A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) either registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations

CRB Index

AUD/THB

MXN/USD

Overbought (RSI > 70)

Biodiesel

Robusta Coffee

AEX

KBW Bank Index

Budapest

CAC 30

DAX

Dow Jones Industrial Average

Italy’s MIB

Nasdaq Composite

S&P MidCap 400

Nikkei 225

Philadelphia SOX

TAIEX

Nasdaq Transports

Toronto’s TSX

FTSE 100

Vietnam

And the S&P 500 Index

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Russian 10 year bond yield

Gold in USD, AUD, CAD, EUR, GBP & CHF

Cocoa

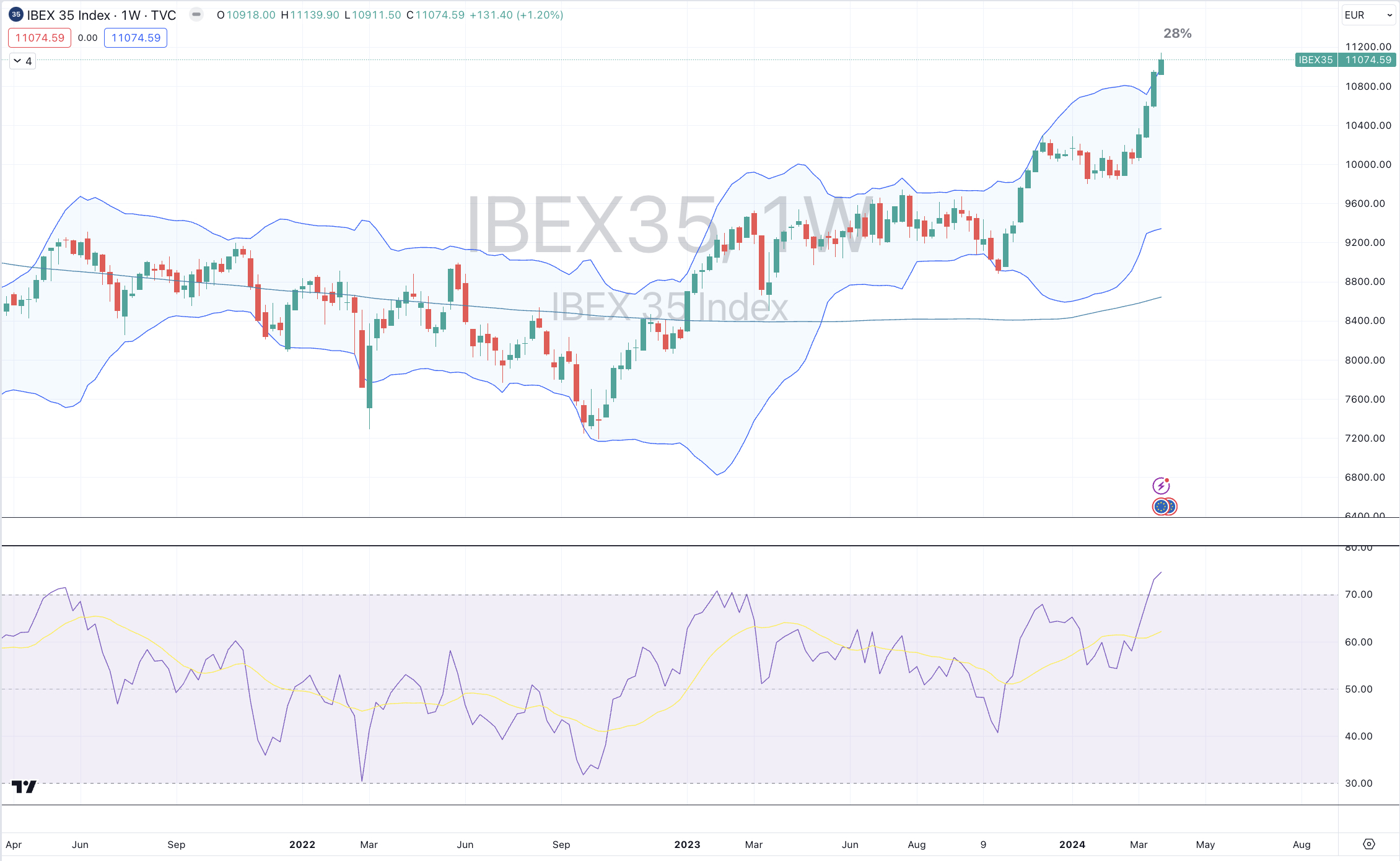

IBEX

Extremes “below” the Mean (at least 2.5 standard deviations)

