The following assets (on a weekly timeframe) registered an Overbought reading or traded more than 2.5 standard deviations above its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations)

Australian 2, 5 & 10 year government bond yields

Spanish, Greek & Italian 10’s

Dow Jones Industrial Average

S&P Midcap 400 Index

Russell 2000 Small Cap Index

Nasdaq Transports

Overbought (RSI > 70)

WTI Crude Oil (the March 2022 contract)

Gasoil

the JKM “Japan/Korea (LNG) Marker”

Natural Gas

Australian coal

Urea

Cattle

Amsterdam’s AEX equity index

Dow Jones Transports index

And the USD/TRY (setting a new all-time low in a weakening Turkish Lira)

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

France’s CAC-40 equity index

Dow Jones Transports

Italy’s MIB equity index

Nasdaq 100

Oslo Bors equity index

Philadelphia Semiconductor Index

S&P 500

And Instanbul’s BIST equity index

Assets (securities) which touched the other side of the extreme, being Oversold (where the RSI is < 30) or were at least 2.5 standard deviations below its mean are;

Extremes “below” the Mean (at least 2.5 standard deviations)

GBP/USD – suggesting a weaker British Pound

Rice

Oversold (RSI < 30)

Iron Ore

The Oversold Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean.

None

Notes & Ideas:

The two notable asset class moves this week were dominated by the reversal in bond yields which saw them fall sharply (meaning the buying of bonds was quite aggressive) along with a host of +2% advances amongst various equity indices.

In fact, the decline in government yields isn’t a surprise. Past editions of ‘Extremes’ contained examples of where the Aussie 10’s moved from 1.77% to 1.95%. In this past week, they retraced the previous week’s move, to close back at 1.74%.

The yield in the Aussie 5’s fell from 1.46% to 1.27% .

It was actually uncanny that yields seemed to fall 20 basis points in many countries irrespective of their actual yield percentage.

However, countries who have recently raised rates where the interesting exceptions. New Zealand saw their 10’s only decline from 2.60% to 2.55%, Norway fell from 1.70% to 1.56% while Poland’s 10’s rose from 2.88% to 2.91%.

In last week’s edition, I highlighted the contrast in Greek 10 year bonds which were yielding 1.33%.

I find it interesting that this yield seems to imply a similar risk/return to the U.S 10’s yield of 1.45%. Does that make Italian, Spanish and Portuguese 10 year government bond yields more creditworthy than the United States? They yield 0.88%, 0.41% & 0.33% respectively.

And when compared to the aforementioned Norway, it’s equally difficult to reconcile their pricing.

Incidentally, the investors fancied Greek 10 year bonds, seeing its yield firm from 1.33% to 1.09% this week.

