A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) either registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

n.b. pricing of (commodity) futures contracts is only considering the immediate front month.

* denotes multiple week inclusion

Extremes above the Mean (at least 2.5 standard deviations)

SHY

MYR/USD

Mexico’s IPC equity index

Overbought (RSI > 70)

U.S. 30 year minus U.S. 10 year bond yield spread *

Gold in AUD, CAD, USD and ZAR *

Chile’s IGPA and IPSA equity indices

The Overbought Quinella (Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

U.S. 10 year minus U.S. 5 year bond yield spread *

Urea (U.S. Gulf price) *

PHP/USD *

Extremes below the Mean (at least 2.5 standard deviations)

Brent and WTI Crude Oil

S&P GSCI (commodities) Index

USD/INR

USD/SGD

Oversold (RSI < 30)

Australian 2 year government bond yield *

Indian 10 year government bond yield *

Richards Bay Coal *

Lithium Carbonate *

Lithium Hydroxide *

Newcastle Coal *

USD/SEK *

The Oversold Quinella (Both Oversold and Traded at < 2.5 standard deviations below the weekly mean)

None’

Notes & Ideas:

Government bond yields rose with her exception of Belgium, Brazil and the Japanese curve.

In fact, Brazilian 10’s are approaching overbought territory .

European (German) 10 year yields rose and broke their 6 weeks of decline.

South Korean 10’s and Chilean 2’s ended their 4 weeks of lower travel.

Norwegian & Indian 10 year yields are in a 7 week declining streak.

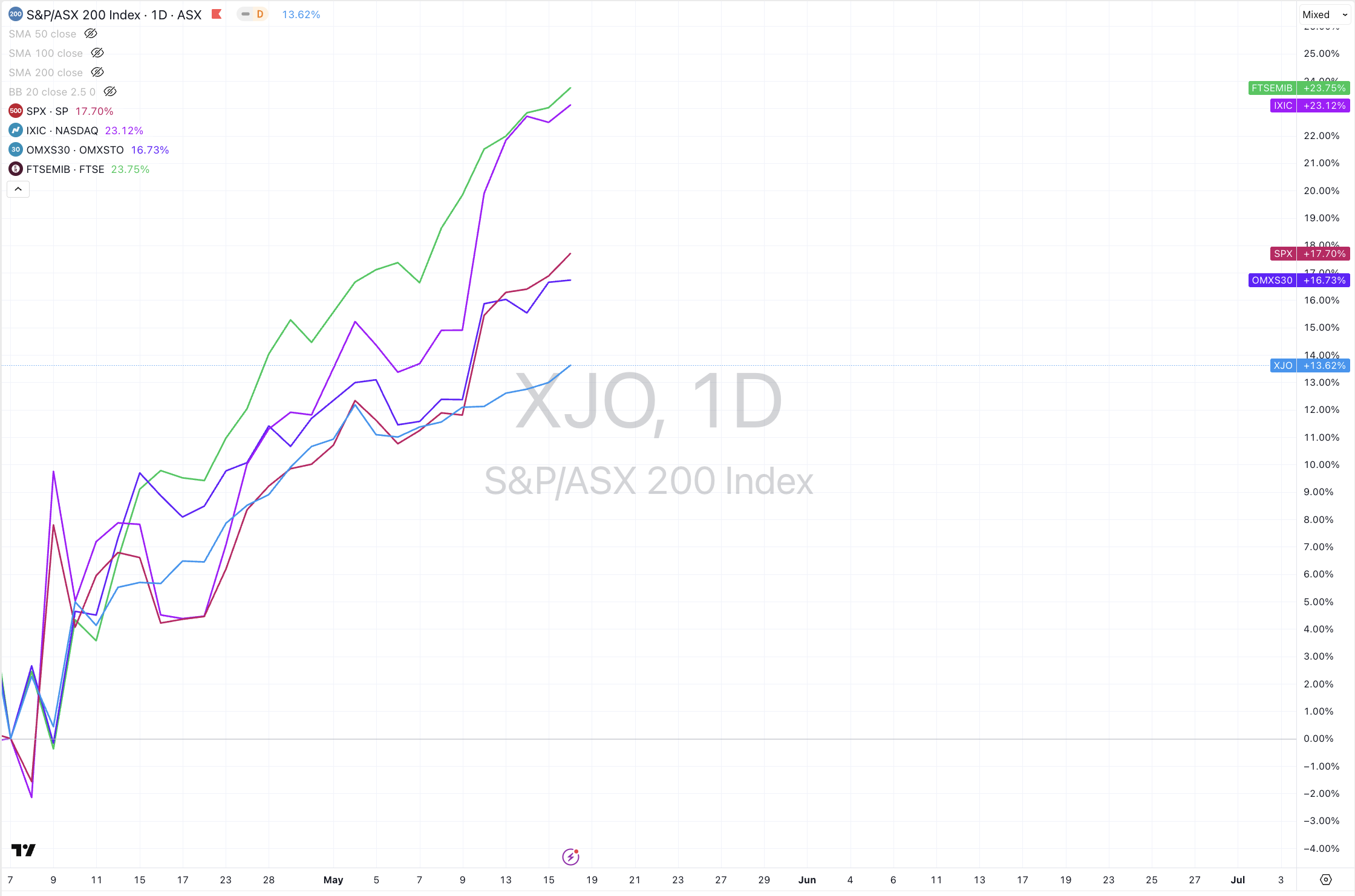

Equities rose, everywhere, again.

