Today, Gasoil (diesel) and Heating Oil completed their mean reversion back to their 200 week moving average. This was prompted in this weekends edition of Macro Extremes.

They join Crude Oil and Natural Gas who achieved this milestone a couple months earlier.

However, ‘achieving’ mean reversion doesn’t translate to a ‘Buy’ signal.

This observation is a reminder to not have chased prices higher, especially at the stratospheric levels seen at the onset of the Russian-Ukraine war.

You would think lower fuel costs should be good for truckers and courier services, however there is a perverse trend that diesel prices lead the stock prices of ‘transporters’ lower.

This is a result of their fuel forward purchases, hedges and a lag in working off inventories.

This is terrific for today’s spot buyers.

Gasoil has halved since that high.

Although, falling Gasoil prices translates into predicting weakness in the Dow Jones Transports Index,

and a lower transports index usually mimics a decline in the S&P 500,

which coincides with weakness in the U.S. Dollar and broadly lower commodity prices,

which portends lower interest rates (perhaps the 2 year) yields,

which might be a positive for technology stocks.

But amongst this story telling, Gasoil, Heating Oil and Crude Oil will find a floor before it becomes mainstream news.

Now that RBOB Gasoline, Natural Gas, Dutch TTF Gas and the JKM LNG Marker prices have halved, I think other commodities in the energy complex are at a critical juncture.

While I remain cautious and specifically bearish on crude oil prices (I expect WTI Crude to move towards $65-$68 from its current $84.50), the larger declines could be seen in Heating Oil and Diesel (Gasoil).

They are currently trading at $3.95 and $10.82 respectively.

Both Heating Oil and Gasoil remain in downtrends across various timeframes and now I am watching a few more indicators to confirm strength and the next leg downwards.

If so, there could be 40% further downside in Heating Oil and Gasoil.

This view all seems quite perverse as the Northern Hemisphere winter approaches.

p.s. the largest use of diesel is in transportation, not electricity generators

I’ll write when/if the probability of this increases.

