Peaking bond yields…..

June 4, 2024 Leave a comment

I’m watching how the German 2 year bond yield tracks the Nasdaq 100 (or vice versa)

June 4, 2024

Trying to hear what's not being said

June 4, 2024 Leave a comment

I’m watching how the German 2 year bond yield tracks the Nasdaq 100 (or vice versa)

June 4, 2024

June 2, 2024 Leave a comment

A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) either registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

* denotes multiple week inclusion

Extremes above the Mean (at least 2.5 standard deviations)

German, Spanish, French, British, Greek and Portuguese 10 year government bond yields

British 3 year bond yields

Dutch TTF Gas *

Wheat *

And India’s SENSEX equity index

Overbought (RSI > 70)

Japanese 2 & 5 year government bond yield *

Russian 10 year government bond yield *

JKM LNG

Biodiesel

Rubber

GBP/JPY

Pakistan’s KSE Index *

Oslo *

and Turkiye’s BIST 100 *

The Overbought Quinella (Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Japanese 10 year government bond yield *

Robusta Coffee

Extremes below the Mean (at least 2.5 standard deviations)

Australian 10 year minus Australian 2 year government bond yield spread *

Chilean 2 year government bond yield

EUR/GBP

Brazil’s BOVESPA equity index

Oversold (RSI < 30)

North European Hot Rolled Coil Steel *

Lumber *

Lithium Hydroxide *

Sugar *

PHP/USD

And Indonesia’s IDX 30 equity index

The Oversold Quinella (Both Oversold and Traded at < 2.5 standard deviations below the weekly mean)

None

Notes & Ideas:

Government bond yields rose, mostly, again.

However, the correlation between the Copper/Gold Ratio was bucked.

The Japanese bond yields all remain at extremes.

Equities were mainly weaker, again.

Many indices fell between the 1% – 1.3% range.

Several more indices dropped out of overbought territory.

The Nasdaq Composite, SENSEX, SOX, the ASX Industrials and Chile’s equity index all performed an outside bearish week.

The Nasdaq Composite, KLSE, FTSE 250, Nasdaq 100, S&P 500 and TAEIX all broke their 5 week winning streak.

Oslo makes another all-time high.

Last week’s weekly outside bearish week for the HSCEI and Indonesia’s IDX resulted in declines of 3.2% and 4.1% respectively.

Commodities were mostly weaker.

Coal, Cocoa, & Coffee all saw strength again.

Robusta Coffee and Cocoa have risen 19% and 25%, respectively over the past fortnight.

Cotton, Copper, Palladium, Corn, Orange Juice and Lumber were amongst the weakest performers for the week.

Copper has fallen 9% in the past 2 weeks.

Rice has slumped 8% in the past 3 weeks.

The Copper, Platinum, Nickel, Tin and the Copper/Gold Ratio aren’t overbought anymore. The latter is more relevant as a risk on-off indicator.

While Dutch TTF Gad and Wheat make repeat entries in the overbought category.

Lean Hogs broke their 5 week losing streak.

Soybeans broke its 5 week winning streak.

Rubber & Biodiesel are in 5 week winning streaks.

U.S. Midwest Hot Rolled Coil Steel had an outside bearish week.

Orange Juice fell 8% giving up a part of the 27% advance seen in the prior 3 weeks.

And Lithium Hydroxide has now spent 46 consecutive weeks in weekly oversold territory.

Currencies were quite active for the 2nd consecutive week.

The Aussie rose agains most, but it didn’t quite make a new high versus the Japanese Yen.

The CHF rose versus the Aussie which reflected the ‘risk-off’ stance for the week.

The Loonie eeked out some gains.

The DXY Index was flat.

The Euro slightly weaker, while the anomaly in the strength in the EUR/GBP, which is now overbought.

The GBP/JPY is in a 4 week winning streak.

We are seeing new weakness in the Philippine Peso against the USD, which is now in a 4 week losing streak.

And the Yen was mostly weaker, again.

The larger advancers over the past week comprised of;

Australian Coking Coal 4.2%, Cocoa 12.1%, China Coking Coal 3.9%, Robusta Coffee 5.9%, Oats 3.1%.

