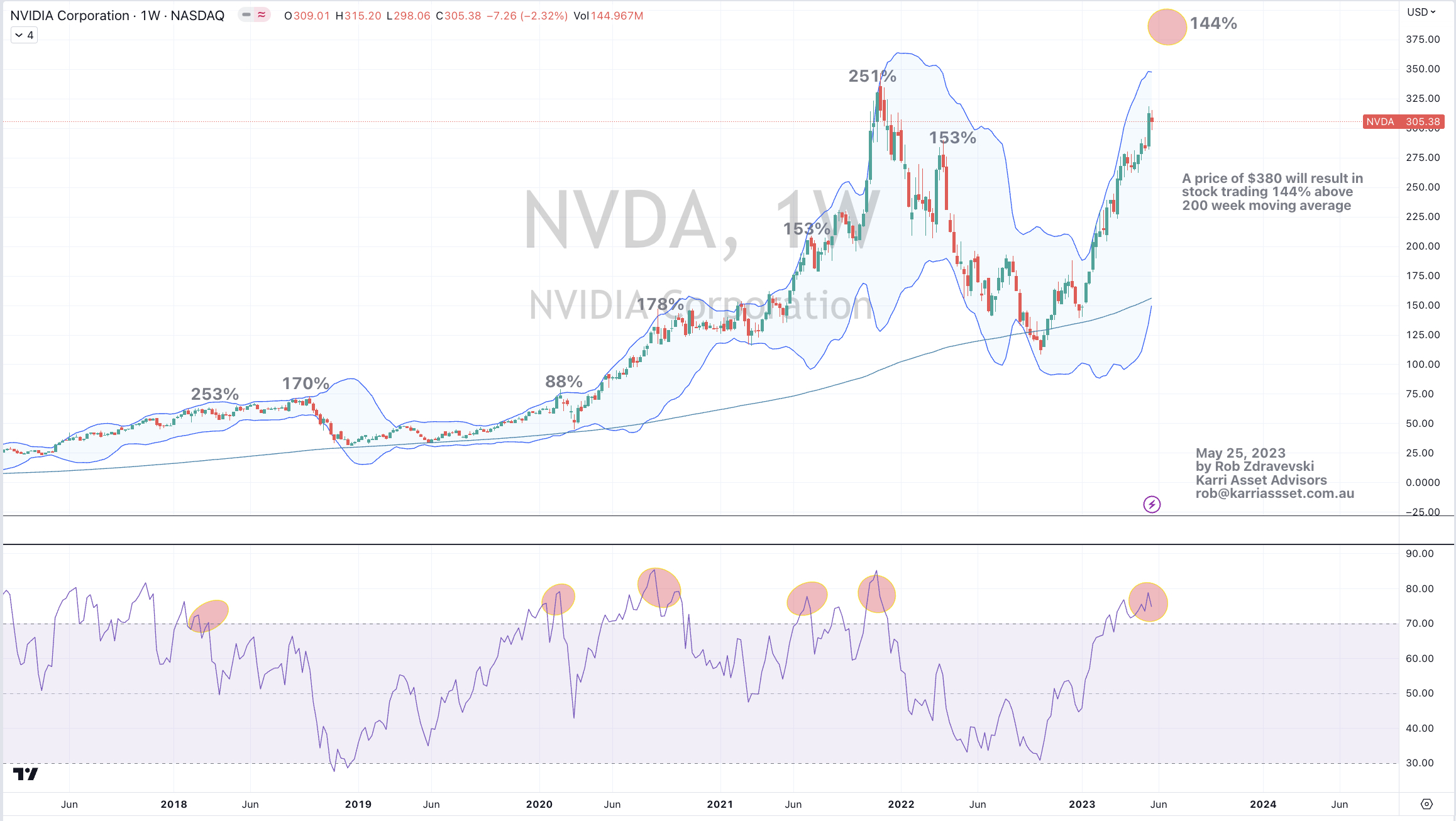

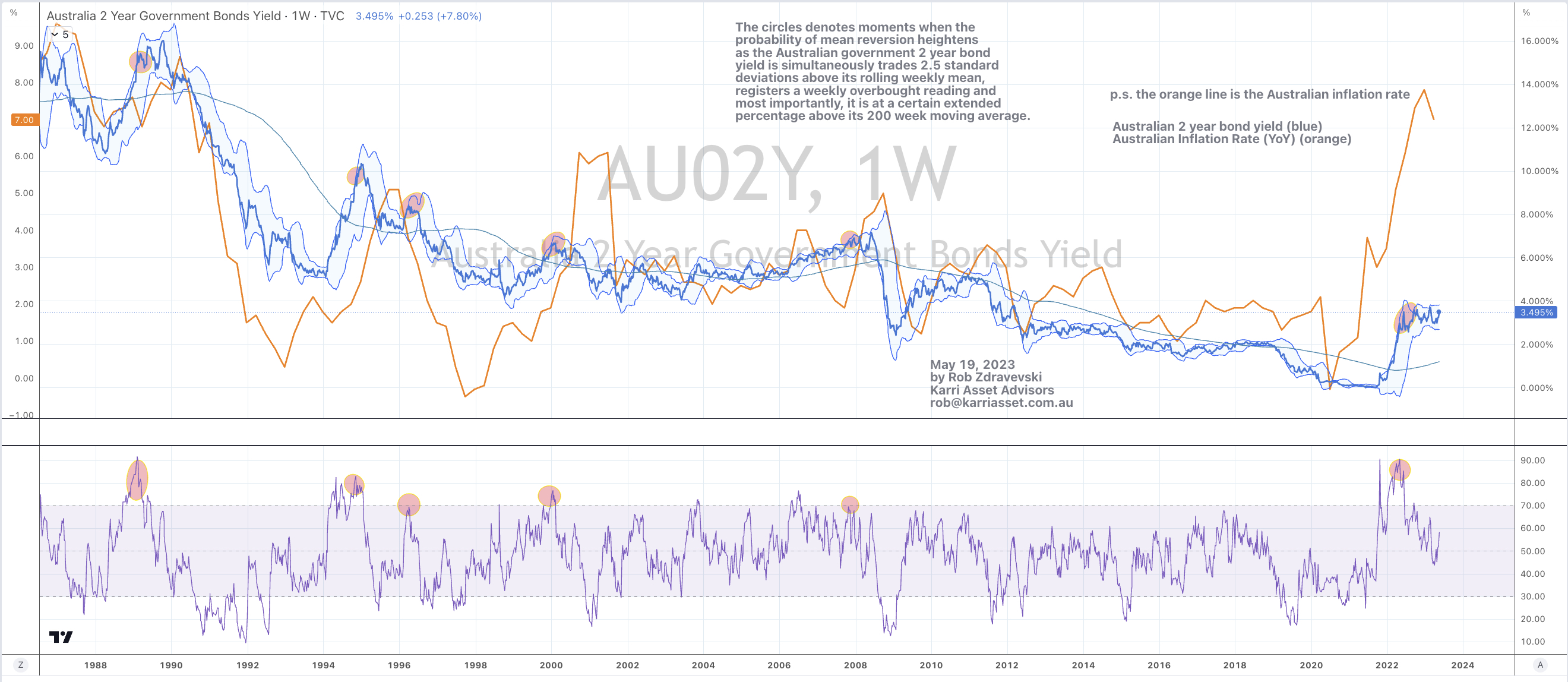

A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations)

Turkish 10 year government bond yields

China Coal

Chilean equity index

Overbought (RSI > 70)

Australian 3 month bank bill yield (90 day swap rate)

U.S. 3 month government bond yield

Sugar

Gold (in AUD)

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

None

Extremes “below” the Mean (at least 2.5 standard deviations)

China 10 year government bond yields

Copper

Soybeans

EUR/GBP

Oversold (RSI < 30)

U.S. 5 year bond yield minus U.S. 3 month bond yield

JKM LNG Gas

Lithium Hydroxide

Urea (Middle East)

KBW Banking Index

KRE Regional Bank Index

The Oversold Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

ZAR/USD

Notes & Ideas:

Equities were muted again for another week with weaker prices being amongst the majority, with Chinese equities, U.S. banks and small caps leading the way lower.