The Netherland’s, Norway’s, Thailand’s, Canada’s, Poland’s main equity indices are in 4 week rising streaks.

As are the KBW Banks, the ASX’s Small Caps and Industrials along with some U.S. biotech indices.

Over the past 4 weeks, various indices have risen between 8%-13%.

Transportation indices and Thailand’s SET Index are no longer oversold.

Commodities were mostly lower.

The largest winners were Coals, Gases, Urea, Shipping Rates, Palladium and Uranium.

The notable losers included Oils & Distillates, Tin, Sugar Copper, Cocoa, Silver, Lumber and Coffee.

The big news is seeing Crude Oil prices return to oversold extremes.

Gold prices fell and those priced in USD, GBP and EUR left overbought territory.

Natural Gas broke its 4 week losing streak.

U.S. Gulf Urea prices have risen for 5 straight weeks and has climbed to prices not seen since November 2022.

North European Hot Rolled Coil Steel & Rubber are no longer oversold,

while Lithium Hydroxide has been oversold territory for 100 consecutive weeks.

Currencies were quiet, for a change of pace.

Continuing last weeks trend, many more currency pairs are not at extremes.

Commensurate with the ‘risk-on’ environment, the Aussie rose while the Yen and Swissie fell.

U.S. (DXY) Dollar Index rose and moved out from oversold territory.

The Aussie was stronger again and is in a 4 week rising streak against the Loonie, Euro and USD.

The Loonie was firmer.

The CAD/AUD has fallen for the past 4 weeks.

The Euro fell,

And the JPY/AUD is in a 4 week losing streak.

The larger advancers over the past week comprised of;

Richards Bay Coal 1.6%, Rotterdam Coal 2.1%, Baltic Dry Index 3.5%, North European Hot Rolled Coil Steel 1.7%, Newcastle Coal 3.6%, Natural Gas 16.6%, Palladium 1.6%, Dutch TTF Gas 1.8%, U.S. Gulf Urea 4.3%, Uranium 4.4%, All Developed World – ex USA 2.9%, AEX 2.8%, KBW Banks 4.3%, CAC 3.1%, DAX 3.8%, DJ Industrials 3%, DJ Transports 4.3%, MIB 2.6%, HSCEI 1.9%, IDX 5.6%, S&P SmallCap 600 3.2%, Russell 2000 3.3%, TAEIX 4.6%, Nasdaq Composite 3.4%, KLSE 2.2%, KRE Regional Banks 4.2%, FTSE 250 3.2%, S&P MidCap 400 3.6%, Nasdaq Biotechs 3.3%, Nasdaq 100 3.5%, Nikkei 225 3.2%, Oslo 3.7%, Copenhagen 7%, Helsinki 3.9%, PSI 2.3%, Sensex 1.6%, SET 3.5%, SMI 2.6%, S&P 500 2.9%, FTSE 100 2.2%, ASX Financials 3.3%, ASX 200 3.4%, Nasdaq Transports 2.9%, ASX Industrials 2.6%, ASX SmallCaps 3%, IBB biotech ETF 2.7%, XBI biotech ETF 4.2% and the Philadelphia SOX Index rose 3.4%.

The group of largest decliners from the week included;

Australian Coking Coal (1.6%), Brent Crude Oil (6.9%), Cocoa (5.5%), WTI Crude Oil (7.5%), Lean Hogs (1.8%), Copper (4.4%), Heating Oil (5.6%), Arabica Coffee (3.6%), Lumber (3.9%), JKM LNG in Yen (3.5%), Lithium Carbonate (.2%), Tin (6.5%), Gasoline (4.1), Robusta Coffee (2.3%), Sugar (5%), Sugar #16 (2.5%), SPGSCI (3.2%), CRB Index (2.7%), Gasoil (6.8%), Middle East Urea (1.9%), Silver in AUD (4%), Silver in USD (3.3%), Gold in AUD (3.1%), Gold in CAD (2.6%), Gold in CHF (2.5%), Gold in Euro (1.8%), Gold in GBP (2.1%), Gold in USD (2.4%), Gold in ZAR (3.9%), Corn (4%), Oats (5.7%), Rice (2.8%), Palm Oil (4.3%) and Turkiye’s BIST Index fell 2.8%.

May 4, 2025

By Rob Zdravevski

rob@karriasset.com.au