A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations)

U.S. 10 year minus U.S. 2 year yield spread

SHY

Overbought (RSI > 70)

Hot Rolled Coil Steel (HRC)

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Gold (in AUD and CAD)

Gold Volatility Index

Extremes “below” the Mean (at least 2.5 standard deviations)

U.S. 5 year yield minus U.S. 5 year breakeven inflation rate

Australian 3 and 5 year bond yields

Copper/Gold Ratio

U.S. 2 year bond yield

CRB Index

Corn

Rice

DJ Industrials

Nifty & Sensex indices

The major equity index in Norway, Swiss, Singapore, Malaysia and Thailand

AUD/EUR

CAD/USD

AUD/SGD

Oversold (RSI < 30)

Urea (U.S. Gulf)

Urea (Middle East)

The Oversold Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

KBW Banking Index

Notes & Ideas:

In as the previous week in Equities, I am pasting the same opening paragraph as last week.

They were weak across the board led by U.S. banks, mid caps and small caps, while some holdout from the broad decline such as Taiwan only easing 0.5%.

But not all equity indices fell sharply. The Dow Jones Industrials eased 0.2% as did the CSI 300. Amongst U.S. banking liquidity concerns, the KOSPI, Shanghai Composite and Hang Seng rose 0.1%, 0.6% and 1%, respectively.

In fact, it may seem perverse that the S&P 500 rose 1.4% on the week, while the Nasdaq composite soared 5.8% for the week. But it isn’t too strange when you consider that collapsing yields gives the stock prices of technology companies tailwinds.

So much so, that the Nasdaq 100 and Philly Semiconductor Index had a bullish outside reversal week.

In the previous week, the Nasdaq Biotech Index revisited an oversold extreme. This past week, it rose 2.2%.

And finally, Helsinki mean reverted to its 200 week moving average.

Amongst bonds, yields continued to fall, heavily.

Although, there were a few which fell to a lesser degree and closed nearer to the middle of the week’s range.

The most dramatic observation is that the U.S. 10 year minus 2 year bond spread (yield curve) moved from a ‘negative’ 2.5 standard deviation to a ‘positive’ 2.5 standard deviation reading within 1 week.

Closest similar observation and occurrence was on February 24, 2020 and then on May 27, 2019.

The other way occurred on August 7, 2000.

On a yield basis, this spread moved from (1.08%) to (0.33%), closing at (0.43%).In the pre ious week, the media was making a hoo-ha about the yield curve being the most negative in decades.

Keep in mind, such extremes don’t stay as so, for too long.

Meanwhile, the JGB’s experienced a massive decline yields. Shorting the JGB’s has been considered the ‘widow-maker’ trade for decades. It’s yield started from a high of 0.385% and moving down to a intra-week low of 0.167%, they closed at 0.285%. They were trading at 0.52% 2 weeks earlier. This has other implications too.

U.S. 5 year inflation break-even rate has nearly mean reverted to its 200 week moving average, telling us that inflation is easing.

While I remind myself to balance the drama and noise being distributed. The high of the U.S. 20 year bond yield was seen in late October 2022 and the recent ‘dramatic’ decline in yields didn’t break the low seen in late January 2023.

And the U.S. 30 year yield hasn’t broken below the early December 2023 low.

In commodities, the Baltic Dry Index has risen 127% in 4 weeks.

Energy continued its weakness. WTI Crude finally mean reverted to its 200 week moving average completing a big call I made a year ago.

Brent Crude is nearly at its mean reversion, while Aluminium and Lean Hogs made double dip visit to that mark.

Gold rallied some more is overbought in various currencies.

JKM LNG is closing in on my buy target although we need temper expectations of prices skyrocketing again. It’s not prudent to paint ‘shapes’ of V’s or W’s.

Grains rose across the board. Remember, in last week’s edition, I wrote that Wheat completed a mean reversion back to its 200 week moving average. It rose 4.6% this past week.

The Copper/Gold Ratio is ‘oversold’.

And Cattle broke its 22 consecutive week overbought streak. It’s not too late to increase the percentage of your herd sales.

In currencies, don’t much was doing.

The larger advancers over the past week comprised of;

Rotterdam Coal 2.2%, Baltic Dry Index 9.6%, Lumber 8.7%, Palladium 1.8%, Silver in AUD 7.5%, Silver in USD 9.4%, Gold in AUD 4%, Gold in USD 5.9%, Gold in CAD 5.2%, Corn 2.8%, Rice 5.2%, Wheat 4.6%, HSCEI 2.6%, Nasdaq Composite 4.4%, Nasdaq Biotechs 2.2%, Nasdaq 100 5.8%, SOX 5.5% and S&P 500 rallied 1.4%.

