A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) either registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

n.b. pricing of (commodity) futures contracts is only considering the immediate front month.

* denotes multiple week inclusion

Extremes above the Mean (at least 2.5 standard deviations)

Cattle

India’s NIFTY

And the ASX Industrials equity index

Overbought (RSI > 70)

U.S. 10 year minus U.S. 5 year bond yield spread *

Urea (U.S. Gulf price) *

Hungary’s BUX index

Spain’s IBEX index

Czechia’s PX Index *

and Chile’s IGPA and IPSA equity indices *

The Overbought Quinella (Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Tel Aviv 25 equity index *

Extremes below the Mean (at least 2.5 standard deviations)

None

Oversold (RSI < 30)

Indian 10 year government bond yield *

Richards Bay Coal *

Lumber

Lithium Carbonate *

Lithium Hydroxide *

Newcastle Coal

The Oversold Quinella (Both Oversold and Traded at < 2.5 standard deviations below the weekly mean)

None

Notes & Ideas:

Government bond yields rose again, again.

Italian 2 year bond yields have risen for 4 weeks.

Brazilian and Indonesian 10 year yields broke their 4 straight weeks of decline.

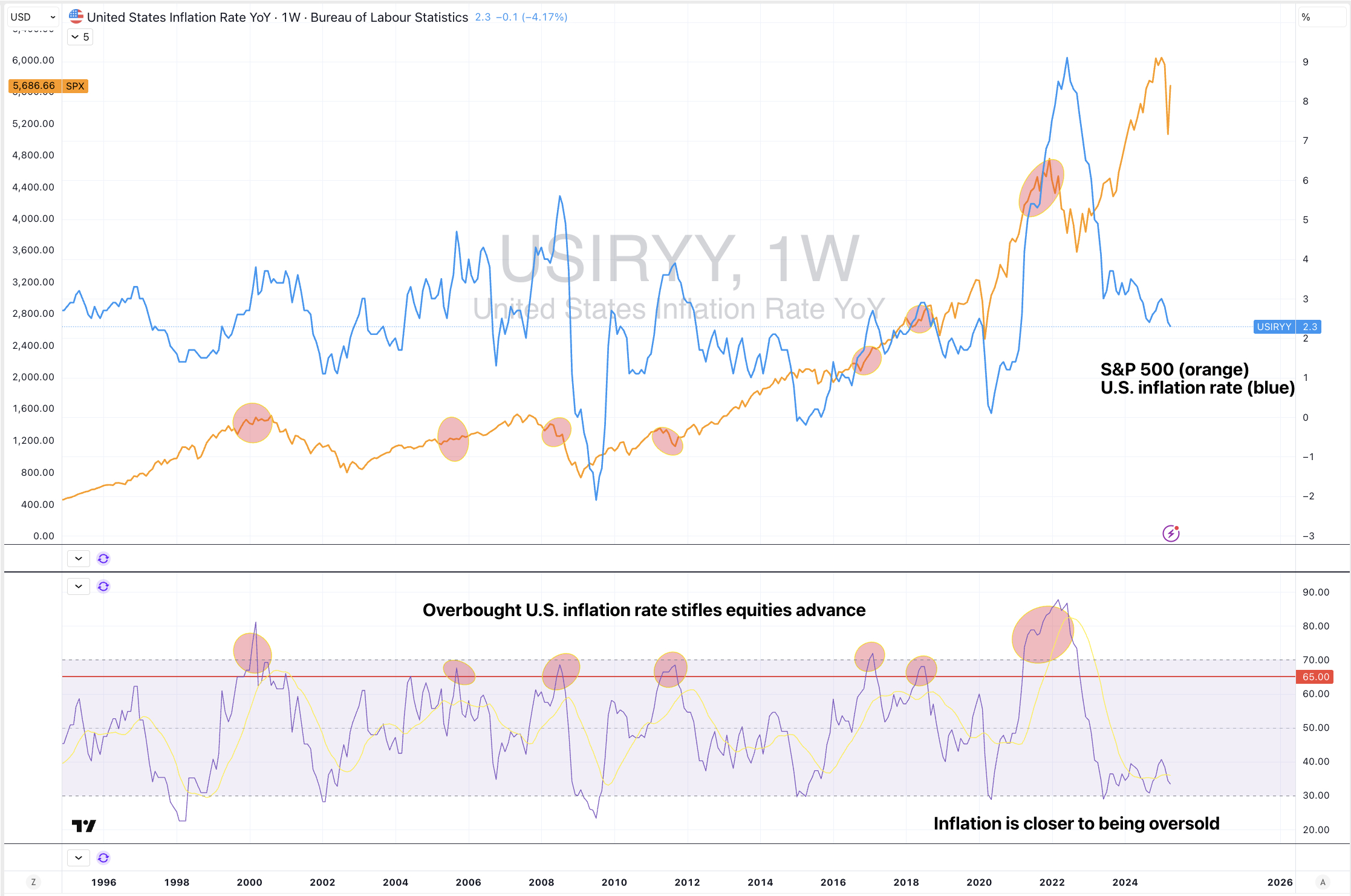

U.S. 10 year yield minus U.S. 10 year inflation rate is nearly overbought.

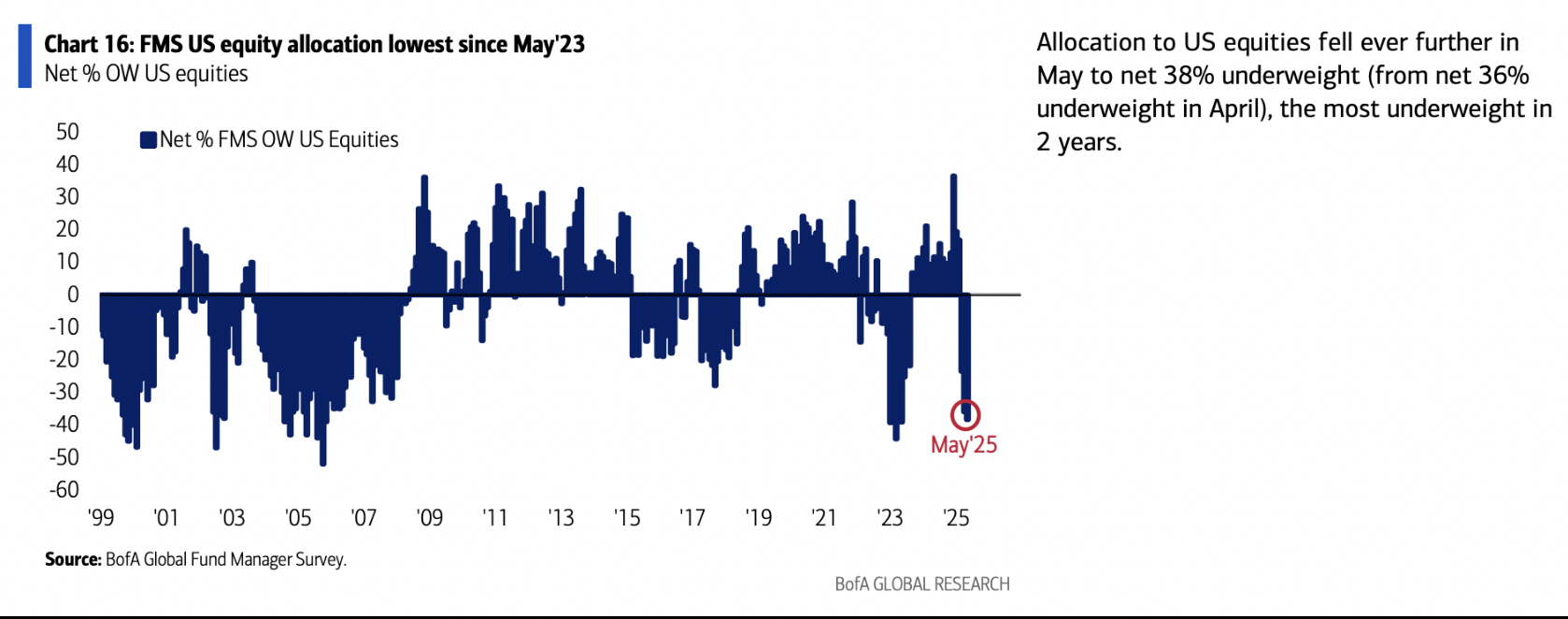

Equities had a tremendous week.

Several indices are overbought and many streaks are in progress.

The TAEIX, SOX and Nasdaq Transports have risen for 4 consecutive weeks.

