Macro Extremes (week ending December 27, 2024)

December 29, 2024 Leave a comment

A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) either registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

* denotes multiple week inclusion

Extremes above the Mean (at least 2.5 standard deviations)

Australian 10 year bond yield minus Australian 2 year bond yield

Australian 10 year bond yield minus Australian 5 year bond yield

Chilean 2 and 10 year government bond yields

Swedish 10 year government bond yield

Japan Korean Marker (JPM) LNG

Natural Gas

Overbought (RSI > 70)

Japanese 2 year government bond yield

U.S. 5 year bond yield minus the U.S. 3 month bill yield *

Arabica coffee *

Pakistan’s KSE Index *

Czech Republic’s PX Index *

Israel’s TA35 *

The Overbought Quinella (Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Brazil 10 year government bond yield

U.S. 10 year bond yield minus Australian 10 year bond yield spread *

U.S. 10 year bond yield divided by the Australian 10 year bond yield spread *

Extremes below the Mean (at least 2.5 standard deviations)

Rice

AUD/GBP

AUD/SGD

ZAR/USD

Oversold (RSI < 30)

U.S. 3 month government bill yield *

Australian Coking Coal *

North European Hot Rolled Coil Steel *

U.S. Midwest Hot Rolled Coil Steel *

Lithium Carbonate *

Lithium Hydroxide *

Newcastle Coal *

RMB/USD *

CAD/USD

The Oversold Quinella (Both Oversold and Traded at < 2.5 standard deviations below the weekly mean)

