A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) either registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations)

U.S. 10 year breakeven inflation rate

Japanese Government 10 year bond yield

TBT

U.S. Government 10, 20 & 30 year bond yields

U.S. 10 year yield minus German 10 year bond yield spread

Gasoil

Heating Oil

Straits Times Index

AEX

MIB

Overbought (RSI > 70)

Russian 10 year government bond yields

U.S. 3 month bill yields

Cocoa

Urea Middle East price

Turkiye’s BIST 100

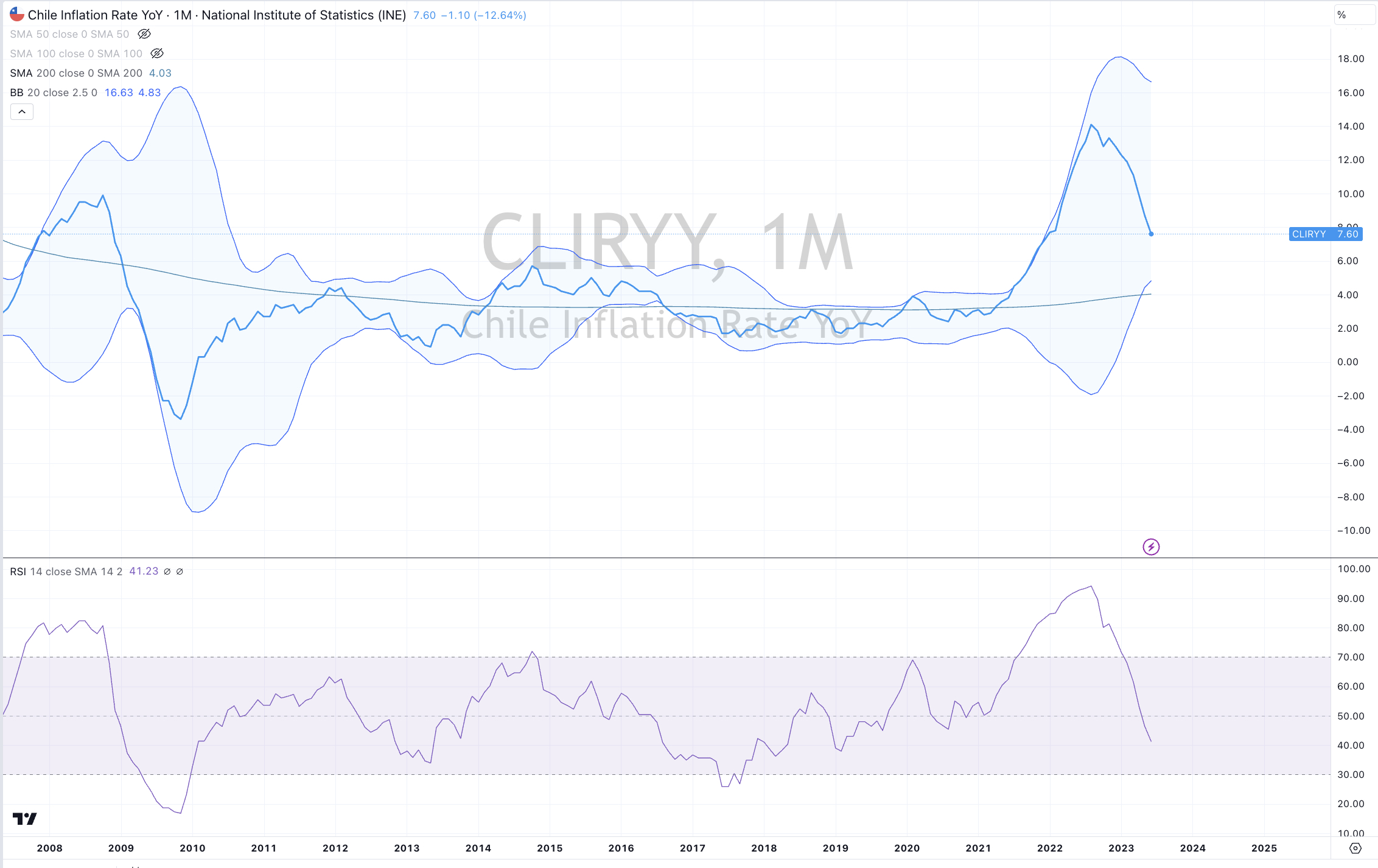

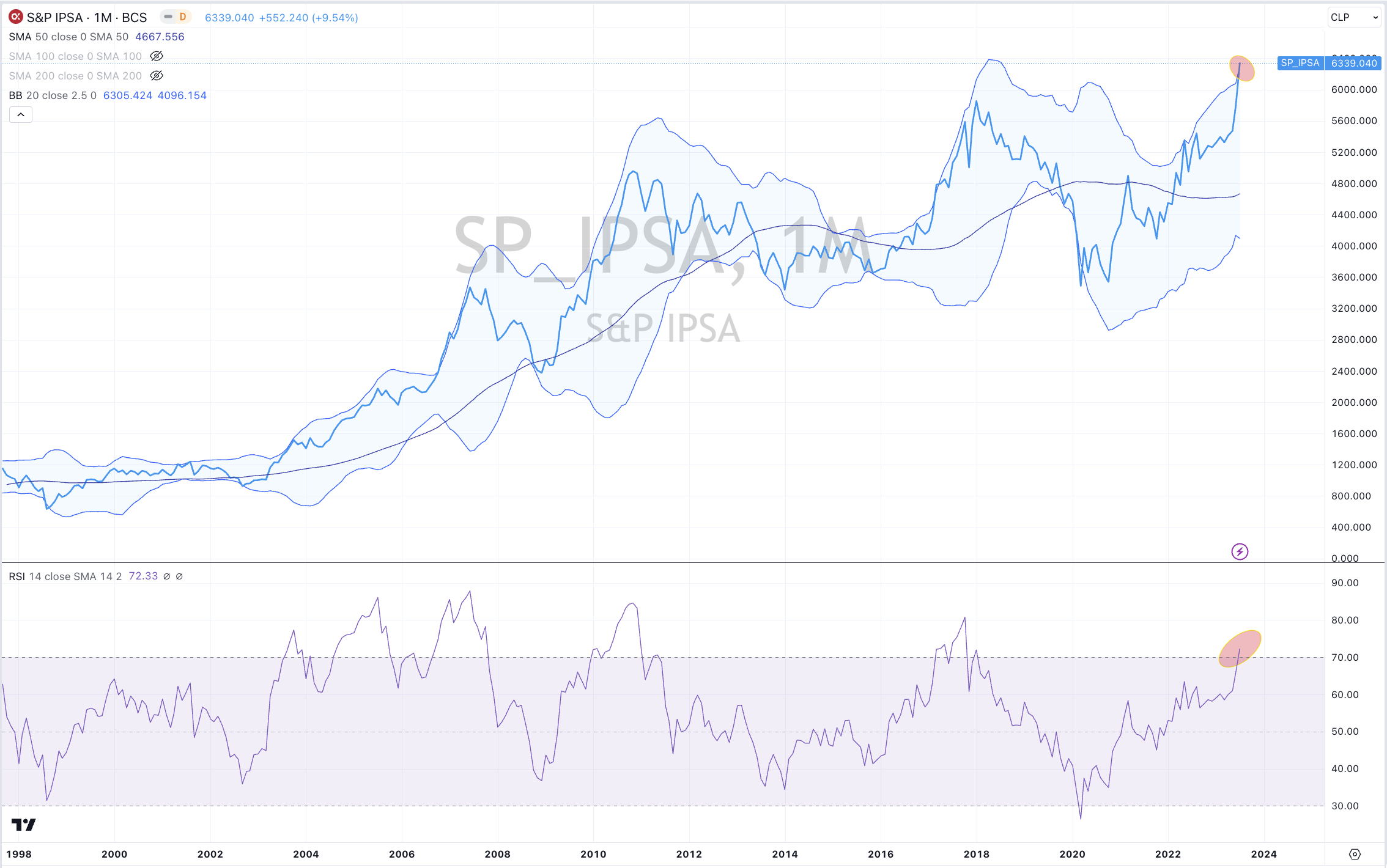

And Chile’s IPSA and IGPA equity indices

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

CHF/AUD

Russia’s MOEX equity index

Extremes “below” the Mean (at least 2.5 standard deviations)