The AEX, ATX, DAX, MIB, HSCEI, Hang Seng, IBEX, KLSE, KRE Regional Banks, KOSPI, OMX Helsinki, PSE, Strait Times, IDX and the ASX Materials and Industrials have climbed for 5 straight weeks.

The Bovespa, S&P SmallCap 600, Russell 2000, FTSE 250, IPSA, S&P MidCap 400, ASX SmallCaps, TSX and KBW Banks Index are in 6 week winning streaks.

Israel’s TA35 broke its 4 week winning streak.

SET, WIG and the ASX SmallCaps broke their 5 weeks of consecutive advance.

The Dow Jones Industrials has risen 5 of the past 6 weeks.

Commodities were mixed.

The largest winners were Oils & Distillates, Gases (again), Cocoa, Orange Juice, Lumber and Tin.

The notable losers included Coal, Cotton, Coffee, Natural Gas, Silver and Gold.

Heating Oil has risen 7.5% over the past 2 weeks.

Lumber left oversold territory as did Gold across as priced against all currencies.

Gold prices are at their lowest close since April 10th.

Newcastle Coal returned to being oversold.

Rubber & Cattle broke its 4 week winning streak.

Uranium has risen for 5 week straight streaks.

Rice & Wheat broke a 4 week losing streak.

Corn has declined 12% during its 5 week losing streak.

And U.S. Gulf Urea prices broke their 5 straight weeks of advance.