The group of largest decliners from the week included;

Cotton (5.4%), Iron Ore (1.7%), Copper (3.2%), Heating Oil (1.9%), U.S. Hot Rolled Coil Steel (1.8%), Lumber (4.1%), Natural Gas (6.1%), Nickel (2.8%), Orange Juice (8.3%), Palladium (7.3%), Gasoline (2.1%), Uranium (3.2%), Gold in CHF (1,6%), Corn (4%), Rice (3.7%), Soybeans (3.5%), Wheat (2.7%), HSCEI (3.2%), Hang Seng (2.8%), BOVESPA (1.8%), Indonesia (4.1%), MOEX (5.3%), KOSPI (1.9%), Nasdaq 100 (1.4%), NIFTY (1.9%), PSE (3.8%), South Africa 40 (3.2%), SENSEX (1.9%), SOX (1.9%), Chile (2.1%), TAIEX (1.8%) and BIST fell 2.6%.

And for some reference for Australian readers, the ASX 200 fell 0.3%, ASX Small Caps rose 0.4% and the S&P 500 fell 0.5% for the week.

June 2, 2024

by Rob Zdravevski

rob@karriasset.com.au

May 31, 2024 Leave a comment

Shares in #Accenture have just registered their 5th moment of being ‘oversold’ (on a weekly basis) in the past 20 years.