For instance, the U.S. Russell 2000 and Small Caps fell 1.3% and 1.9% respectively, while the S&P 500 rose 0.3% and the Dow Jones Industrials retreating 1.1%

The KBW Bank index fell 3.5% for the week, extending last week’s 7% decline, while the KRE Index (which tracks the regional U.S. banks) is closing in on a monumental low mimicking what was last seen in 2020 and in 2009. Incidentally, the KRE has tanked 46% in the past 3 weeks.

Something to watch are bearish outside reversal weeks seen in South Korea and Taiwan.

For the week, the ASX 200 rose 0.5% and the ASX Small Caps advanced 0.6%.

Overall, we remain in a trend less equity markets.

Government bond yields were generally quiet.

While many rose slightly (except in Brazil), many of those yields made intra-week low’s which were lower than last week’s low.

The U.S. 5 year bond yield minus U.S. 3 month bond yield spread (or yield curve) is still Oversold, which means something and a reminder that the Aussie 5 year minus 3 month yield spread is in negative territory.

Action in Commodities was a mixed bag, although the more notables moves were seen amongst the decliners.

Copper, Orange Juice (remember they were Overbought recently), Coal, Nickel and Lumber were some of the larger losers for the week.

Silver is no longer overbought as it fell 5%.

Rotterdam delivered Coal is closing in on a notable low.

Oil and some of the agricultural commodities moved out of oversold extreme territory

The Copper/Gold Ratio made a lower low (cite: May 4, ’23 Sell Copper note) and as it approaches a certain point, Selling Gold/Buying Copper may be a suggested trade.

JKM LNG closed at its lowest point in 3 years.

Heating Oil’s losing weekly streak extends to 7 while Lithium broke its 11 week losing streak

Currencies are seeing a couple new entrants in the weekly list with the ZAR/USD cross not visiting the ‘extremes’ for some time.

GBP/USD made a outside bearish reversal week a did EUR/USD.

The USD/SGD registered an outside bullish week which suggests weakness for the Singapore Dollar.

The larger advancers over the past week comprised of;

Cocoa 1.8%, China Coal 1.8%, Iron Ore 2.4%, Lean Hogs 11.4%, Lithium 3.2%, Natural Gas 6%, Palladium 1.8%, Gasoline 2.2%, Urea U.S. Gulf 4.2%, Oats 1.9%, BOVESPA 3.2%, SET 1.8%, Chile 2.1% and Copenhagen’s OMX soared 3.6%

The group of decliners included;

Australian Coking Coal (3.1%), Aluminium (3.9%), Rotterdam Coal (6.1%), WTI Crude (1.8%), Copper (4%), JKM LNG (1.8%), Coffee (2.8%), Lumber (5.4%), Tin (2.6%), Nickel (6.9%), Orange Juice (10.1%), Cotton (4%), Dutch TTF Gas (10.4%), Urea Middle East (3.5%), Silver in AUD (5%), Silver in USD (6.6%), Corn (1.7%), Soybeans (3.2%), Wheat (3.8%), Shanghai (1.9%), CSI 300 (2%), KBW Banks (3.5%), KRE Banks (5.2%), DJ Transports (2.4%), Hang Seng (2.1%), HSCEI (2%), S&P 600 Small Caps (1.9%) and Singapore’s Strait Times fell 1.8%.

May 14, 2023

by Rob Zdravevski

rob@karriasset.com.au