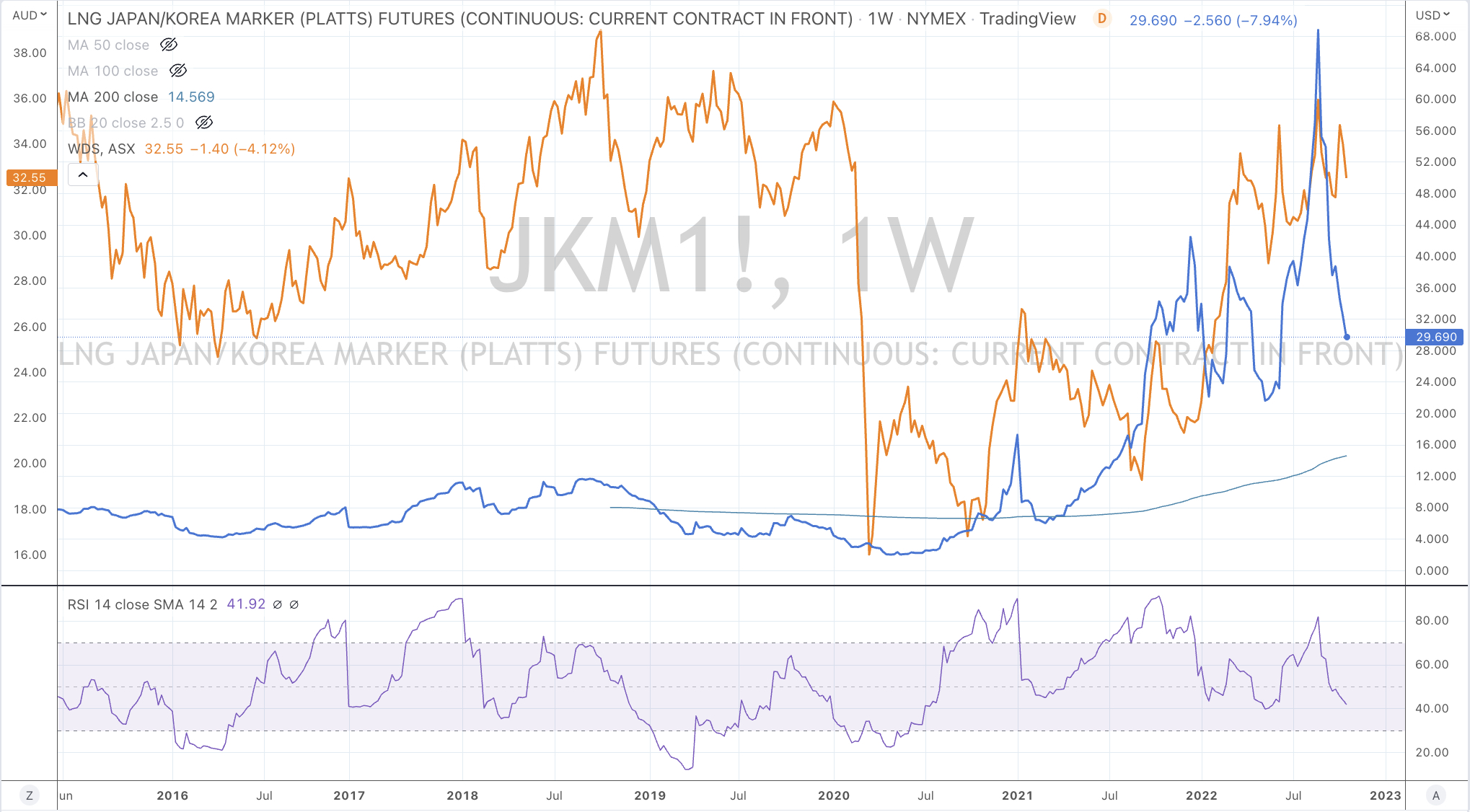

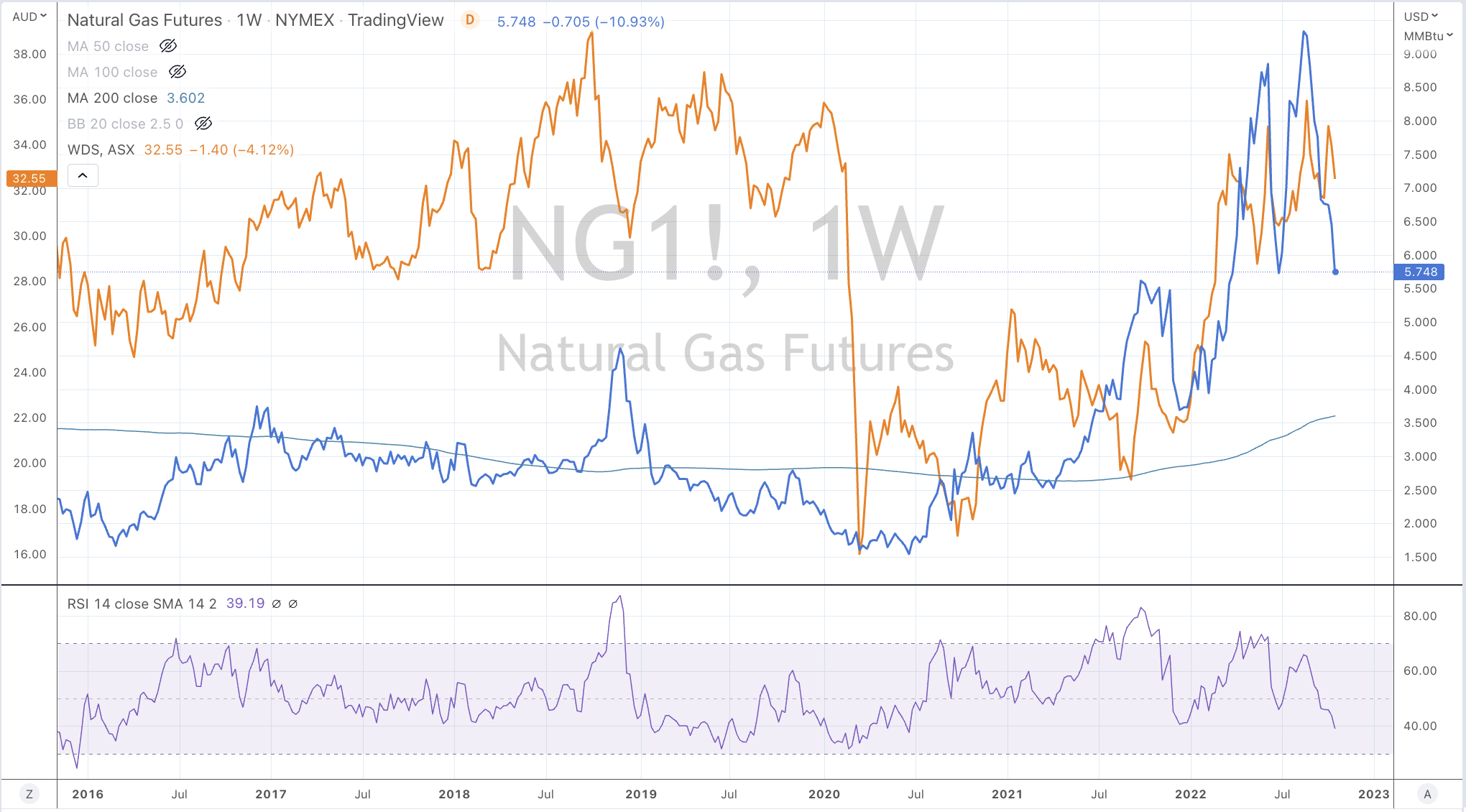