Australian 10 year bond yield minus the U.S. 10 year bond yield spread

Chinese 10 year government bond yields *

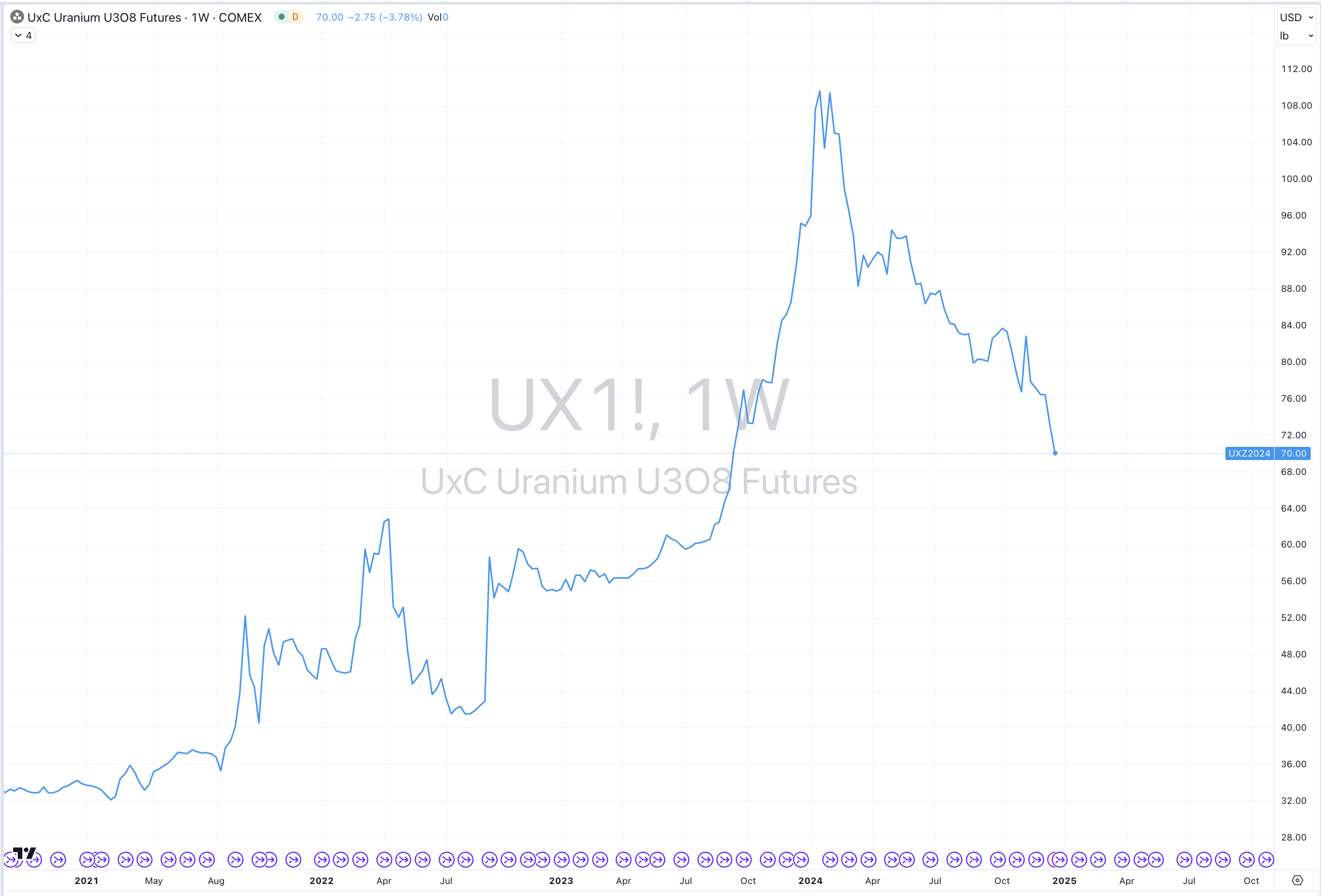

Uranium

AUD/THB *

BRL/USD *

INR/USD *

KRW/USD *

Notes & Ideas:

Government bond yields were mixed overall, with a bias for higher rates.

Euro 5’s and 10’s yields have risen for 4 weeks straight.

Yields across the British curve have also climbed for 4 weeks, as have Swedish 10’s.

The South Korean 10 year yield has bounced since its oversold reading 3 weeks ago.

Brazilian 10’s have risen for 6 weeks.

Chinese yields broke their 6 consecutive weeks of declines.

The U.S. 10 minus Euro 10 spread is nearly overbought.

While this week sees the return of the Aussie yield curve return to overbought territory.

Equities were stronger, reversing the previous 2 weeks of weakness.

The overreactive decline following last weeks Fed announcement seems comical now.

The Czech Republic’s PX Index has risen for 11 of the past 12 weeks.

Israel’s Tel Aviv 35 Index had climbed for 5 straight weeks.

The Russell 2000 rose and Oslo’s OBX Index broke their 4 week losing streak.

The Regional Banks (KRE) Index is in 5 week losing streaks.

And Indonesia’s IDX is nearly oversold.

Commodity prices were mixed.

Gases, Corn and Wheat were the notable gainers.

Cocoa, Oat and Coal prices were amongst the weeks losers.

Aluminium and JKM LNG (in Yen) broke their 4 week losing streaks.

Gold as priced in AUD and CAD has risen for 4 consecutive weeks, as has Corn.

Nickel is now trading 32% below its 200 week moving average and at its lowest close since early June, 2020.

Sugar has fallen for 11 of the past 12 weeks.

Dutch TTF Gas has climbed 15% over the past 2 weeks.

The Baltic Dry Index broke its 5 week losing streak,

Palladium has declined for 5 weeks,

while Uranium extends its loses to 6 consecutive weeks.

Lean Hogs and Cocoa broke their respective 5 and 6 straight weeks of gains.

U.S.Midwest Hot Rolled Coil Steel has spent 31 weeks being oversold,

while Lithium Hydroxide has now lingered in weekly oversold territory for 82 consecutive weeks.

Currencies were active, again.

The Aussie was weaker again.

The Thai Baht is at its highest against the AUD since June 2020.

The AUD has fallen for 10 of the past 13 weeks against the USD and the CAD.

The Euro was firmer.

EUR/JPY has risen for 4 straight weeks.

And so, the Yen was weaker and it has fallen for 4 weeks against the USD.

The Loonie remains oversold versus the USD as does China’s Renminbi.

And the NZD/USD has fallen for 11 of the past 13 weeks.

The larger advancers over the past week comprised of;

Aluminium 1.7%, Rotterdam Coal 3.2%, WTI Crude Oil 1.6%, JKM LNG 4.6%, JKM LNG in Yen 11.6%, Dutch TTF Gas 8.1%, Corn 1.7%, Wheat 2.5%, All World Developed ex USA 1.6%, China A50 2%, HSCEI 2.3%, Hang Seng 1.9%, TAIEX 3.4%, KLSE 2.3%, Nikkei 225 4.1%, Oslo 1.8%, Copenhagen 3.3%, Helsinki 1.7%, PSE 1.9%, SET 2.7%, SMI 1.8%, SOX 3.2%, ASX Financials 3.4%, ASX 200 2.4%, ASX Industrials 2.1%, ASX Small Caps and Turkiye’s BIST rose 3.1%.

The group of largest decliners from the week included;

Australia Coking Coal (2%), Cocoa (15.3%), Lean Hogs (2.1%), Newcastle Coal (1.9%), Orange Juice (2.7%), Uranium (3%), Oats (9.5%), Rice (1.5%), Egypt (1.9%) and Brazil’s BOVESPA fell 1.5%.

December 29, 2024

By Rob Zdravevski

rob@karriasset.com.au