The following assets (on a weekly timeframe) registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations)

Orange Juice

GBP/AUD

Overbought (RSI > 70)

Cattle

U.S. 2, 5 and 10 year government bond yields

German 2, 5 & 10 year government bond yields

British 5 year government bond yields

Australian, Spanish, French, British, Greek, Italian, Portuguese and Swedish 10 year government bond yields

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

TBT & TBX

U.S. 20 and 20 year government bond yields

Canadian, Korean and New Zealand 10 year government bond yields

Extremes “below” the Mean (at least 2.5 standard deviations)

AUD/CAD

SGD/AUD

AUD/INR

Straits Times Index

Coffee

Oversold (RSI < 30)

Tin

Hot Rolled Coil Steel (HRC)

Cotton

TLT

IEF & IEI

CSI 300 Index

Hang Seng Index

KRW/USD

The Oversold Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

INR/USD

JPY/USD

IDR/USD

Notes & Ideas:

The news for the week was the benign week for most commodities, the bouncing reverberation for equities and many currencies trading in and away from their recent weeks of extremes.

Other notable changes from last week’s list is that some equity indices moved away from their extremes such as the Shanghai Composite and the TAIEX and we saw some bond yields entering a quinella of overbought extremes.

Whilst we mainly saw a robust bounce amongst the larger U.S. equity indices, the KBW Banking Index and DJ Transports didn’t mimic the moves of their bigger siblings, advancing ‘only’ 0.7% and 1.5% for the week respectively.

In other capital market observations, the Hang Seng has fallen 27% since its rebound rally high on July 4th, 2022. The HSCEI Index has tanked 44% over the same time.

Inversely, from that same day, Brazil’s Bovespa has risen 24%. Interestingly, as Brazil’s central banks had one of the first and most aggressive rate hiking policy.

I’m watching for a change in trend in the price of Copper. Not yet confirmed though.

Gas prices continue to plummet, Coffee has fallen 13% in the past 2 weeks and Diesel (Gasoil) has tanked 17% over the same time.

Brazilian and Swiss 10 year bond yields look like peaking and rolling lower.

Many currencies strengthened against the USD (including the Aussie) and the DXY isn’t overbought this week. Incidentally, something to watch is the DXY had a bearish outside reversal week.

The Indian Rupee (INR) fell an alarming 4.6% on the week sending the currency to its weakest levels in my data. The INR has declined 11% this calendar year.

The Yen also fell to its lowest price (against the USD) on record.

Interestingly, India’s Sensex equity index is up 1.8% for this calendar year compared to the S&P 500 which is 21% that its price on January 1st, 2022 while the DXY has soared 17%.

And lastly, the US 5 year bond yield minus 5 year inflation breakeven rate remains Overbought as does its 10 year peer. These usually signal a peaking process in the Crude Oil price, which relates to other ramifications and correlations.

The larger advancers over the past week comprised of;