TLT

Rubber

AUD/CAD

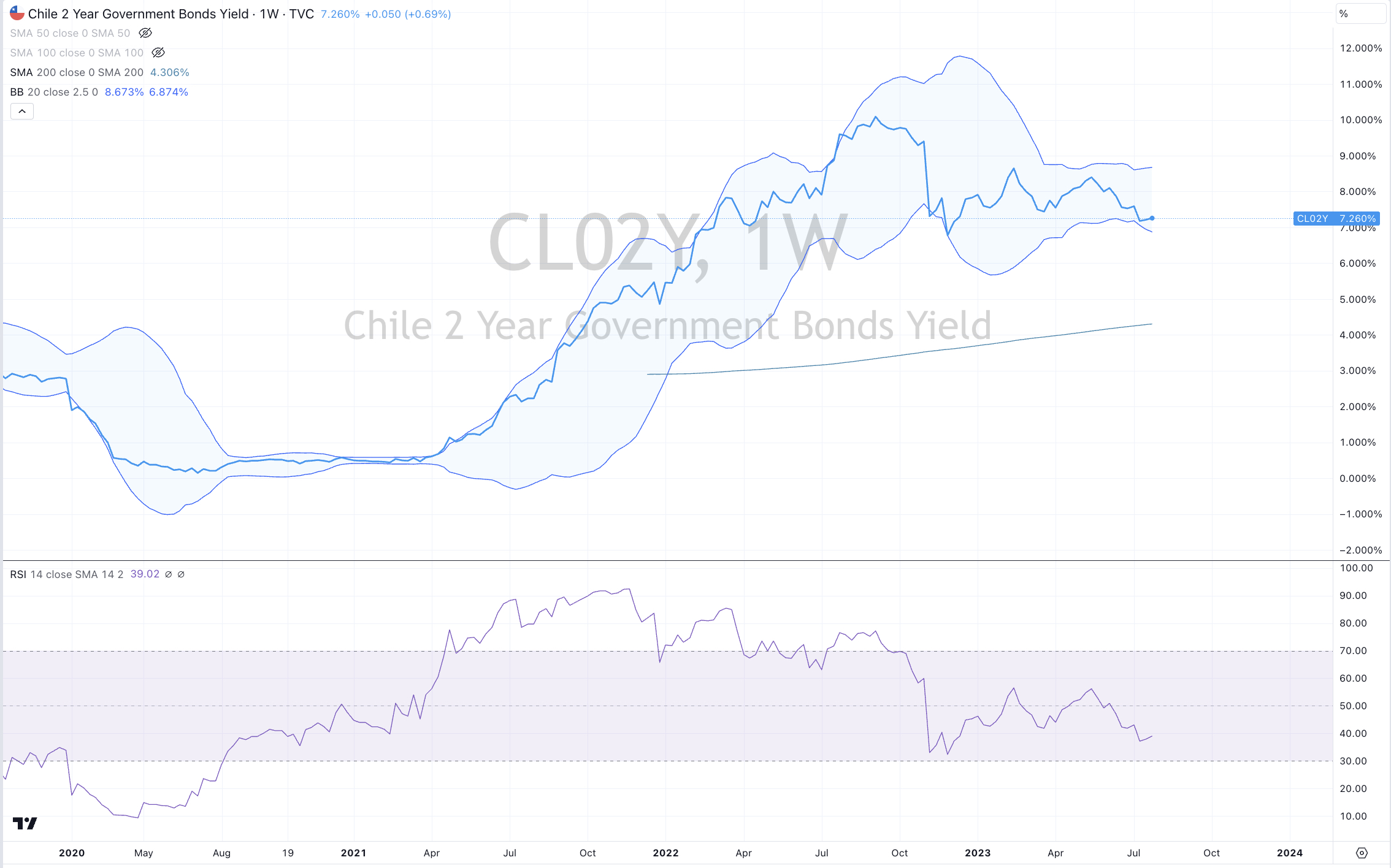

CLP/USD

Oversold (RSI < 30)

Newcastle Coal

The Oversold Quinella – Both Oversold and Traded at < 2.5 standard deviations below the weekly mean)

None

Notes & Ideas:

Equities had a poor showing this past week and amidst a sea of probability, it shouldn’t be a surprise considering the consecutive weeks that some bourses spent either extending winning weekly streaks or being overbought.

