A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) either registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

* denotes multiple week inclusion

Extremes above the Mean (at least 2.5 standard deviations)

Australian 10 year bond yield minus the 2 year bond yield

Australian 10 year bond yield minus the 5 year bond yield

Brazilian 10 year government bond yield

Sugar *

Silver in USD

Gold in CHF

AUD/CAD *

ZAR/USD *

AUD/INR

AUD/USD

CAD/USD

All World Developed Equities Index (ex USA)

China A50

DAX

IBEX *

South Africa 40 Index

Nasdaq Transportation Index *

And Australia’s ASX Small Caps

Overbought (RSI > 70)

SHY

U.S. 10 year minus U.S. 2 year government yield *

U.S. 10 year minus U.S. 5 year government yield *

Robusta Coffee *

Gold as priced in AUD, CAD & GBP *

MYR/USD *

THB/AUD

Budapest

Karachi

NIFTY *

SENSEX *

The Overbought Quinella (Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Arabica Coffee

Gold in EUR & USD

CNH/USD

HSCEI

Hang Seng

And the Philippines PSE Index

Extremes below the Mean (at least 2.5 standard deviations)

CAD/AUD

EUR/GBP

USD/ZAR

Oversold (RSI < 30)

U.S. and German 2 year government bond yield *

Australian Coking Coal *

U.S. Midwest Hot Rolled Coil Steel *

North European Hot Rolled Coil Steel *

Lithium Carbonate *

Lithium Hydroxide *

USD/IDR *

USD/SGD *

The Oversold Quinella (Both Oversold and Traded at < 2.5 standard deviations below the weekly mean)

U.S. 3 month bill yield

USD/CNH

Notes & Ideas:

Global government bond yields fell.

Shorter dated American and German (Euro) yields are oversold.

Japanese yields slumped more than others.

Those who bucked the declines were Chinese 10’s and Gilts across the curve.

U.S. bond yields squeezed out a small rise.

Following its central bank policy to hike rates, Brazilian 10’s ventured into overbought territory.

It’s worthy to note that the Copper/Gold ratio rallied.