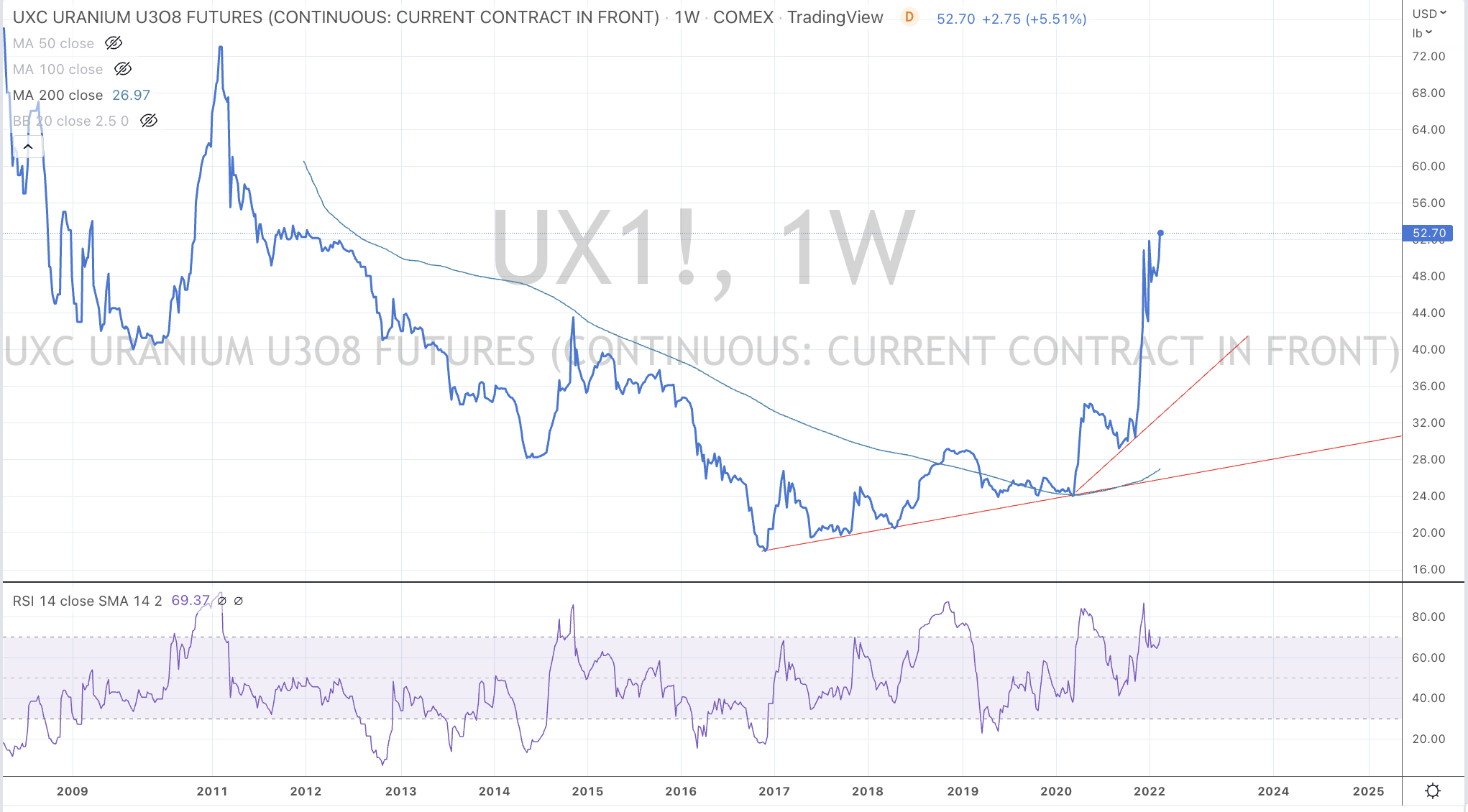

Australian Coking Coal 2.4%, Lean Hogs 8.4%, Lumber 8.9%, Cattle 2.4%, Platinum 4.4%, Brent Crude 2%, Uranium 5.5%, Silver in AUD 3.1%, Silver in USD 6.1%, CAC 1.7%, DAX 2.4%, Dow Jones Industrials 4.9%, DJ Transports 1.5%, MIB 3%, IBEX 2.2%, Bovespa 7%, S&P MidCap 400 3%, Nasdaq 100 5.8%, Sensex 2.4%, Stockholm 1.7%, Russell 2000 3.6%, SOX 8.1% (for context, it fell 8.3% last week), S&P 500 4.7% (same closing price as a month ago), FTSE 1.6%, Istanbul 8.9%, TSX 2.9%, S&P SmallCap 600 3.3% and Nasdaq Composite 5.2%.

The group of decliners included;

Aluminium (4.9%), Bloomberg Commodity Index (2.1%), Cocoa (3%), China Coal (2.3%), Gasoil (3.3%), Heating Oil (3.7%), Coffee (3%), Tin (2.9%), Natural Gas (23.2%), Nickel (2%), Sugar (2.4%), Dutch TTG Gas (20%), Florida Gulf Urea (4%), Gold in AUD (2%), Oats (5.4%), CSI 300 (2.6%), Hang Seng (2%), STI (2.3%), TAIEX (2.4%) and Australia’s ASX 200 fell 1.2%

October 23, 2022

By Rob Zdravevski

rob@karriasset.com.au