This year, IPO’s on U.S. exchanges have raised a record $140 billion, exceeding the $107 billion raised in the height of the 1999 dot-com boom.

It has also been a week when we have seen;

✔️ Tesla announce its 3rd (secondary) equity sale this year.

The timing of the previous offerings uncannily occurred at interim market highs;

✔️ the most ridiculous IPO in DoorDash;

(stock doubles on its first day, market cap is $60bn vs. $16bn in early 2020)

✔️ and Airbnb premiered on the bourse with an IPO of its own.

The process of pricing of Airbnb’s IPO began between the $44-$50 per share range which was revised to $56-$60 while the final price struck was at $68.

Unlike Facebook’s IPO pricing debacle in 2012, I think Airbnb’s pricing was spot-on.

The after-market demand saw the stock close at $145 on its first day of trading. With $602 million shares outstanding, it now has a market cap of $87 billion.

But on a fully diluted basis (including employee stock, options and restricted units) Airbnb has 700m shares, so its Market Cap is $101 billion.

and DoorDash has 385m shares, which adjusts its Market Cap to $71.5 billion, which is a little bit too much when you are losing $150 million and trading on 30 times revenue.

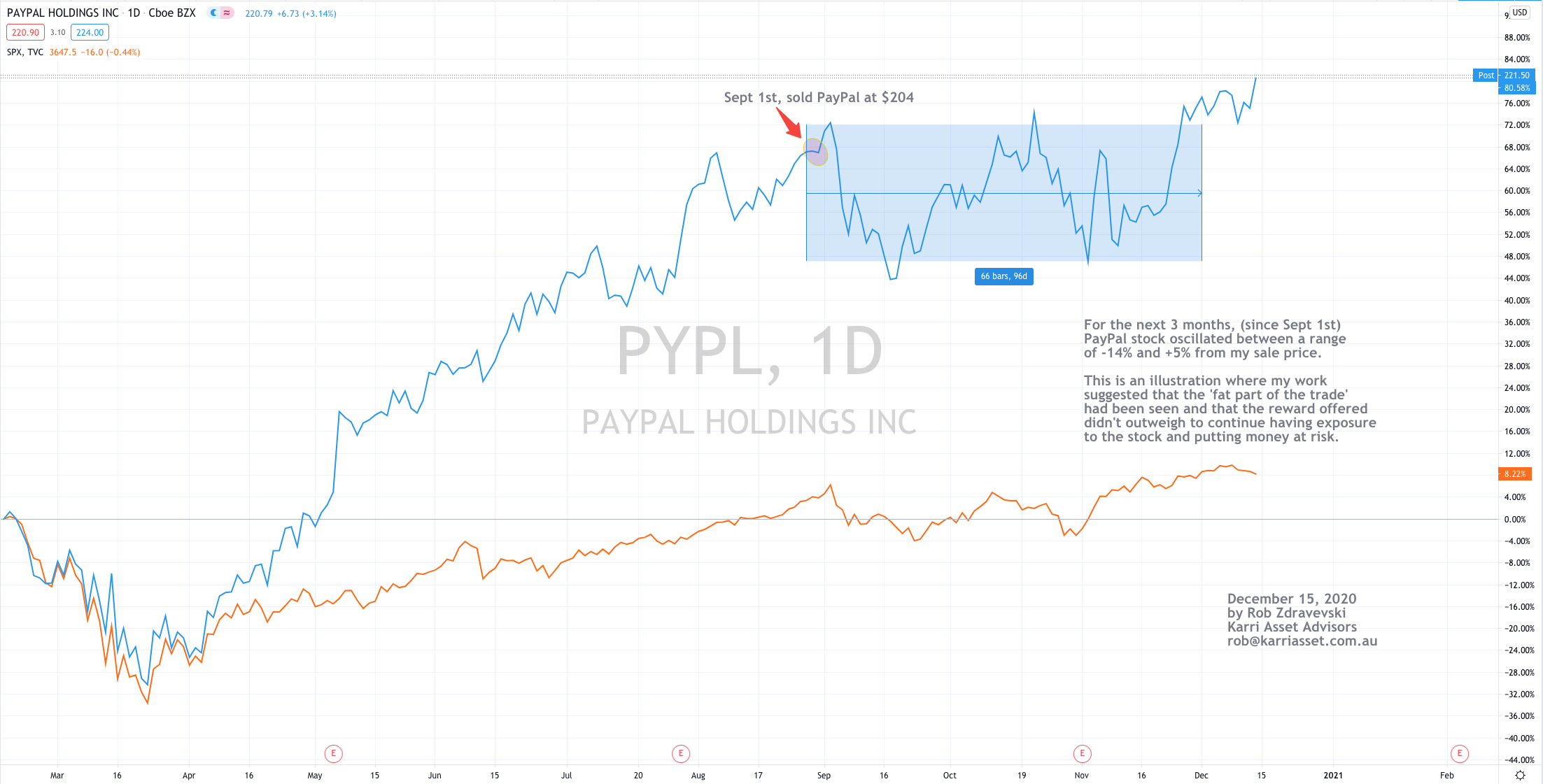

December 11, 2020

by Rob Zdravevski

rob@karriasset.com.au