CHF/AUD

Oversold (RSI < 30)

Chinese 10 year government bond yields

Lithium Hydroxide

Rice

The Oversold Quinella – Both Oversold and Traded at < 2.5 standard deviations below the weekly mean)

Australian Coking Coal

Chinese Coking Coal

Iron Ore

Shanghai Rebar

Notes & Ideas:

For the week, government bond yields were mixed with a light bias towards weakness.

The Japanese 2’s and 5’s yield took a break from rising with the latter ending its 7 week winning streak.

Over the past several weeks, yields remain mostly in sideways travel.

Russian 10 year yields broke their 8 consecutive weeks of increases.

And there may be a change in trend for the U.S. 3 month bills.

Equities were higher, again.

Other than movers listed below, many indices remained subdued for the week.

The KBW Banking Index makes a return to overbought territory (having risen in 5 of the last 6 weeks) as does the S&P MidCap 400 and the FTSE 100.

While Stockholm eases out of that category.

Oslo is in a 5 week winning streak.

Toronto’s TSK extends its winning streak to 7 weeks.

The DAX is in 8 week winning streak.

Italy’s MIB advance extends to 9 consecutive weeks, has spent 7 weeks in overbought territory and is trading at its highest price since April 2008.

Egypt 30 index has tanked 12.4% over the past fortnight.

The Nasdaq 100 is 33% above its 2090 week moving average while the S&P 500 is 27% above the same measure.

Spain’s IBEX has registered an overbought quinella as it trades at its highest point since May 2017.

The FTSE 100 returns to the overbought territory.

And the CAC and DAX are still making new all-time highs.

Commodities were generally higher.

Gold prices across various currencies remains overbought.

Prices related to steel production such as coking coal, iron ore, rebar, are all in oversold territory.

The ‘coking coals’ have fallen for 5 straight weeks.

Furthermore, U.S. Midwest Hot Rolled Coil Steel is approaching oversold land too.

Crude Oil, Copper, Tin and Silver moved out of overbought territory.

Rice has fallen for 5 consecutive weeks and its price has declined 14% over that time.

Cocoa has been overbought for 23 weeks.

Aluminium has risen for 5 straight weeks.

And Lithium Hydroxide has now spent 38 consecutive weeks in weekly oversold territory.

Currencies were tempered for the week.

The AUD was mixed, while the CAD and GBP were stronger.

The Euro wea weaker.

The Yen eked out some small gains,

And the Kiwi has declined for 5 consecutive weeks versus the Aussie.

The larger advancers over the past week comprised of;

Roterdam Coal 5.7%, Cocoa 9.3%, WTI Crude Oil 2.8%, Lean Hogs 2.5%, Arabica Coffee 2.2%, LNH in Yen 1.9%, Newcastle Coal 5.7%, Palladium 2.3%, Robusta Coffee 3.8%, Sugar 3.1%, S&P GSCI 1.4%, Brent Crude Oil 1.6%, Gold in AUD 3.1%, Gold in CAD 2.8%, Gold in USD 3.2%, Gold in CHF 3.6%, Gold in EUR 3.3%, Gold in GBP 2.9%, KBW Bank Index 3.1%, DAX 1.6%, S&P Small Cap 600 2.6%, Russell 2000 2.6%, KRE Regional Banks 3.7%, Karachi 2.8%, S&P Midcap 400 2%, South Africa 2%, Chile 1.9%, ASX 200 1.6% and the ASX Materials, Industrials and Small Caps all rose 2% for the week.

The group of largest decliners from the week included;

Australian Coking Coal (10.5%), Baltic Dry Index (17.1%), China Coking Coal (10.5%), HRC Steel (3.2%), Iron Ore (9.3%), Lumber (3.9%), Natural Gas (3.8%), Nickel (2.8%), Nickel on MCX (4.2%), Shanghai Rebar (2.8%), Dutch TTF Gas (1.5%), Egypt 30 (5.2%) and the Nasdaq 100 fell 0.5%.

March 31, 2024

by Rob Zdravevski

rob@karriasset.com.au