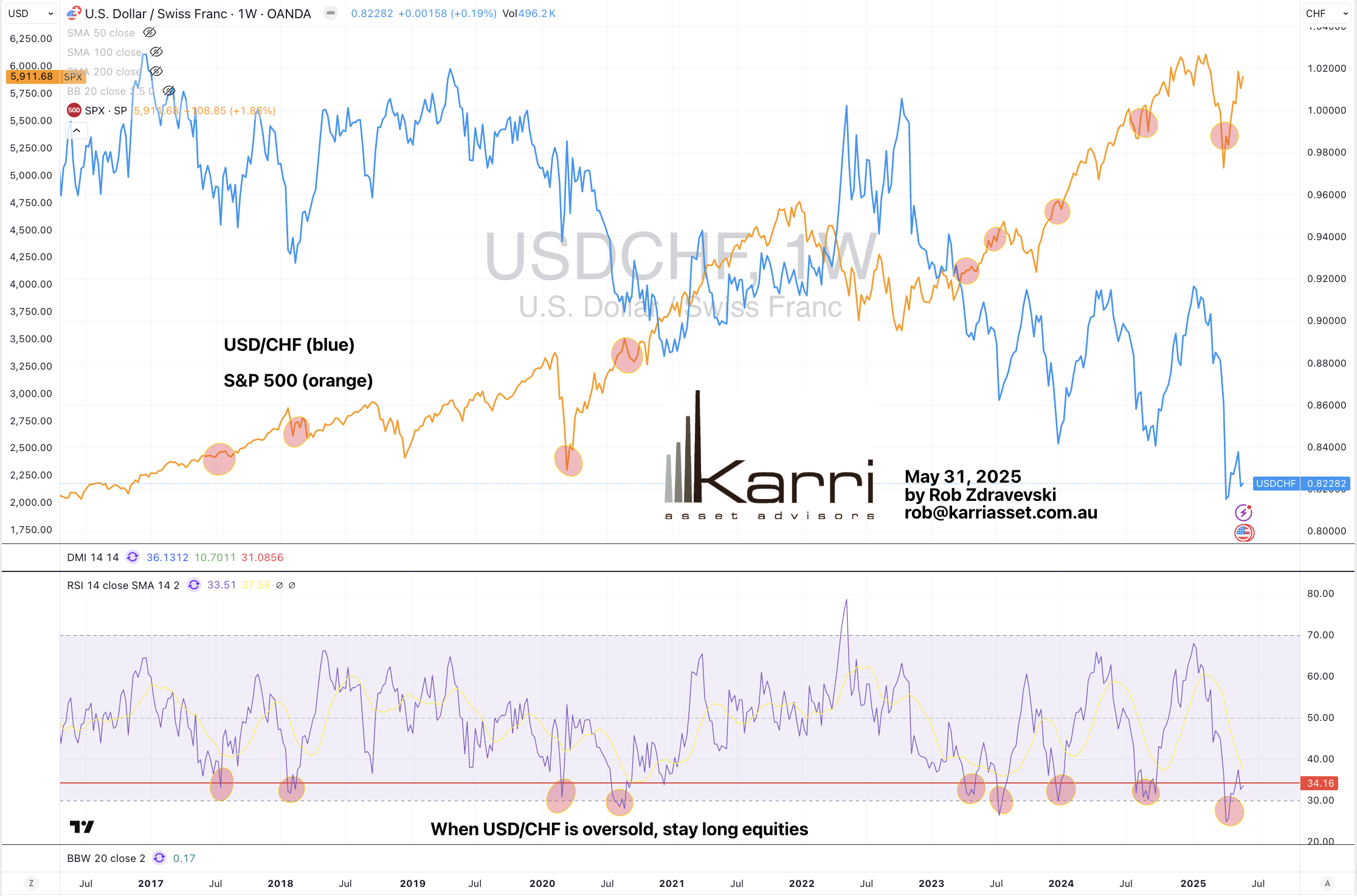

Currencies were subdued, but there are many streaks in play.

All the currencies which appeared as extremes in last week’s list, are no longer so.

The British Pound was mixed, Yen flat, Aussie firmer and Euro weaker.

The U.S. Dollar (DXY) Index has risen for 4 weeks.

AUD/CAD, AUD/CHF and AUD/EUR are in a 6 week winning streak.

AUD/CHF and the GBP/JPY have risen for 5 weeks.

While on the losing streaks, the USD/ZAR has declined for 6 consecutive weeks.

The AUD/ZAR has fallen for 5 straight weeks.

CHF/AUD and the EUR/GBP are in 5 week losing streaks.

BRL/USD broke its 4 weeks of advance against the USD.

PHP/USD broke its 5 week winning streak.

The larger advancers over the past week comprised of;

Aluminium 3.5%, Baltic Dry Index 6.9%, Brent Crude 2.2%, Cocoa 18.6%, WTI Crude 2.4%, Lean Hogs 2.8%, Heating Oil 3.7%, Lumber 5.2%, Tin 2.8%, Orange Juice 9.8%, Gasoline 1.3%, Dutch TTF Gas 1.6%, Gasoil 3%, Uranium 1.9%, ATX 3%, AEX 2.8%, KBW Banks 6.5%, BUX 3.2%, CAC 1.9%, China A50 1.7%, DJ Industrials 3.4%, DJ Transports 8%, MIB 3.3%, HSCEI 1.9%, Hang Seng 2.1%, BOVESPA 2%, IDX 4.5%, S&P SmallCap 600 4.7%, Russell 2000 4.5%, TAEIX 4.4%, Nasdaq Composite 7.2%, KLSE 1.6%, KRE Regional Banks 4.7%, KSE 11.6%, KOSPI 1.9%, FTSE 250 2.3%, S&P MidCap 400 4.9%, Mexico 2.5%, Nasdaq Biotech 4.1%, Nasdaq 100 6.8%, Oslo 4%, Copenhagen 4%, Helsinki 3.4%, Stockholm 3.9%, PX 2.1%, SENSEX 3.6%, SMI 2.1%, SOX 10.2%, IGPA 1.9%, S&P 500 5.3%, Nasdaq Transports 7%, TSX 2.4%, Vietnam 2.7%, ASX 200 1.4%, ASX Materials 2.6%, ASX Industrials 1.*%, BIST 3%, IBB 3.9% and Nasdaq Biotechs 3.4%.

The group of largest decliners from the week included;

Richards Bay Coal (1.6%), Bloomberg Commodity Index (1.8%), Cotton (2,6%), Arabica Coffee 5.7%), Newcastle Coal (2.3%), Natural Gas (12.2%), Palladium (2.2%), Robusta Coffee (6.9%), Sugar (1.5%), Rubber (1.7%), Silver (1.3%), Gold in AUD (3.5%), Gold in CAD (3.5%), Gold in CHF (2.9%), Gold in EUR (3%), Gold in GBP (3.5%), Gold in USD (3.8%), Gold in ZAR (4.6%) and Corn fell 1.4%.

May 18, 2025

By Rob Zdravevski

rob@karriasset.com.au