#ACN

May 31, 2024

May 29, 2024 Leave a comment

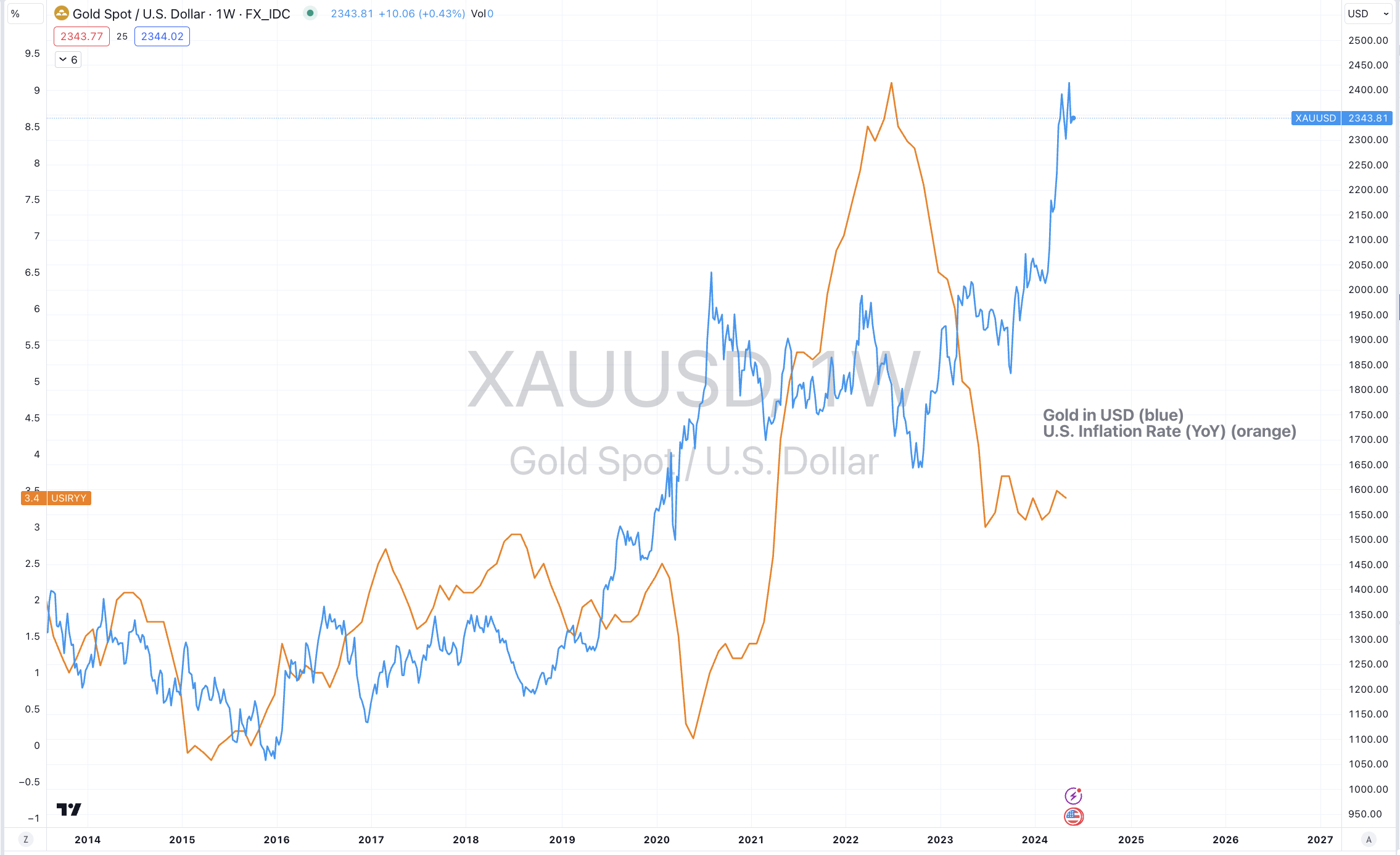

I recall ‘gold bugs’ commonly telling us that owning Gold is a hedge against inflation and a weak economy and stock market.

Lately, that story hasn’t been applicable.

Just keep this in mind when the next time that the financial media try to frame it as so.

May 29, 2024

by Rob Zdravevski

rob@karriasset.com.au

May 29, 2024 Leave a comment

I am still finding many publicly listed companies around the world whose net interest expense is greater than 40% of their EBIT.

Ah, the fine edge of leverage.

I think that the cost of money won’t abate enough to provide relief that the overly indebted would hope.

May 28, 2024 Leave a comment

When the blue line (the U.S. 10 year yield minus the 10 year breakeven inflation rate) trades above and to some considerable percentage above its 200 week moving average, it results in the S&P 500 either peaking or stifling any further advance.

I think it’s a dangerous equity market.

May 28, 2024

by Rob Zdravevski

rob@karriasset.com.au

May 26, 2024 Leave a comment

A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) either registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

* denotes multiple week inclusion

Extremes above the Mean (at least 2.5 standard deviations)

Copper/Gold Ratio *

Bloomberg Commodity Index

Copper

JKM LNG in USD and JPY

Nickel *

Platinum *

Dutch TTF Gas

Wheat *

AUD/SGD

Helsinki *

South Africa 40

And the ASX Materials Index

Overbought (RSI > 70)

Japanese 2, 5 and 10 year government bond yield *

Tin

AEX *

Austria’s ATX *

Malaysia’s KLSE *

Pakistan’s KSE Index *

Oslo *

Stockholm

TAEIX *

and Turkiye’s BIST 100 *

The Overbought Quinella (Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Nickel on MCX

Orange Juice

Extremes below the Mean (at least 2.5 standard deviations)

Australian 10 year minus Australian 2 year government bond yield spread

CAD/EUR

CAD/GBP

USD/ZAR

Oversold (RSI < 30)

North European Hot Rolled Coil Steel *

Lumber *

Lithium Hydroxide *

Sugar

The Oversold Quinella (Both Oversold and Traded at < 2.5 standard deviations below the weekly mean)

None

Notes & Ideas:

Government bond yields rose, mostly.

It was another week of relative quiet action.

The Russian 10 year government bond yield isn’t overbought anymore.

And the U.S. 10 year inflation breakeven rate, mean reverted.

Equities were mainly weaker.

The Hang Seng Index and S&P Small Cap 600 aren’t overbought anymore.

Many other equity indices also dropped out of their overbought extremes.

The KBW Bank Index, Vietnam, CSI 300 and Shanghai Index all broke their weekly winning streaks.

The Nasdaq Composite, KLSE, FTSE 250, Nasdaq 100, S&P 500 and TAEIX have all put together a 5 week winning streak.

Pakistan’s KSE has risen for 9 of the past 10 weeks.

