Inverted yield doesn’t kill the bull market

February 17, 2023 Leave a comment

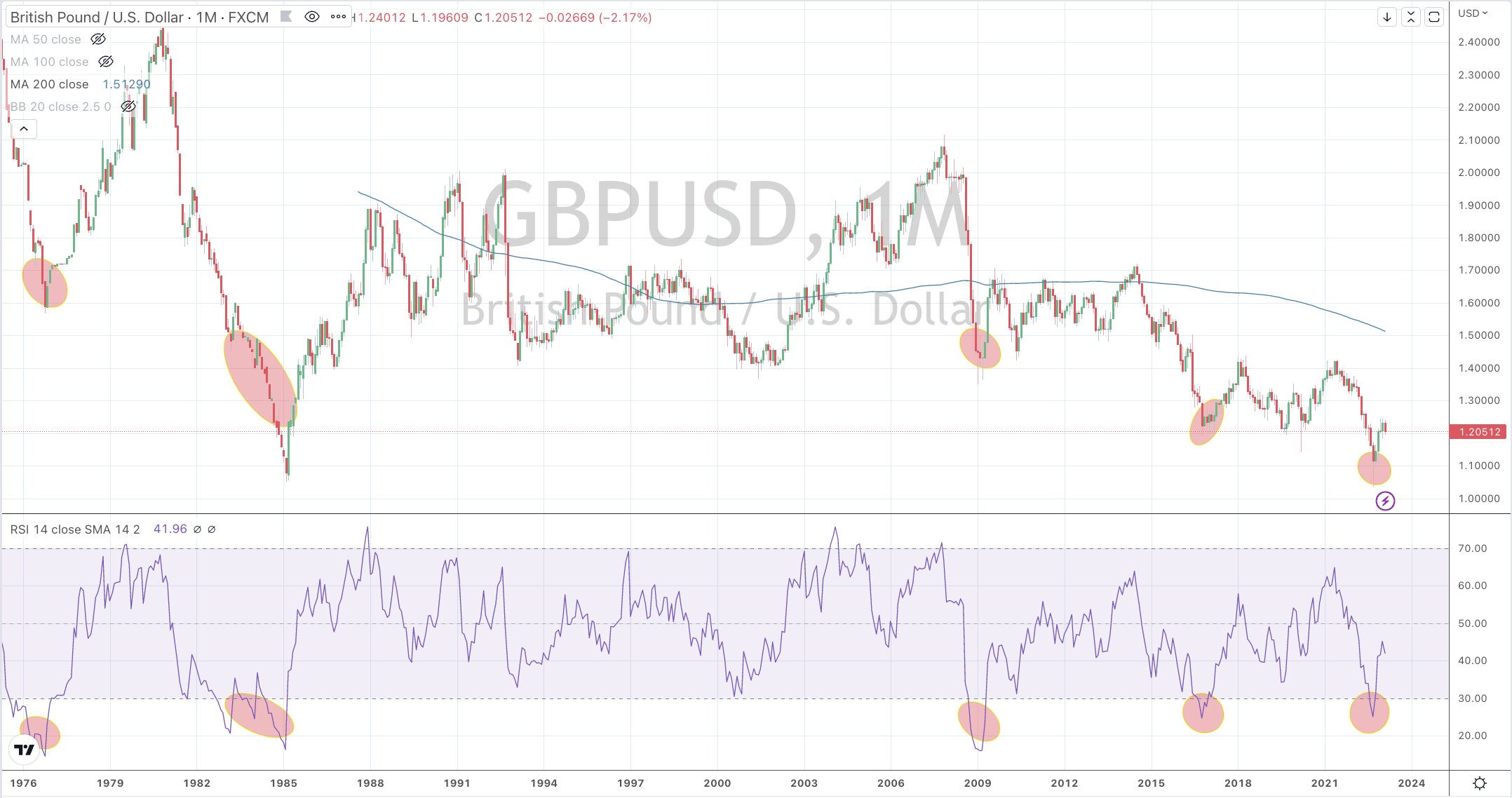

The genesis of today’s preceding post….was this note written nearly 2 years ago.

The notations in the chart within the link said that if the U.S. 10 year minus 2 year spread rose then the bull market is stifled.

Instead the yield curve moved towards and below zero….thus the equities bull market has remained intact.

So much so, the S&P 500 rallied 12% from that June 2021 moment and even today, the S&P 500 is the same price as then.

Hardly, a downdraught let alone a bear market as depicted in the elongated ovals of 2001 and 2008 as per the original post.

Below, is how today’s study looks.

February 17, 2023

by Rob Zdravevski

rob@karriasset.com.au