American indices aren’t in such territory anymore whether its the Nasdaq, Transports, Small Caps or Banks.

In fact, the DJ Industrials, DAX, CAC, MIB, Nasdaq Composite, Nasdaq 100, Nikkei 225, Russell 2000, SOX, TAEIX, FTSE 100, Mexico and Toronto’s TSX.,……all posted outside bearish reversal weeks

Furthermore, many stock market indices also broke weekly winning streaks such as Chile, U.S. KRE Regional Banks and DJ Transports along with the Nasdaq 100 ending its 10 week residence in the overbought arena.

Amsterdam’s AEX gave exactly last week’s gains.

Russia’s MOEX and Turkiye’s BIST 100 extended their amazing bull runs to recently include consecutive winning streaks of 6 & 7 respectively. Avid readers of this periodical can recite that these numbers are where streaks are closer to being exhausted and ending.

On a jolly note, the Nasdaq SmallCap 700 had a pleasant week.

Commodities were active again.

With the decline across the agricultural, Wheat isn’t overbought anymore.

Cattle had a bullish outside reversal week while Silver (priced in AUD) performed the opposite feat, being a bearish outside reversal week.

Rubber entered the oversold arena as it posted its 5th consecutive losing week.

Orange Juice reversed all of last week’s gains.

On the other side of the ledger, the S&P GSCI, Gasoil (diesel) and Brent Crude Oil respectively are into their 5th, 6th and 6th week of rising prices.

and Cocoa is now in its 9th week of being overbought.

In currencies, the AUD was weaker across many pairs and approaching the oversold region.

The AUD/EUR has stretched its weekly losing streak to 7 weeks.

Last week’s bearish outside reversal week in the AUD/JPY portended this week’s weakness in ‘risk; as seen in equity markets.

The Euro was mostly firmer as was the USD against most.

While the GBP/AUD is new overbought levels.

The South African Rand fell 4% giving up recent gains.

The Colombian Peso (COP) posted a bearish outside week….

And the CHF/AUD extends its weekly rising streak to 7 as it makes a visit to the Overbought quinella this week.

Bond yields mainly declined, which is keeping with my broader view of abating and mean reverting yields….although for the week, the Germans, Spanish and French yields did rise.

The Japanese 10’s soared into overbought land.

The larger advancers over the past week comprised of;

Australian Coking Coal 6.5%, Brent Crude 1.8%, Baltic Dry Index 2.3%, China Coking Coal 13.2%, WTI Crude 2.4%, Iron Ore 2.3%, Gasoil 3.4%, Heating Oil 3.4%, Coffee 2.2%, Cattle 1.6%, Dutch TTF Gas 7.3%, Rice 1.9%, MOEX 2.8% and BIST 100 rose 4.7%.

The group of decliners included;

Lean Hogs (2.1%), Copper (2.2%), Hot Rolled Coil Steel (2%), Lumber (4.2%), Tin (5.1%), Newcastle Coal (2.2%), Natural Gas (2.4%), Orange Juice (4.9%), Gasoline (3.5%), Silver (3.1%), Urea U.S. Gulf & Middle East (5.9%), Silver in AUD (1.8%), Corn (7.1%), Soybeans (3.7%), Wheat (9.8%), AEX (2.7%), CAC (2.2%), DAX (3.1%), DJ Transports (2.3%), MIB (3.1%), Hang Seng (1.9%), IBEX (3.3%), Nasdaq Composite (2.9%), Nasdaq 100 (3%), Nikkei 225 (1.7%), Copenhagen (2.1%), Helsinki (2.1%), Stockholm (2%), Swiss SMI (1.9%), SOX (4%), S&P 500 (2.3%), Singapore’s Strait Times (2.3%), TAEIX (2.6%) and the Nasdaq Transports fell 3.4%.

August 6, 2023

by Rob Zdravevski

rob@karriasset.com.au