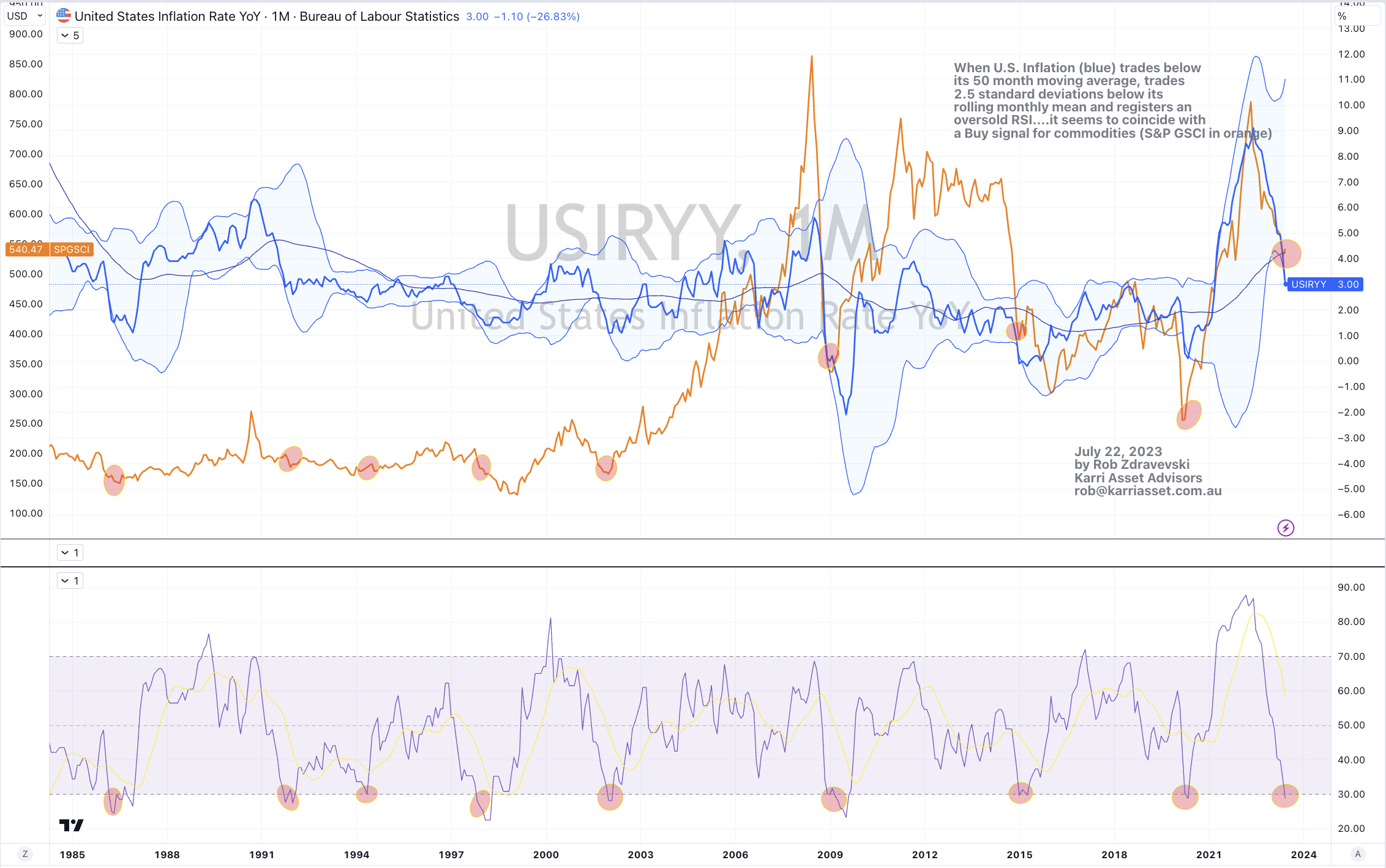

Macro Extremes (week ending July 28, 2023)

July 30, 2023 Leave a comment

A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) either registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations)