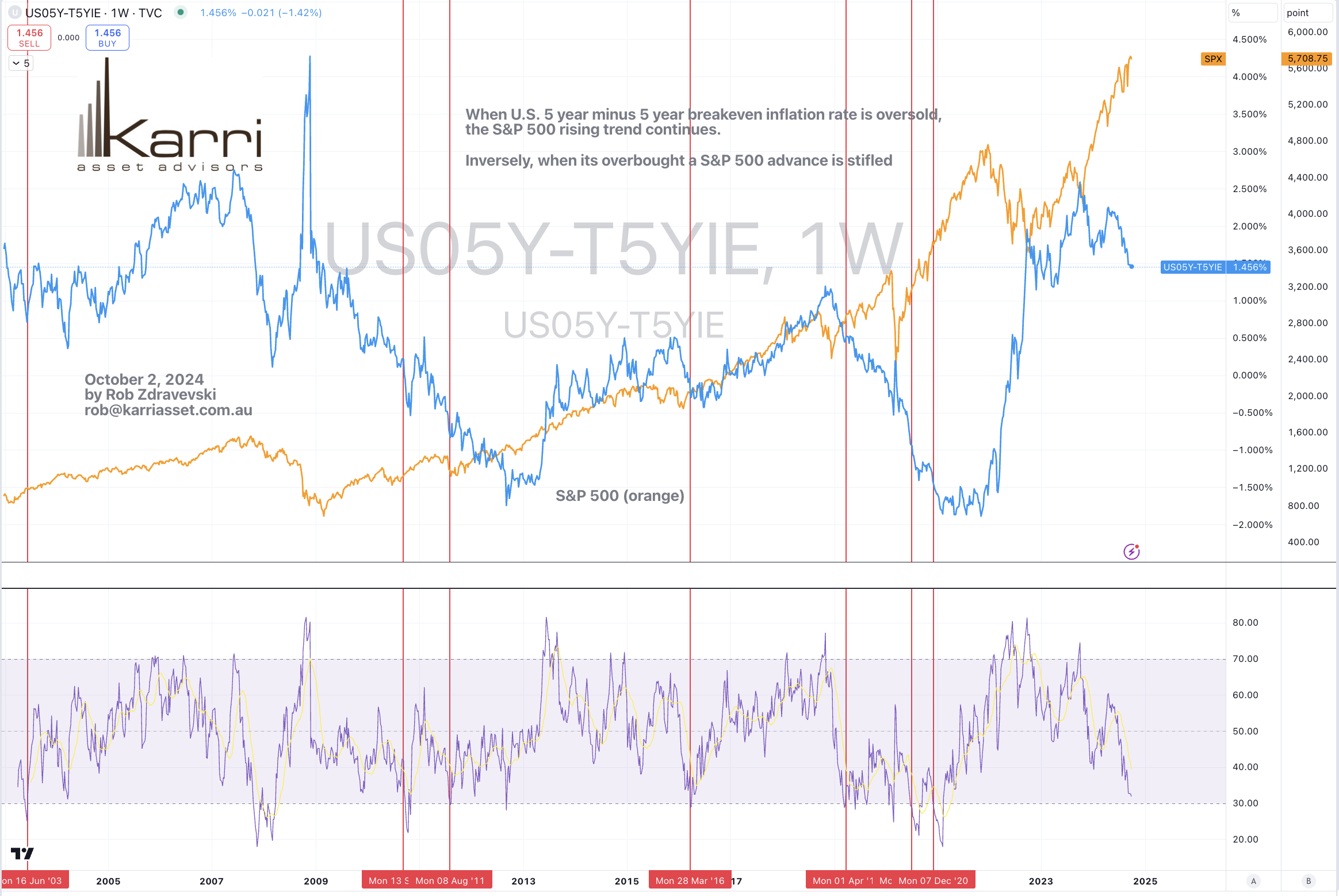

The U.S. 5 year minus 5 year breakeven inflation rate is nearing an oversold extreme.

And various Australian and U.S. bond yield spreads are in this weeks list.

Equities rose again, again.

Many indices have put together a 3 week rising streak.

And we are seeing more indices entering overbought territory.

The FTSE All World Index (Developed ex USA) makes a return to the list.

Chinese and Hong Kong indices soared during the week sending them into overbought extremes.

Bangkok, Copenhagen and the ASX Financials took a break from being overbought. The latter fell 4.4% for the week.

Spain’s IBEX and Germany’s DAX are mathematically stretched.

The former has risen 7 of its past 8 weeks, amounting to an advance of 16%.

The PSE has also climbed 16% over the past 14 weeks.

Australia’s Materials Index has soared 15% over the past 3 weeks.

Singapore’s Strait Times breaks its 6 week winning streak.

And Toronto’s TSX is nearing an overbought quinella.

Commodities mostly rose.

The Bloomberg Commodity Index has risen 6.8% over the past 3 weeks.

Palladium isn’t overbought this week while Gold across various currencies remains so.

Aluminium, Iron Ore, Copper, Coffee, Dutch TTF Gas and grains had a terrific week.

Only a few commodity contracts saw declines being Crude Oil, Palladium, Rice and OJ.

Most commodities are trading at their ‘mid-points’.

Soybeans have risen for 6 consecutive weeks.

U.S. Henry Hub Natural Gas has risen 44% in its current 4 week winning streak.

U.S.Midwest Hot Rolled Coil Steel has spent 18 weeks being oversold.

And Lithium Hydroxide has now spent 63 consecutive weeks in weekly oversold territory.

Currencies once again saw most action and they feature prominently in this week’s list.

The Aussie rose again, stringing together a 3 week streak.

The Canadian Loonie was generally weaker, again. Confusing perhaps, as the decline in the CAD juxtaposed the risk-on feeling for the week.

The Euro was weaker while the Yen saw strength.

The Swiss has fallen 3 consecutive weeks agains the AUD, confirming the ‘risk-on’ mood.

The DXY is in a 4 week losing streak which helps explain USD appearing as oversold in this weeks edition.

Furthermore, the USD/SGD has fallen for 9 of the past 10 weeks.

And the British Pound registered an overbought reading against the USD.

The larger advancers over the past week comprised of;

Australian Coking Coal 1.7%, Aluminium 7.1%, Rotterdam Coal 2%, Bloomberg Commodity Index 2.1%, Baltic Dry Index 6.7%, Cocoa 8.1%, Iron Ore 11.4%, Copper 5.9%, JKM LNG 1.8%, Arabica Coffee 7.3%, Lumber 4.6%, Tin 2.1%, Newcastle Coal 4.7%, Natural Gas 11%, Nickel 2.8%, Platinum 3.1%, Shanghai Rebar 3.3%, Robusta Coffee 8.4%, Dutch TTF 9.6%, Uranium 3.2%, Corn 4%, Oats 4.8%, Soybeans 5.3%, Wheat 2%, Shanghai Composite 12.8%, CSI 300 15.7%, All World Index ex-USA 3.4%, AEX 2.2%, Budapest 1.9%, CAC 3.9%, China A50 18.9%, DAX 4%, DJ Transports 2.7%, MIB 2.9%, HSCEI 14.4%, Hang Seng 13%, IBEX 1.8%, MOEX 2.7%, TAIEX 3%, KOSPI 2.2%, FTSE 250 2%, Nikkei 225 5.6%, Helsinki 4.2%, Stockholm 2.3%, PSE 2.8%, South Africa 4.9%, SMI 2.5%, SOX 4.3%, Chile 3%, Tel Aviv 4.9%, WIG 3.9%, ASX Materials 9.4% and the ASX Small Caps rose 2.8%.

The group of largest decliners from the week included;

WTI Crude Oil (4%), Orange Juice (4.2%), Palladium (5.1%), Gasoline (4%), Brent Crude Oil (3.7%), Rice (3.1%), KRE Regional Banks Index (3.1%), Nasdaq Biotechs (2.7%), Copenhagen (1.3%), Strait Times (1.4%) and the ASX Financials slumped 4.4%.

September 29, 2024

by Rob Zdravevski

rob@karriasset.com.au