Stock prices are discounting lack of visibility.

September 16, 2022 Leave a comment

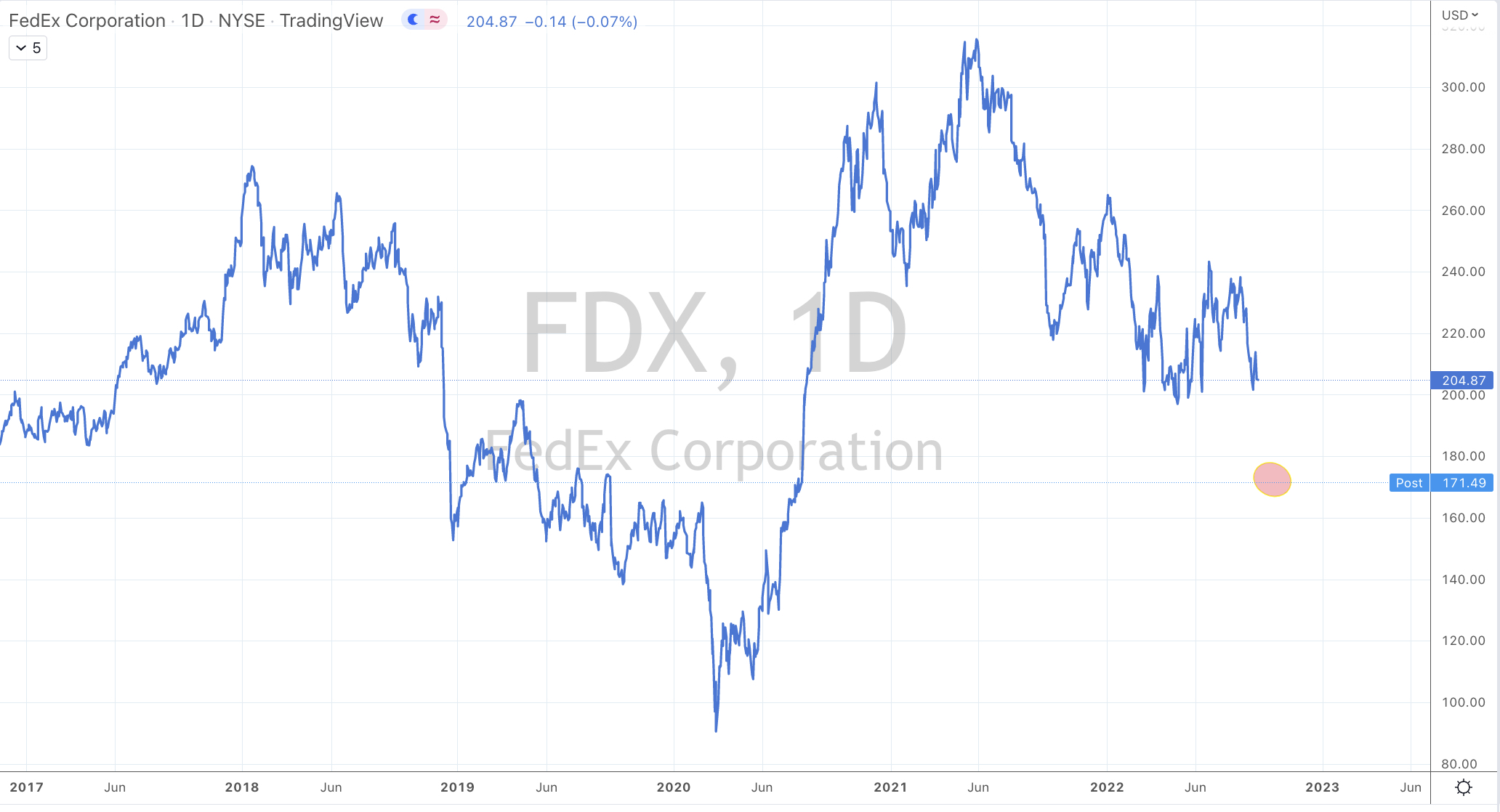

Has the market already discounted a decline in earnings for FedEx?

Has it already anticipated broker estimate downgrades?

Today, FedEx (FDX) guides 1Q23 EPS well below consensus and guides Q2 EPS and revenue below consensus and withdraws FY23 earnings guidance.

But the adjustment of expectations relating to future earnings has occurred in many stocks across various industries.

There has already been much damage.

By tomorrow’s close (stock is down 17% in today’s after-market) the stock has halved from its June 2021 high.

It is interesting to note that many stocks peaked 14-18 months ago.

September 16, 2022

by Rob Zdravevski

rob@karriasset.com.au