U.S. 10 year breakeven inflation rate

Japanese Government 10 year bond yield

Cotton

Gasoil

Heating Oil

Gasoline

Orange Juice

Urea (both U.S. Gulf and Middle East prices)

Wheat

S&P SmallCap 600

KBW Bank Index

KRE Regional Bank Index

Indonesia 30 Index

Overbought (RSI > 70)

Russian 10 year government bond yields

U.S. 3 month bill yields

Cocoa

MXN/USD

COP/USD

S&P 500

Nasdaq Composite Index

India’s Nifty 50 and Sensex

Turkiye’s BIST 100

Chile’s IPSA and IGPA equity indices

And Russia’s MOEX equity index

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Dow Jones Transports

Extremes “below” the Mean (at least 2.5 standard deviations)

Chilean 2 year government and yield

Oversold (RSI < 30)

Newcastle Coal

The Oversold Quinella – Both Oversold and Traded at < 2.5 standard deviations below the weekly mean)

None

Notes & Ideas:

Most of the currencies at extremes in last weeks edition are no longer so.

The AUD and EUR were weaker and the JPY was stronger.

Overall, the USD was stronger (it bounced off its oversold levels) except against most Asian currencies and the South African Rand.

The Rand continues to strengthen and the AUD/ZAR continuous to plummet.

The AUD/JPY pair had a bearish outside reversal week.

And the CHF/AUD is in a 6 week rising streak.

The big story in equities is that the S&P 500 is now overbought.

In fact, many equities are now appearing in that category.

The Dow Jones Transports registered a quinella overbought reading this week while rising for its 5th consecutive week and producing a 20% return over the past 8 weeks.

The KRE Regional Banking Index has posted an impressive 22% return in its 5 week winning streak.

The U.S. Mid Cap indices took a breather from being overbought, while the Russell 2000 was only a hair away from back-t0-back overbought weeks.

Shanghai, the CSI 300, HSCEO, Hang Seng and Mexico bourses all produced an outside bullish reversal week.

And the Nasdaq 100 in now in its 10th week of being overbought.

In commodities, most energy was stronger while precious metals, gases and steel related commodities were weaker.

It has been over a year since Gasoline, Heating Oil and Distillates traded at overbought extremes.

Cattle eased lower from overbought territory.

Lumber and Hot Rolled Coil Steel have fallen 11% and 8% respectively over the past 2 weeks.

Cocoa is now in its 8th week of being overbought,

while WTI Crude Oil and Diesel (Gasoil) are in a 5 week winning streak.

Yields were generally lower this past week, except for Japan.

The Japanese 10’s attracted the most attention during the week.

And the Aussie 10-2 yield spread has risen to its weekly mid-point.

The larger advancers over the past week comprised of;

Aluminium 1.7%, Brent Crude 4.8%, Baltic Dry Index 13.5%, Cocoa 3.2%, Coking Coal 2.7%, WTI Crude 5%, Gasoil 9.9%, Gold 1.8%, Copper 3%, Heating Oil 8.2%, Tin 2.6%, Newcastle Coal 6.1%, Orange Juice 5.7%, Gasoline 3.2%, S&P GSCI 2.8%, Urea U.S. Gulf 13.8%, Urea Middle East 10.3%, Shanghai 3.4%, CSI 300 4.5%, AEX 2.7%, DAX 1.8%, DJ Transports 2.9%, MIB 2.2%, HSCEI 6.1%, Hang Seng 4.4%, MOEX 2.9%, Nasdaq Composite 2%, Nasdaq 100 2.1%, SOX 4.1%, Strait Times 2.8%, BIST 5.7%, KLSE 2.6%, Mexico 2.3% and KRE 5.1%.

The group of decliners included;

Rotterdam Coal (3.6%), Iron Ore 4.3%, Hot Rolled Coil Steel (4.3%), Coffee (2.4%), Lumber (5.4%), JKM LNG (5%), Natural Gas (3%), Palladium 3.7%, Platinum (2.8%), Sugar (4.4%), Dutch TTF Gas (4.6%), Oats (2%) and the Copenhagen bourse fell 2.6%

July 30, 2023

by Rob Zdravevski

rob@karriasset.com.au