A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations)

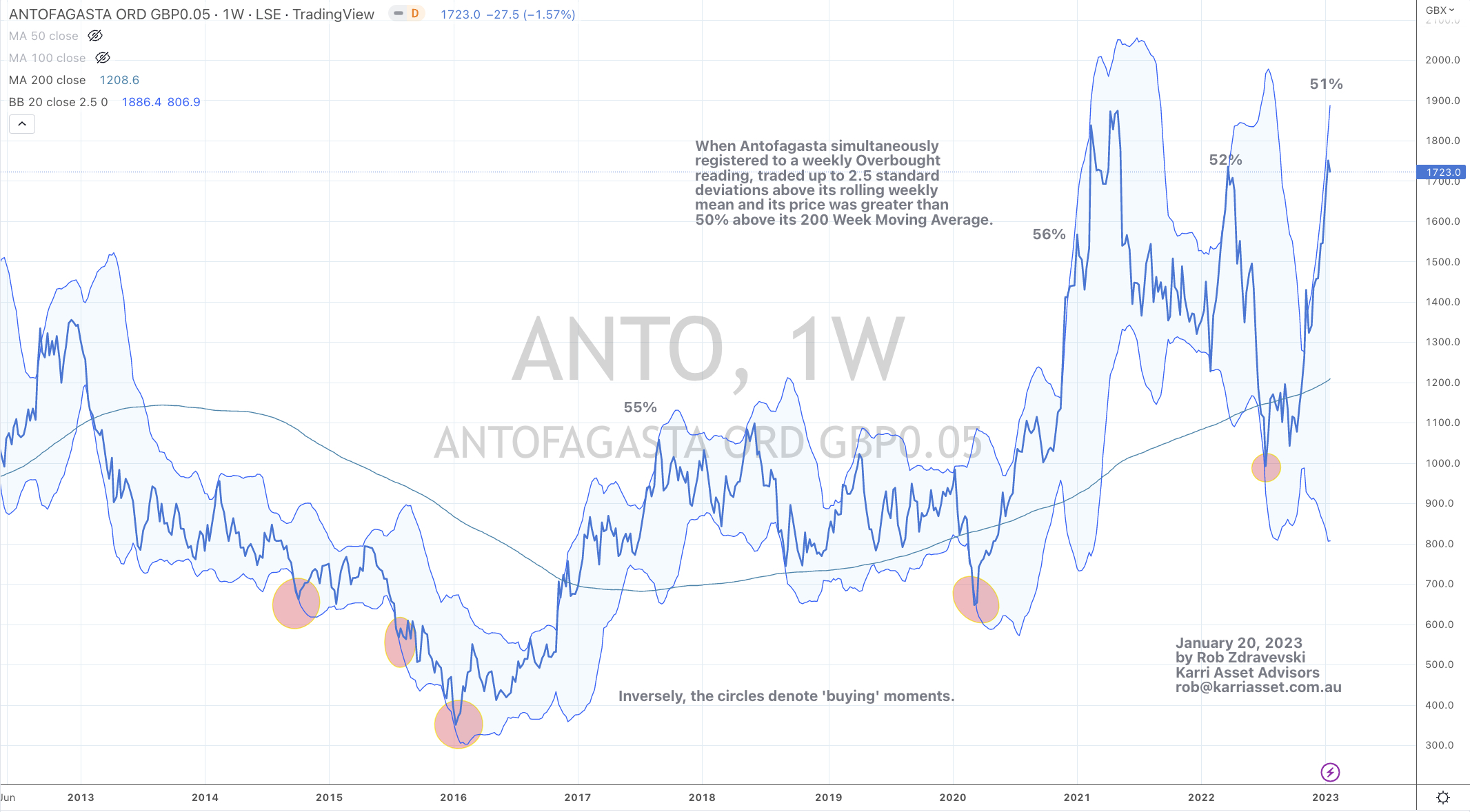