The Philadelphia Semiconductor Index (SOX) has risen 10% over the past 3 weeks.

Oslo is at an all-time high.

And the HSCEI and Indonesia’s IDX had a weekly outside bearish week.

Commodities were mostly stronger.

Cotton, Coffee, JKM LNG, Cocoa and Wheat all had a good week.

Nickel as traded on India’s MCX makes a return to registering an overbought extreme.

Oil & Distillates, Copper, Palladium, Platinum, Silver and Gold all saw weakness.

Tin returns to overbought territory.

Silver and Gold (in all currencies except the CHF) are no longer overbought.

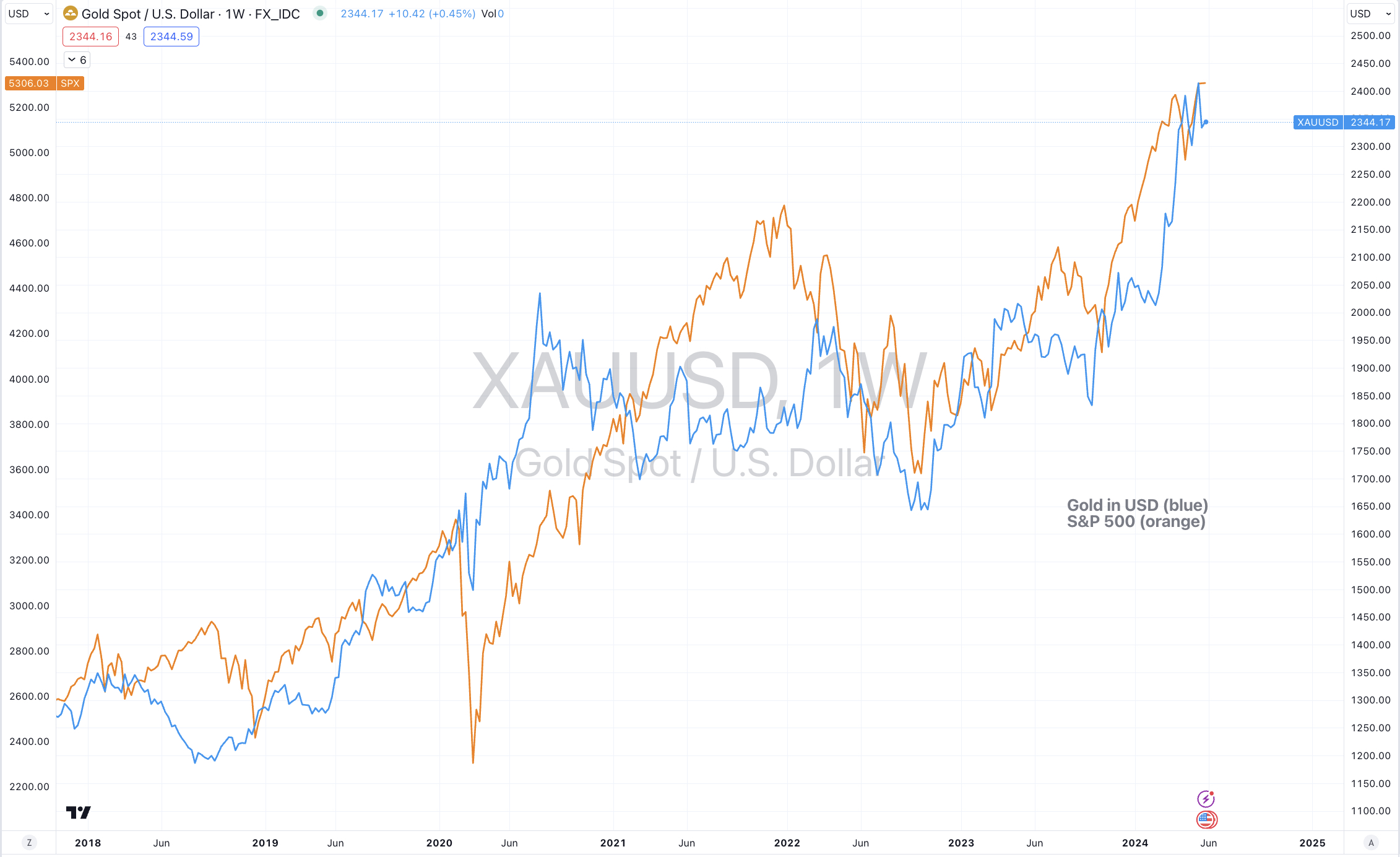

In fact, Gold performed a bearish outside reversal week.

