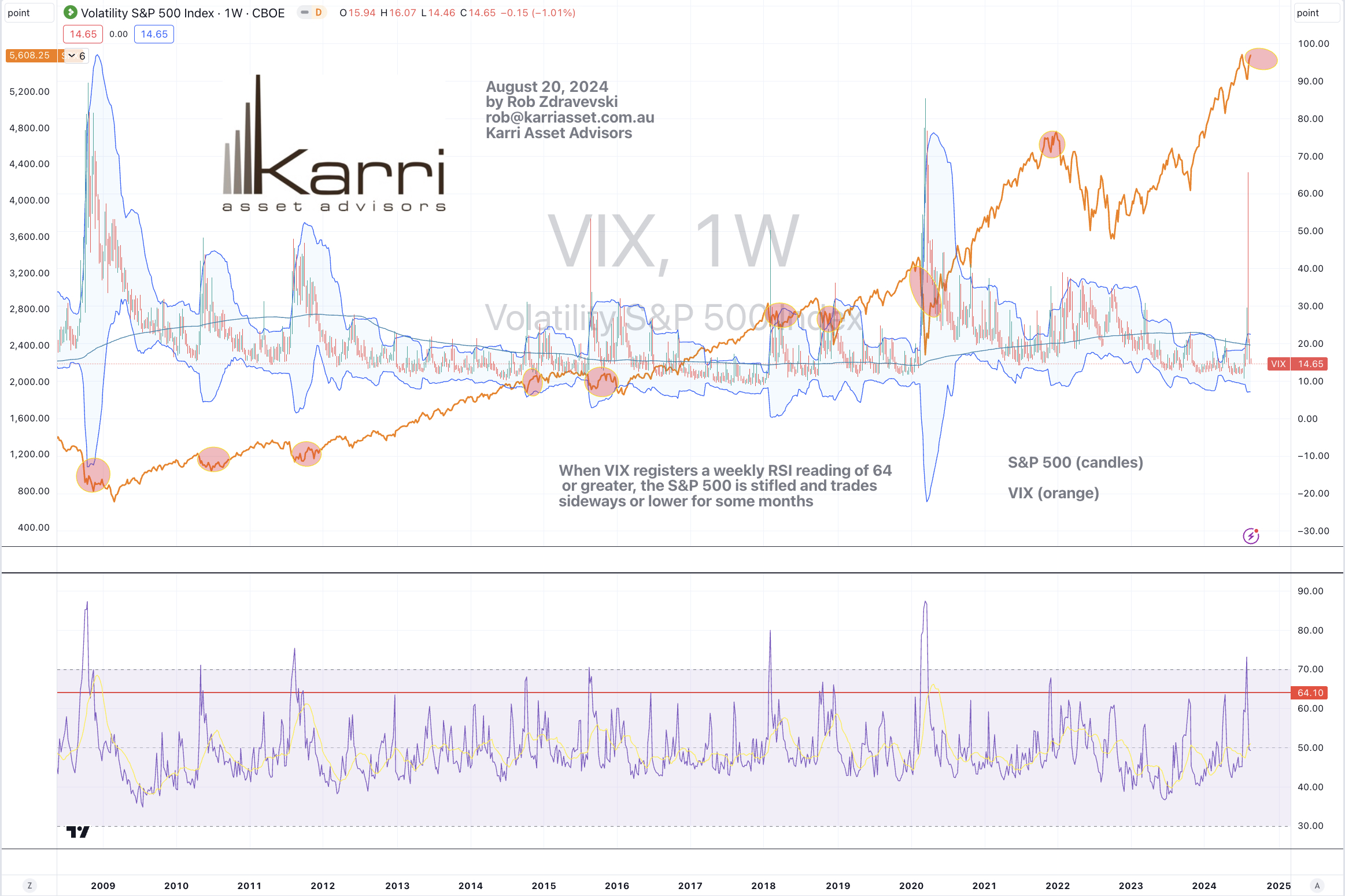

and the respondents are more bearish than last week’s result.

and the bullish/bearish spread is negative at (1.5%).

It’s the highest bearish reading since Nov 2, 2023, when the bullish/bearish spread was also negative.

The most recent moment that the bullish/bearish spread was negative was in the April 25, 2024 release.

I have highlighted those 2 moments in the attached S&P 500 price chart.

This is in keeping with my other commentary that while we are late in this particular equity ‘party’ and the VIX is subdued, it looks like equities will ‘rip’ higher.

Like any place where waves are prevalent, you need to watch out for the rips.

Last week’s palaver about unwinding Yen trades is old news.

The Yen has nearly swung to the other side of the pendulum.

The study below shows the 13 moments over the past 15 years when the AUD/JPY was trading (coinciding with a couple other metrics) at a weekly RSI reading of 36 or below.

I say ‘nearly swung’, for we are close but not there yet……for another such occurrence.

When they do occur, they bode well for listed equities risk appetite.

The Nasdaq 100 index appears within my study as a comparison.

Here is another one for the asset allocators……the S&P 500 is making its 26th visit down to a 2.5 standard deviation move within the past 35 years.

It’s been a handy long term buying moment.

p.s. Long-Term doesn’t equal 3 weeks.

Long-Term is the type of timeframe involved when you consider buying shares for a new born child and not telling them about it until they are allowed to legally buy alcohol.

Timing the entry points and wading in will be artistic part.

The chart below shows the S&P 500 (SPX) overlaid with the Copper/Gold (HG/GC) Ratio on a daily basis over the past 15 years.

The latter ratio is a good indicator of the economy’s health and sometimes a predictor of interest rate direction.

I find this chart helpful when pondering my asset allocation to equities and how much broader risk I am comfortable taking, especially at the later end of an advance, bull market or rally.

I like seeing how the SPX reacts when the HG/GC breaks above or below its trend lines.

Today’s reading of 0.002396 is calculated by dividing the Copper price of $4.32 into Gold’s $1,803.

At this moment, while the HG/GC’s is trading above its trend line (and a reading of 0.00222) it is suggesting that the S&P 500 advance remains intact……..

This seems quite perverse to many, as pundits reiterate their calls of an overvalued, ‘bubble-esque’ equities market.

In some recent posts I challenge the norm and perhaps the consensus call for a notable decline.

The S&P 500 can continue trading at the historical higher end of its historical stretch above its 200 Week Moving Average, just like the late 1990’s.

and the way the S&P 500 relates to the U.S. 10 year bond yield or more pointedly, the spread between the 10 year and 2 year yield is another important indicator to watch.

Investing is a highly nuanced past time or business.

Often markets move to where they can do the most damage….and going up can cause as much damage as going down, in circumstances such as ‘missing out’ or underperforming other fund managers if you’ve been holding a lot of cash.

P/E ratios are not the only thing to look at.

One scenario of a 0.00222 reading is Copper falling to $4.10 and Gold rising to $1,850. Just something to play around with.