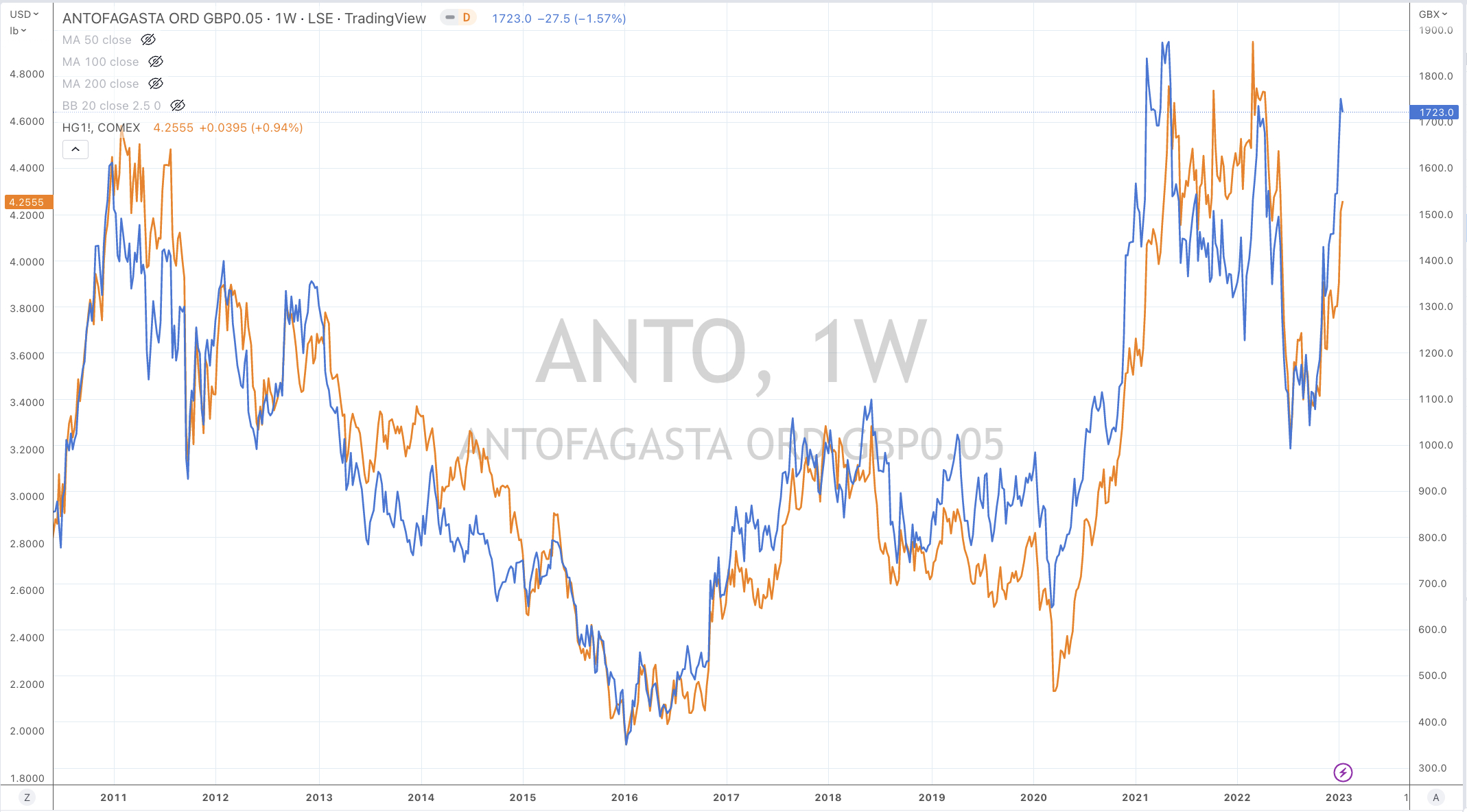

Copper

Copper/Gold Ratio

Overbought (RSI > 70)

