The following assets (on a weekly timeframe) registered an Overbought reading or traded more than 2.5 standard deviations above its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations)

Coffee

Sugar

Italian Government 10 Year Bond Yields

Overbought (RSI > 70)

Canadian 10 year bond yields (for 11th consecutive weeks)

German, French, Korean Government 10 year bond yields

along with the U.S. 5 and 10 year bond yields

The Copper/Gold Ratio

The Commodities Indices (the CRB and Bloomberg’s)

Iron Ore (for the 3rd consecutive week)

Aluminium (for 10 consecutive weeks)

Copper (for the 20th consecutive weeks)

Lean Hogs (for the 11th consecutive week and its highest price since July 2014)

S&P 500 Index (for the 4th consecutive week)

Dow Jones Industrial Average (for the 4th consecutive week)

S&P Mid Cap 400 (8th consecutive week)

U.S. KBW Banking Index (9th consecutive week)

Nasdaq Transportation Index (8th consecutive week)

Dow Jones Transport Index (8th consecutive week)

Sweden’s OMX 30 Equity Index (9th consecutive week)

France’s CAC-40 Equity Index (for the 3rd consecutive week)

Ethereum

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

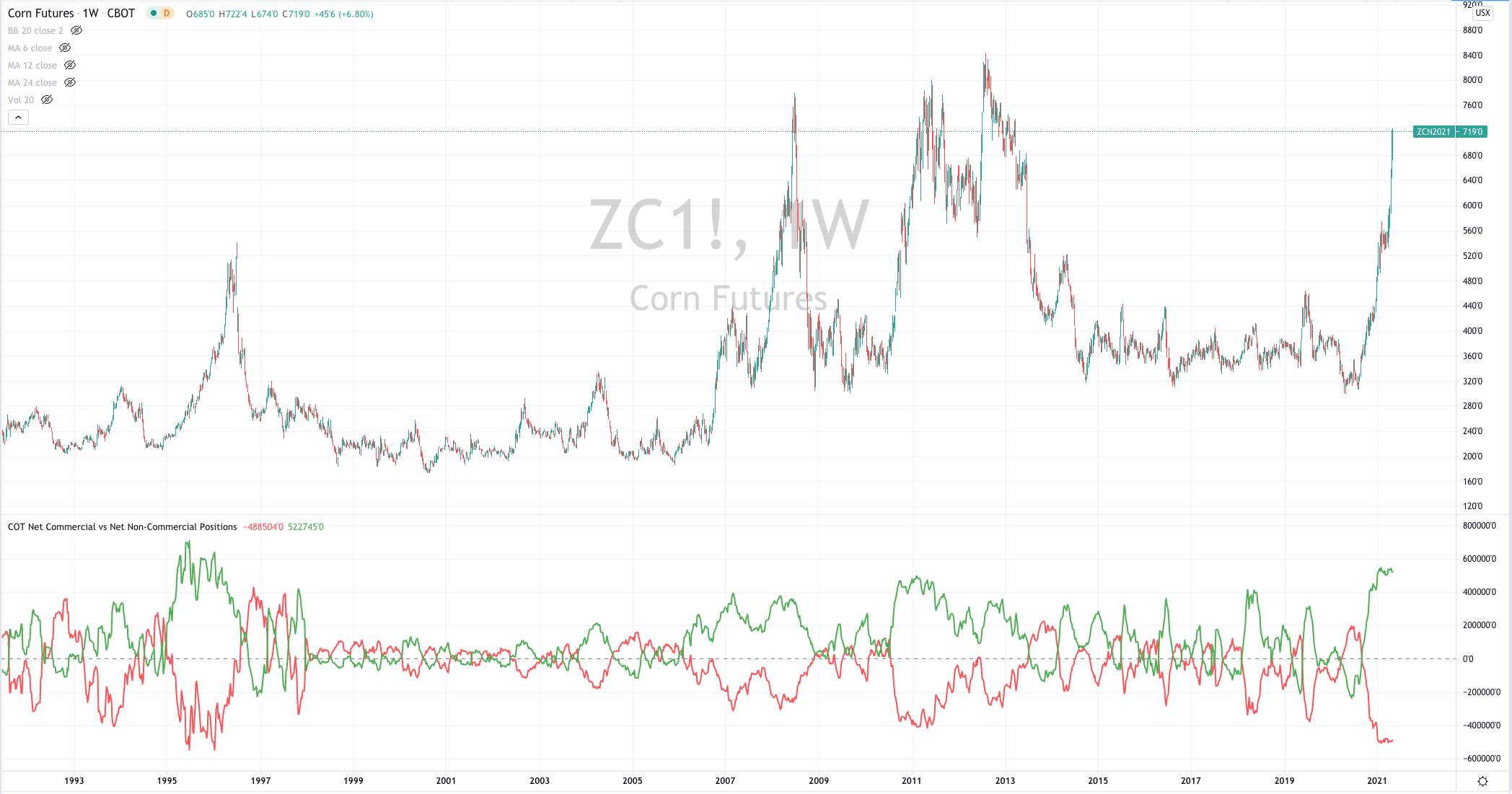

Corn (for the 21st consecutive week & trading 73% above its 200 Week Moving Average)

Soybeans (overbought for 8 consecutive weeks & 73%> its 200 Week Moving Average)

Lumber (having risen 55% in past 6 weeks)

Wheat

Cryptocurrencies Dogecoin, Ripple (XRP) & Monero

Assets (securities) within my immediate universe which touched the other side of the extreme, being Oversold (where the RSI is < 30) or were at least 2.5 standard deviations below its mean are;

Extremes “below” the Mean (at least 2.5 standard deviations)

Nil

Oversold (RSI < 30)

Nil

The Oversold Quinella – Both Oversold and Traded at < 2.5 standard deviations above the weekly mean)

USD/CAD

(meaning sell your strong Canadian Dollars against the weaker U.S. Dollar)

Notes & Ideas:

The ‘softs’ have continued their rise, more so this past week.

Another notable occurrence is the return of Government 10 Year Bond Yields to the Overbought side of the ledger.

On the equities front, the U.S indices continue to linger in overbought territory as does France’s CAC-40, while the ASX 200 has eased lower from its standard deviation stretch.

The only currency registering an extreme is the strong Canadian Dollar vs. the USD, which coincides with strength seen the broader Commodity Indices.

If you are wondering, the AUD/USD was last Overbought in mid-February 2021, when it traded to a high of 0.8007.

and selected cryptocurrencies remain overbought.

May 2, 2021

by Rob Zdravevski

rob@karriasset.com.au