Lean Hogs are in a 5 week losing streak.

Orange Juice has risen 27% over the past 3 weeks.

Soybeans are in a 5 week winning streak.

Cotton rose and broke its 11 week losing streak.

And Lithium Hydroxide has now spent 45 consecutive weeks in weekly oversold territory.

Currencies saw some action during the week.

The British Pound was stronger and nearing extreme against the JPY and EUR.

The Yen was mostly weaker.,

The Aussie was weaker against all except the Thai Baht and South African Rand.

The Euro as mixed while the Loonie was weaker.

The larger advancers over the past week comprised of;

Aluminium 2.4%, Cocoa 12.9%, Cotton 6.1%, JKM LNG 7%, Coffee 5.6%, JKM LNG in Yen 13.9%, Tin 2.7%, Nickel in MCX 4%, Orange Juice 6.3%, Robusta Coffee 10.6%, Corn 2.7%, Oats 3%, Wheat 7.1%, Egypt 4.1%, NIFTY 2%, SENSEX 2%, Chile 1.8% and the SOX rose 4.8%.

The group of largest decliners from the week included;

Baltic Dry Index (2.6%), WTI Crude Oil (2.3%), Lean Hogs (2.3%), Copper (5.9%), Heating Oil (2.8%), Nickel (4.1%), Palladium (4%), Platinum (4.7%), Gasoline (3.5%), Sugar (2.4%), Brent Crude Oil (2.1%), Gasoil (3.1%), Silver in AUD (2.7%), Silver in USD (3.6%), Gold in AUD (2.4%), Gold in CAD (3%), Gold in EUR (3.1%), Gold in GBP (3.6%), Gold in USD (3.3%), Rice (2.2%), Shanghai (2.1%), CSI 300 (2.1%), KBW Banks (2.3%), China A50 (2.6%), DJ Industrials (2.3%), DJ Transports (2.7%), MIB (2.6%), HSCEI (4.8%), Hang Seng (4.8%), BOVESPA (3%), IDX (3%), MOEX (3%), KRE Regional Banks (4.4%) and Mexico fel 3.8%.

And for some reference for Australian readers, the ASX 200 and ASX Small Caps fell 1.1%, the ASX Materials fell 1.5% while the ASX Industrials rose 0.9% for the week.

