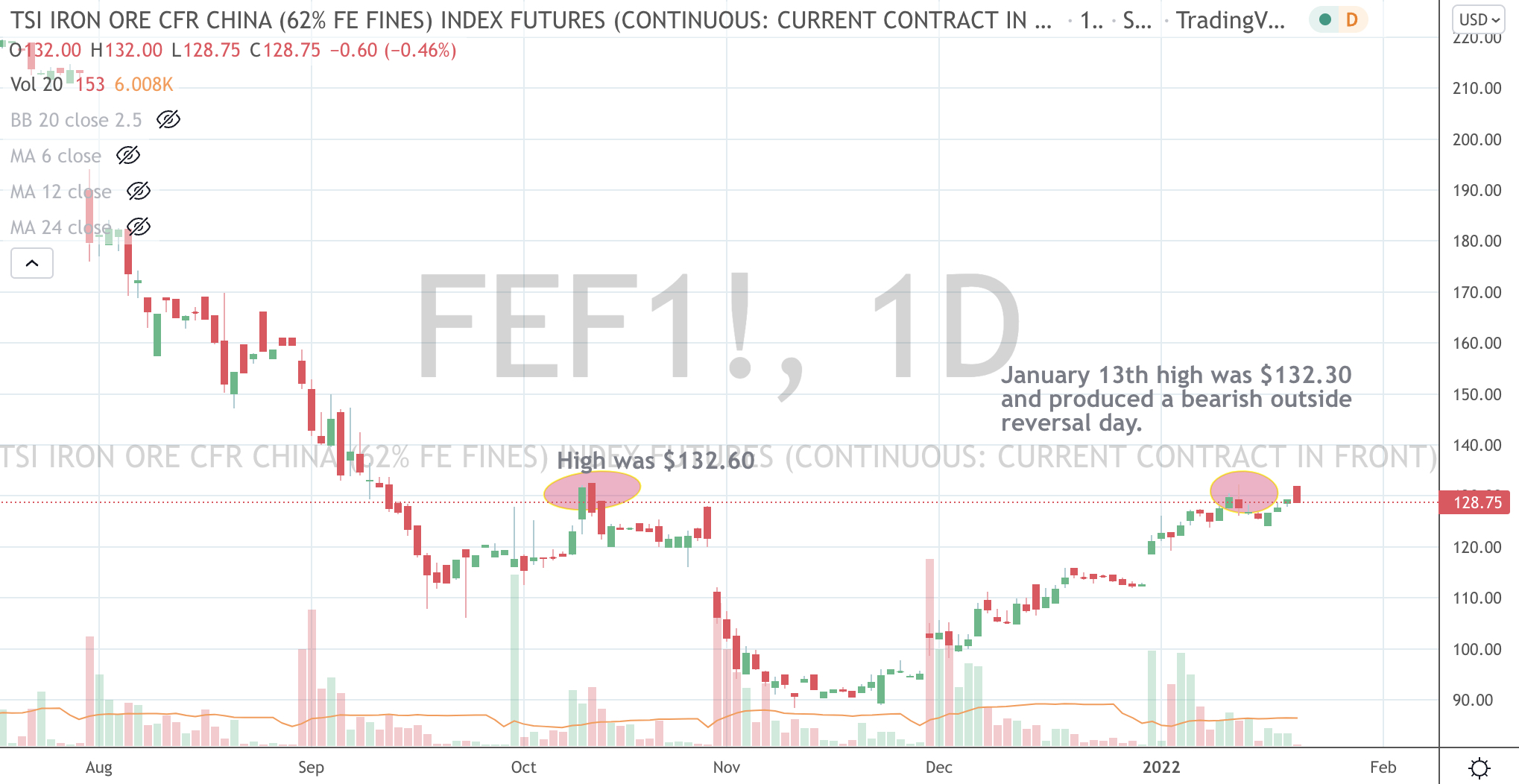

With all my writing about extremes and mean reversion, Iron Ore is reaching an interim point which increases probability of a ‘buying’ moment.

Currently, it is trading at US$145 per ton.

The chart below circles an area between US$124 and $132 which I think (in conjunction with my other indicators) present an opportunity for a ‘trading buy’.

Incidentally, that upward sloping line is Iron Ore’s 100 week moving average.

So, I’m looking for a 14% drop in the coming 15 days to satisfy a buying criteria and this will have an effect of your listed iron ore sensitive equities.