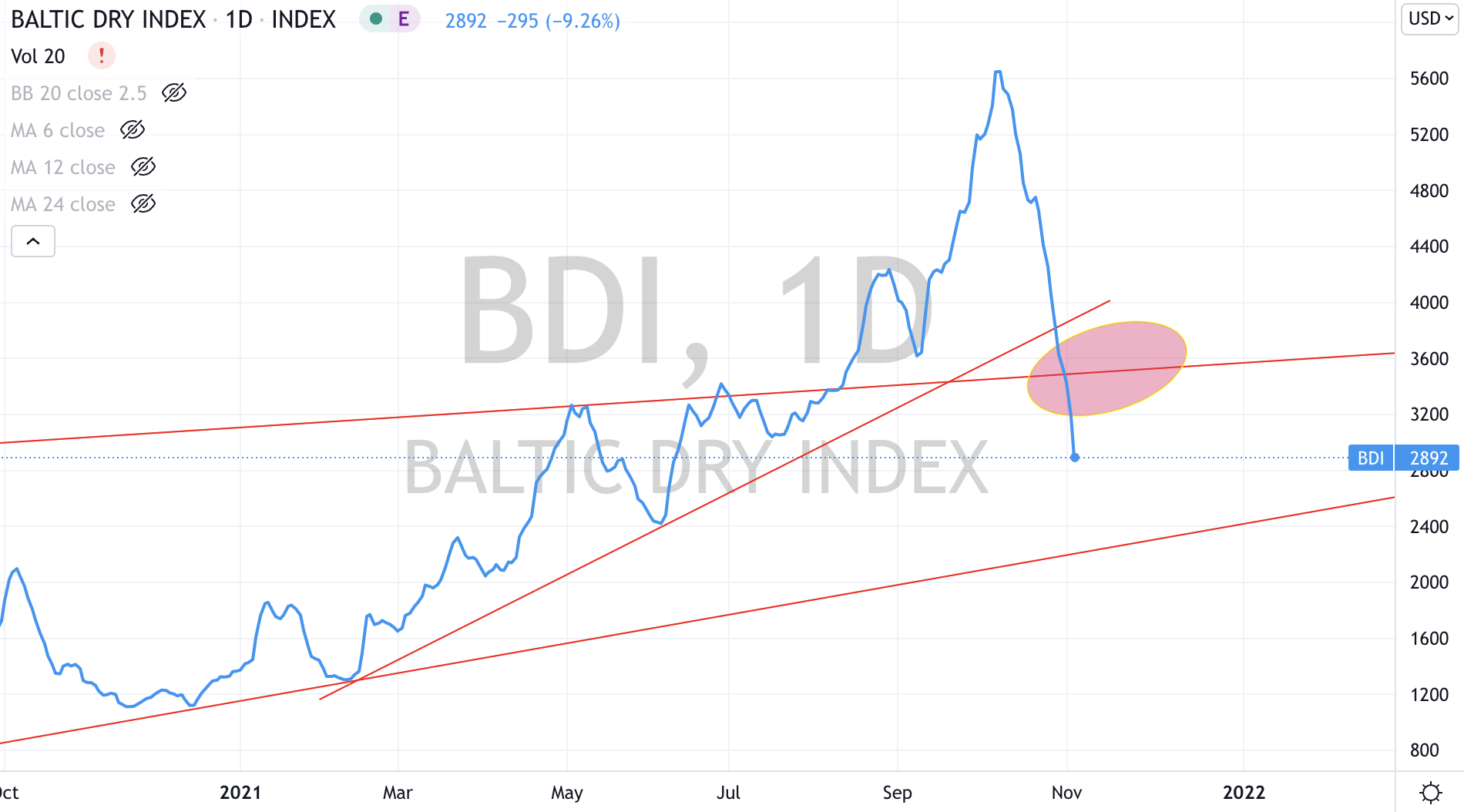

In other happenings, the Baltic Dry Index continues its mean reversion (the cost of bulk shipping) falling 23%, making for a 64% decline in 4 weeks.

Aluminium fell 5.4% giving it a 18% decline in the past 3 weeks and Chinese Coal prices have sunk 26% over the same time.

On the topic of mean reversion, many assets/securities/commodities continue their decline or meander lower, especially as some revert from euphoric media emphasising peaks.

Last week, I wrote that I was watching the AUD/USD test 0.7520. Alas, it didn’t break that level and we now see it at 0.7399.

The larger advancers over the past week comprised of JKM LNG 5.4%, Lumber 4.3%, Iron Ore 2.3%, Cattle 2%, Sugar 3.5%, Gold (in AUD) 3.6%, Gold (in USD) 2%, Rotterdam Coal 3.7%, Dutch TTF Gas 14.1%, Urea 6.6%, CAC 40 3.1%, DAX 2.3%, DJ Transports 5.9%, FTSE MIB 3.4%, Midcap 400 4%, Nikkei 2.5%, Oslo 3.3%, Helsinki 2.2%, Russell 2000 6.1%, SOX 8.9%, S&P 500 2%, Taiwan TAEIX 1.9%, Nasdaq Transports 2.4%, ASX 200 1.8% and Istanbul 5.7%.

The group of decliners included Aluminium (5.9%), Baltic Dry Index (23%), Cocoa (5.8%), WTI Crude (2.8%), Nickel (2%), Orange Juice (3.8%), Gasoline (2.1%), Corn (2.7%), Soybean (3.5%), China Coal (5.7%), Uranium (7.7%) and the Hang Seng Index fell 2%.

November 7, 2021

by Rob Zdravevski

rob@karriasset.com.au