May 26, 2024

by Rob Zdravevski

rob@karriasset.com.au

May 20, 2024 Leave a comment

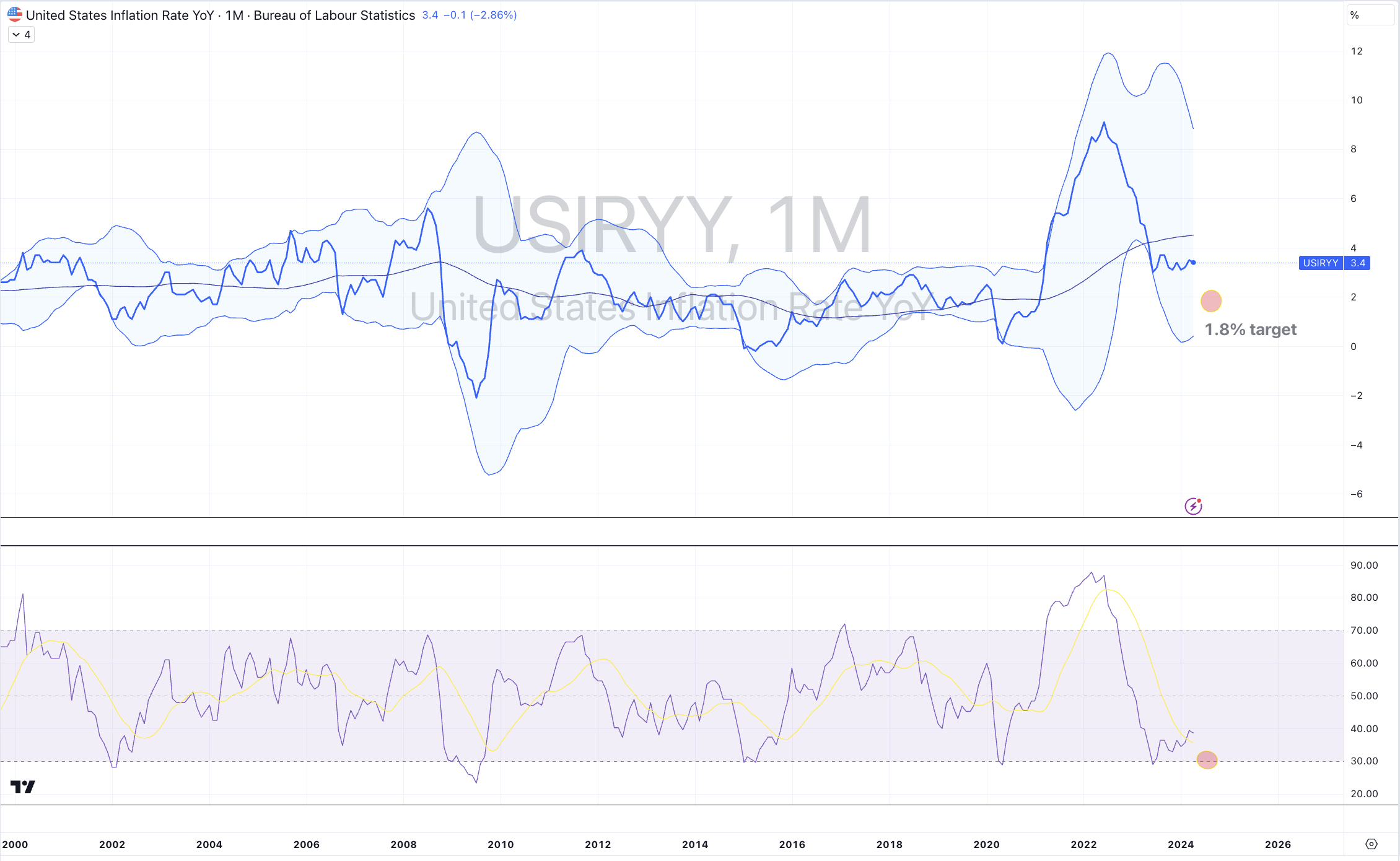

I think U.S. inflation can still decline to the 1.8% mark, somewhere around October 2024……

and all that comes with that for interest rates, commodity prices, growth equities and/or commercial real estate.

May 20, 2024

by Rob Zdravevski

rob@karriasset.com.au

For my past quips, search “inflation” at https://robzdravevski.com/?s=inflation

May 19, 2024 Leave a comment

A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) either registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

* denotes multiple week inclusion

Extremes “above” the Mean (at least 2.5 standard deviations)

Copper/Gold Ratio

Nickel

Platinum

Wheat

AUD/CAD

AUD/JPY

HKD/USD

Hang Seng Index *

S&P Small Cap 600

Helsinki *

And Switzerland’s SMI

Overbought (RSI > 70)

Russian 10 year government bond yield *

Japanese 2 and 5 year government bond yield *

Silver in AUD

Gold in CAD, CHF, EUR, GBP & USD *

AEX *

Austria’s ATX *

Budapest *

DAX *

MIB *

MOEX

Malaysia’s KLSE *

Pakistan’s KSE Index *

Oslo *

Russell 2000

South Africa 40 *

TAEIX *

TSX

FTSE 100

and Turkiye’s BIST 100 *

The Overbought Quinella (Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Copper *

Orange Juice

Silver in USD

Hang Seng China Enterprises Index (HSCEI) *

Extremes “below” the Mean (at least 2.5 standard deviations)

USD/ZAR

Oversold (RSI < 30)

Cotton

Lithium Hydroxide *

Lumber *

North European Hot Rolled Coil Steel *

Urea (Middle East)

The Oversold Quinella (Both Oversold and Traded at < 2.5 standard deviations below the weekly mean)

None

Notes & Ideas:

Government bond yields were lower.

