Banks not only feed the piggies but they slaughter them too

October 12, 2022 Leave a comment

I keep reiterating that what is more important about where interest rates have traded up to isn’t about the nominal rate, but rather the quantum or factor which the nominal rate have risen by.

Yes, the numbers look bigger when rates are rising from 0.5%…..but people, households, companies, governments etc etc don’t necessarily temper their borrowing when rates are low…..We tend to become accustomed to the ‘going rate’.

In general, the piggies are always at the trough.

When a family is seeking a mortgage of $600,000 but their credit provider announces the good news that they have been approved for $680,000, I suspect that they accept all of the $680,000. After all, they can use it for the landscaping etc etc.

We are happy to continue taking as much we can get or is available.

If my mobile phone plan allows for 20GB of data, I’m sure I’ll use it up and then ask for an upgrade to 40GB. Soon after, I’ll be requesting for an upgrade to 60GB of data.

When the Australian cash rates were 0.25% in last 2020, I was asked if I thought the Reserve Bank of Australia would cut rates at the next meeting.

My response was, “who cares”. The questioners were often shocked by my seeming flippancy.

At this point, I would add by asking, “How much debt do you have and how pressure are you under, that you need a further 15 or 25 basis points of relief”.

Today, if your cost of borrowing has risen from 3% to 6% and you are now speculating whether interest rates go up a further 1% receives the same response from me with the difference being, are you still carrying so much debt that you may ‘break’.

Is it the Fed that is possibly going to ‘break something’ or have we simply kept taking on more debt?

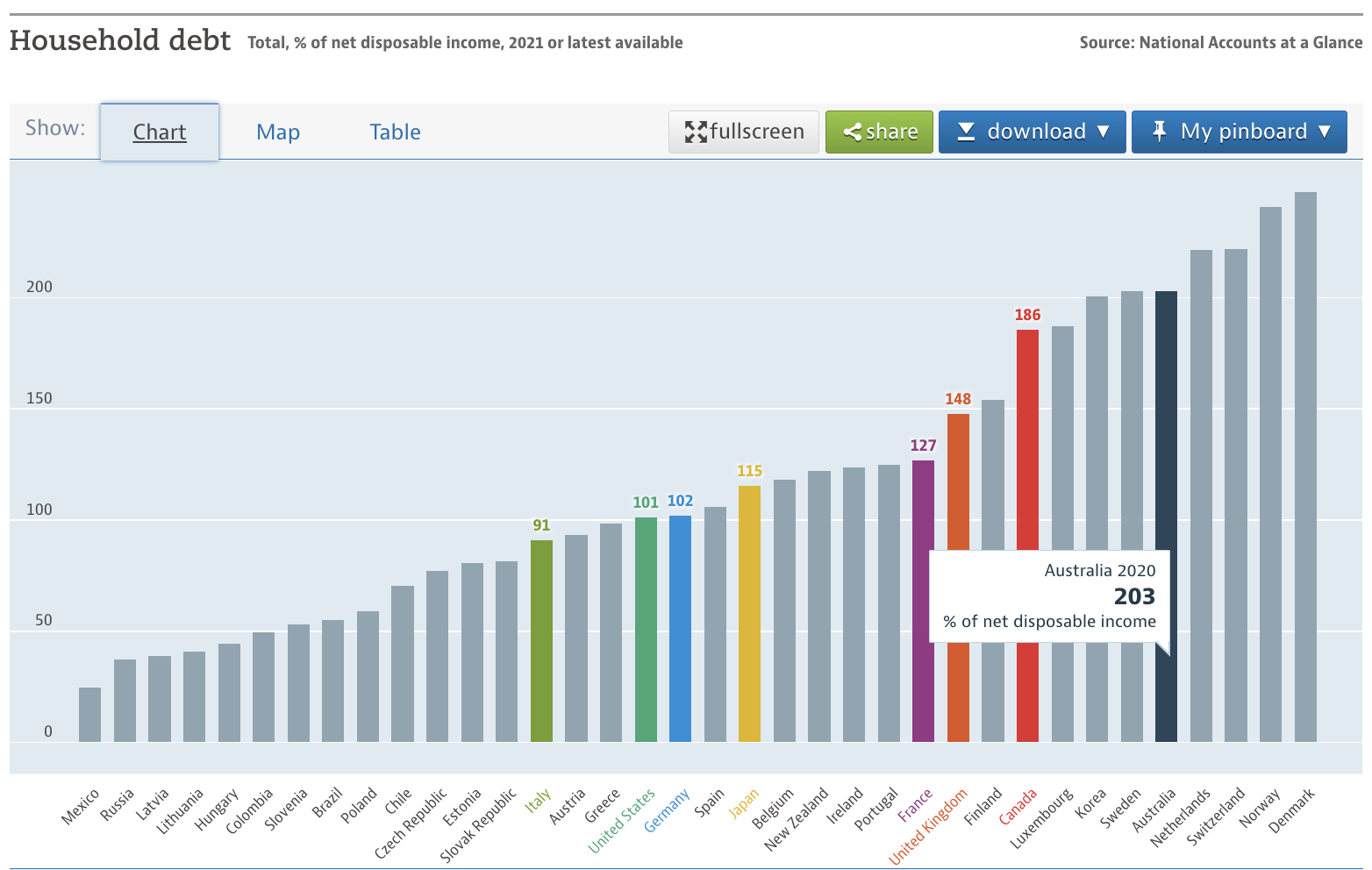

In the graphics below, you can see where the citizens of various nations sit in the indebted stakes.

https://tradingeconomics.com/country-list/households-debt-to-gdp

Look at those frugal and financial responsible Latvians and Hungarians.

source: OECD

Let me get back to the illustrating the ‘factor’ of the rise.

When rates went from 6% to 8%, it was only a 33% increase.

When rates went from 8% to 16%, it was ONLY a 50% increase.

Mortgage rates in Australia have nearly doubled. In the U.S., they have easily doubled.

The U.S. 2 years Treasury Bond yield has risen 10 fold.

When your interest repayments or the total cost of capital increase by such a factor, it is the quantum of the rise from the previous levels where you were comfortable with, that hurts the most.

My studies show that government bond yields have never risen by factors of 3 or 4 from their lows within any credit cycle.

At these extremes, as the chart within the below shows, the 2 year bond yield is miles above its 200 week moving average.

Why doesn’t mean reversion matter now, when it has many times prior?

Expecting rates to go higher and challenge gravity, probability and mathematics is a very foolish and crowded trade.

This is not about calling doom and whether the Fed ‘breaks something’……but rather it’s about thinking independently and reading the market tape as it is.

Behind the talk of where rates go to, sits speculative or investing opportunity.

If you have a view….then make the trade and take a position.

Those who shorted bonds when rates were 1% have made a fortune.

Today, if you think rates go up noticeably more……enough to tempt you into a trade, then short bonds and ride the expectation of whether the Fed keeps hiking rates to a point where ’they break something’.

If you think interest rates will fall, you could buy bonds.

Although, this is not a binary choice and the bond market may not be your natural business.

You can express you trade idea in many different manners.

For example, if interest rates keep rising, then you could short the equity of heavily indebted companies or technology stocks which aren’t profitable and have negative free cash flow, or

If you think rates are going to decline, then perhaps owing shares in high growth companies may see their prices ‘catch a bid’.

Of course, this is not personal advice and it’s important to do your research and analysis.

October 12, 2022

by Rob Zdravevski

rob@karriasset.com.au