The group of decliners included;

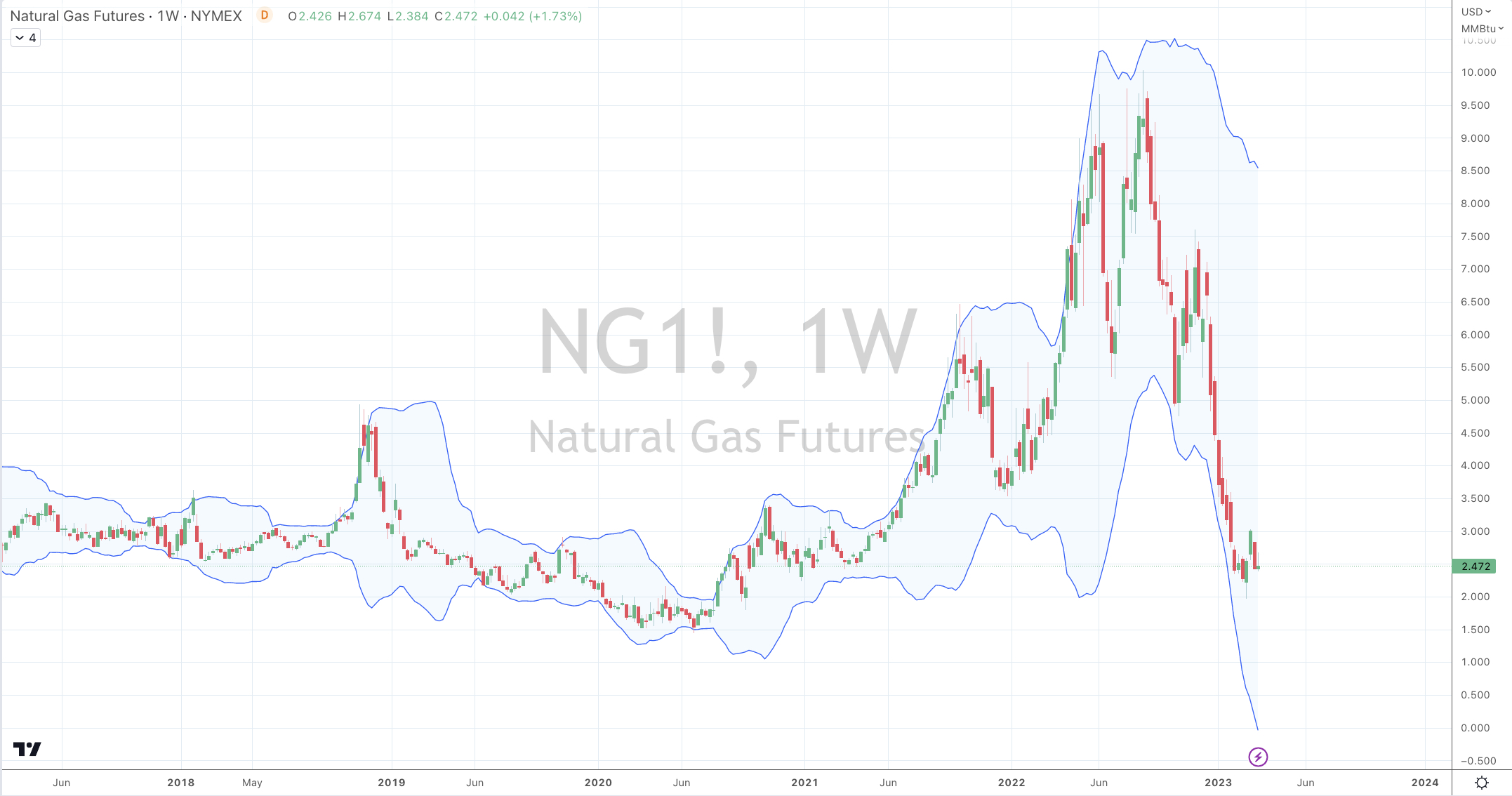

Australian Coking Coal (3%), Aluminium (2.6%), Brent Crude (12.3%), China Coal (2.1%), WTI Crude (13.3%), Gasoil (7.6%), Hogs (8.7%), Copper (3.4%), Heating Oil (3.4%), JKM LNG (4.2%), Tin (5.1%), Natural Gas 3.1%, Nickel (4.4%), Gasoline (5.9%), Sugar (2.3%), Dutch TTF Gas (19.1%), Uranium (2.1%), Soybean (2%), SPGSCI (6%), AEX (2.8%), KBW Bank Index (14.6%), CAC (4.1%), DAX (4.3%), DJ Transports (3.1%), MIB (6.6%), IBEX (6.1%), S&P MidCap 400 (3.3%), Nikkei (2.9%), Oslo (5.5%), Copenhagen (2.4%), Helsinki (5.3%), Stockholm (4.8%), Russell 2000 (2.8%), Sensex (1.9%), S&P SmallCap 600 (3.4%), Nasdaq Transports (4.7%), TSX (2%), FTSE 100 (5.3%), SET (2.3%), Chile (5.2%), ASX SmallCaps (2.6%) and the ASX 200 fell 2.1%.

March 19, 2023

by Rob Zdravevski

rob@karriasset.com.au