Amongst the week’s relative quiet action, the Copper/Gold Ratio entered overbought terrority which tends to coincide with bonds yields peaking.

Equities were higher again.

The FTSE 100 switches places in oversold land with the FTSE 250.

The American Russell 2000 and S&P SmallCap 600 return to being overbought as has Toronto’s TSX.

Many European indices remain overbought as some of the China and Hong Kong indices.

The HSCEI and Hang Seng have both risen 19% in the past 4 weeks.

The All Word Developed (ex USA) Index is in a 4 week winning streak as it the Dow Jones Industrials and the Nasdaq Composite.

And Italys MIB made an all-time high.

Commodities were mostly stronger.

Coal, Cocoa, Lumber, Sugar, Oats and Grains were weaker.

Metals (Precious and Base), Gases, Oil, Coffee, Cattle and Orange Juice were stronger.

Platinum, Nickel and Orange Juice make a return visit to overbought territory.

Oats are no longer oversold as they broke their 5 week winning streak falling 11% for the week (whilst performing a weekly outside bearish reversal), giving up nearly half of their 26.5% return over that time.

Copper, Silver and Gold are overbought, while Hot Rolled Coil Steel, Lumber and Cotton and Lithium are in the oversold category.

Lumber has tanked 22% over the past 8 weeks and Cotton has slumped for 11 consecutive weeks.

Most grains eased following 4 weeks of consecutive gains.

Over the past 3 weeks, Platinum has risen 17%.

The Baltic Dry Index fell 13%, giving up half of the 23% gain seen in the prior fortnight.

And Lithium Hydroxide has now spent 44 consecutive weeks in weekly oversold territory.

Currencies saw some action during the week.

The AUD was stronger and as some pairs return to be ing overbought.

And interestingly, the CHF/AUD is nearing overbought territory.

The larger advancers over the past week comprised of;

Aluminium 1.8%, Bloomberg Commodity Index 2.9%, WTI Crude Oil 2.3%, Copper 8.3%, Heating Oil 2.1%, JKM LNG 4.5%, Coffee 2.7%, Cattle 2.7%, JKM LNG in Yen 1.8%, Tin 2.4%, LME Aluminium 3.6%, Natural Gas 16.6%, Nickel 11.9%, Nickel on MCX 3.2%, Orange Juice 13.8%, Palladium 3%, Platinum 8.2%, Gasoline 2.7%, Robusta Coffee 2.3%, Dutch TTF Gas 2.5%, Silver in AUD 10.3%, Silver in USD 11.8%, Gold in CAD 1.9%, Gold in CHF 2.6%, Gold in USD 2.3%, ASX 200 1.7%, MIB 2.1%, HSCEI 3.2%, HSO 3.1%, IBEX 2%, IDX 2.5%, Russell 2000 1.9%, Nasdaq Composite 2.1%, KSE 3.1%, Nasdaq Biotech 2.4%, Nikkei 225 2.1%, Copenhagen 2.7%, SENSEX 1.7%, SMI 2.4%, SOX 3.6%, S&P 500 1.5%, TAEIX 2.7%, Vietnam 2.3%, ASX Materials 2.5% and BIST rose 4.2%.

The group of largest decliners from the week included;

Australian Coking Coal (2.5%) Rotterdam Coal (1.8%), Baltic Dry Index (13.4%), Cocoa (17.4%), China Coking Coal (2.3%), Cotton (1.8%), Lean Hogs (1.9%), Lumber (1.7%), Sugar (6.1%), Corn (3.7%), Oats (11.1%), Rice (3.2%), Wheat (1.9%), Budapest (1.6%) and the ASX Industrials fell 1.8%.

May 19, 2024

by Rob Zdravevski

rob@karriasset.com.au