German 2 year government bond yields

Gold (in Canadian Dollars)

Gold (in U.S. Dollars)

Cattle

Istanbul’s BIST Index

SGD/USD

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

None

Extremes “below” the Mean (at least 2.5 standard deviations)

None

Oversold (RSI < 30)

U.S. 5 year yield minus U.S. 3 month bill yield spread

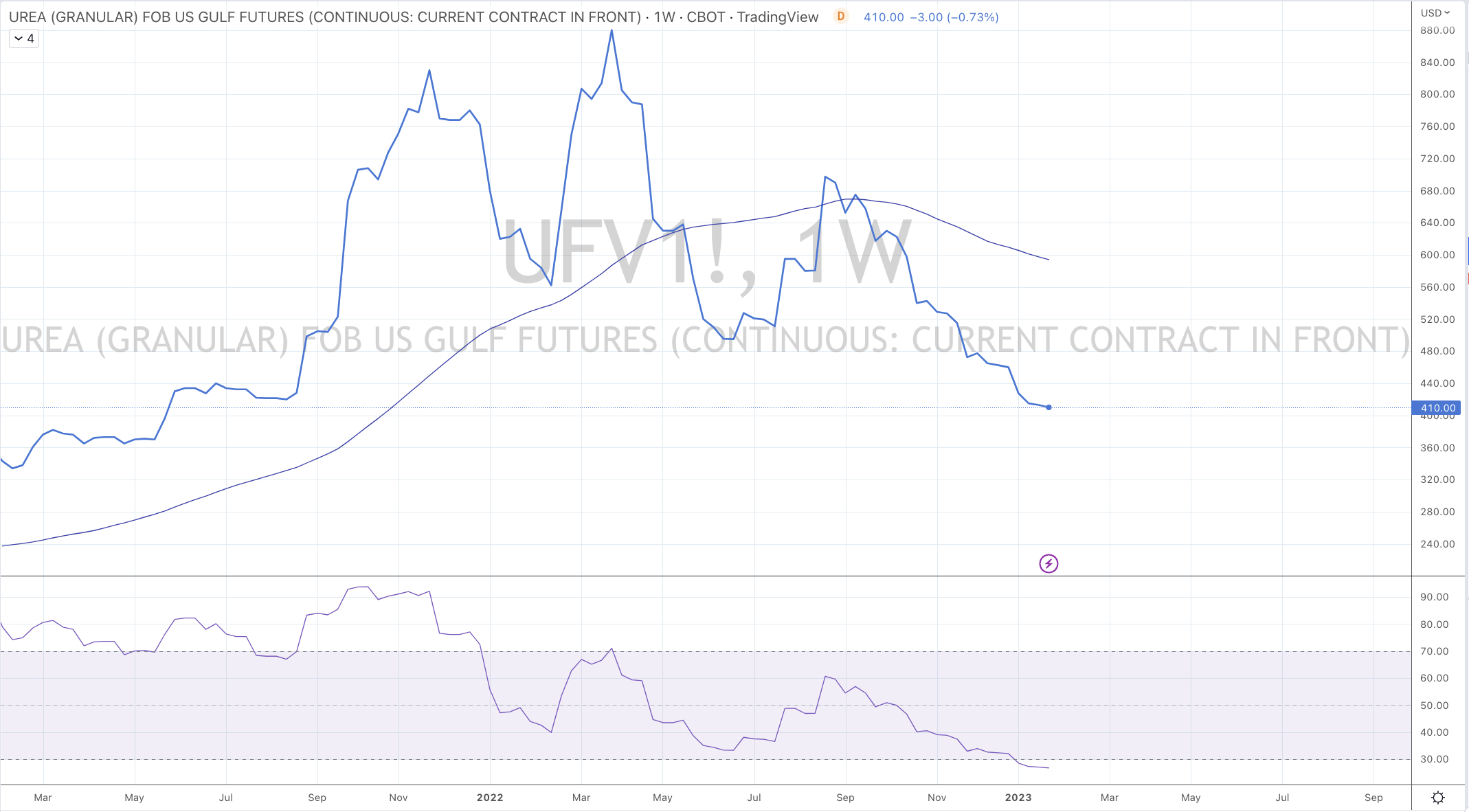

Urea (U.S. Gulf)

Urea (Middle East

The Oversold Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

None

Notes & Ideas:

Global Equities mostly had a benign week with Chinese stocks continuing to steadily add to their gains.

Now, we are hearing bullish cries from many firms but in the near-term, it’s too late. Chinese equity indices have risen 18.5% over the past two and half months and nearing towards an ‘extreme’. Such a return is also a reminder to calibrate ones expectations.

In commodities….over the past 2 weeks, energy prices (except for Natural Gas) have rebounded. This is understandable considering their recent declines.

Gasoil, Brent Crude and WTI Crude have risen 11%, Heating Oil is up 15% and Gasoline has bounced 17%.

6 week ago, Gasoline completed its mean reversion (down to its 200 week moving average), more than halving from its peak of $4.30 to a low of $2.02.

Dutch TTF Gas and Urea have nearly mean reverted. Cotton, Coffee and Natural Gas already have done so.

The latter has slumped a stunning 72% from its high and has just completed its 6th consecutive ‘down’ week’. Bounces are expected when weekly streaks reach 6, 7 or 8. It’s rarefied air.

And Palladium closed at its lowest level since December 20, 2021.

Bonds were the biggest newsmaker for the week as they continued their rally. Buyers remained the more aggressive and yields generally fell across the world.

Whilst they have made a reasonable swoon towards their long term means and arguments for such gravitational pull has validity, in the interim bond yields are nearing some Oversold ‘extremes’.

Incidentally, the U.S. 5 year inflation breakeven rate has nearly mean reverted, which I find understandable considering the same has bee occurring in many commodity prices.

There was much palaver made about the Bank of Japan losing their marbles and control of the Japanese 10 year Government Bond (JGB) yield…….but the ‘widow-maker’ soon returned posting a bearish outside reversal week and yield fell from 0.53% to 0.37%.

Other price action news saw outside bearish reversal weeks in USD priced Silver, AUD/GBP and AUD/EUR, while the AUD/JPY and the Nikkei 225 made the opposite.

The KBW Banking Index can be thankful for Friday’s 3.1% surge to allow it to finish the week only down 0.5%.

The AUD/CAD is nearing an Overbought extreme.

The Baltic Dry Index has now tanked 62% in the past 3 weeks.

The Indian Rupee (vs., USD) isn’t Oversold anymore and building a base near its multi-year lows.

And while I watch for more mean reversions to complete, it’s folly to ‘paint shapes’ resembling a “V” or a “W” assuming prices sharply recover up to where they recently came from.

The larger advancers over the past week comprised of;

Australian Coking Coal 3.3%, Rotterdam Coal 3.2%, WTI Crude 2.2%, Gasoil 5.4%, Heating Oil 6.5%, JKM LNG 13.1%, Coffee 2%, Tin 6.3%, Gasoline 4.5%, Cotton 5.4%, Dutch TTF Gas 3.2%, Brent Crude 2.6%, Oats 1.9%, S&P GSCI 1.7%, Shanghai 2.2%, CSI 300 2.6%, Turkey’s Istanbul BIST Index 10.7% and Australia’s ASX 200 rose 1.7% while the ASX Small Cap Index improved 0.6%.

The group of decliners included;

Baltic Dry Index (19.3%), Cocoa (3.1%), Natural Gas (7.2%), Palladium (3.6%), Platinum (2.3%), Urea Middle East (5.2%), Uranium (2.5%), DJ Industrials (2.7%), S&P 500 (0.7%) while the FSTE 100, Russell 2000 and the S&P MidCap 400 all fell 1%.

January 22, 2023

by Rob Zdravevski

rob@karriasset.com.au