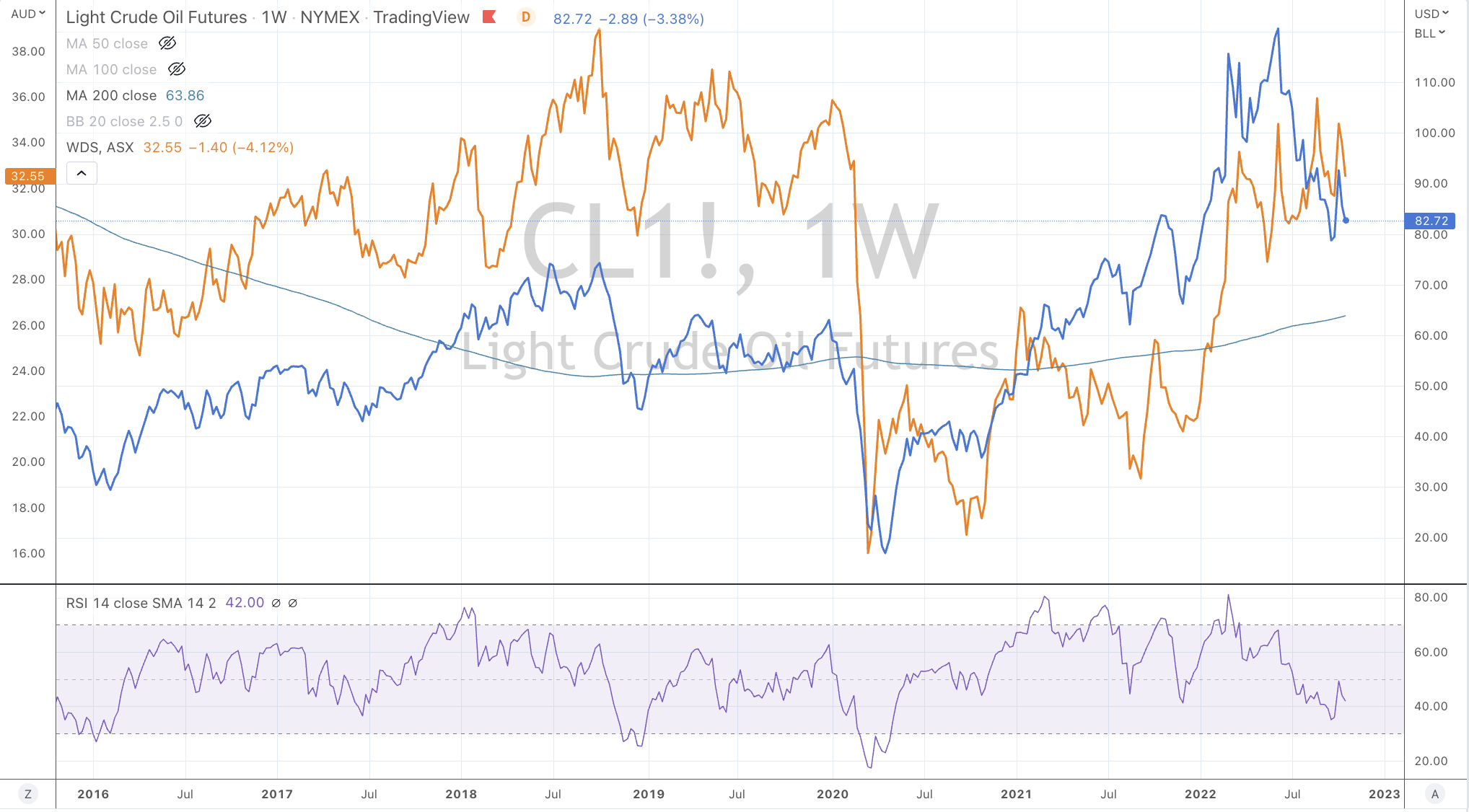

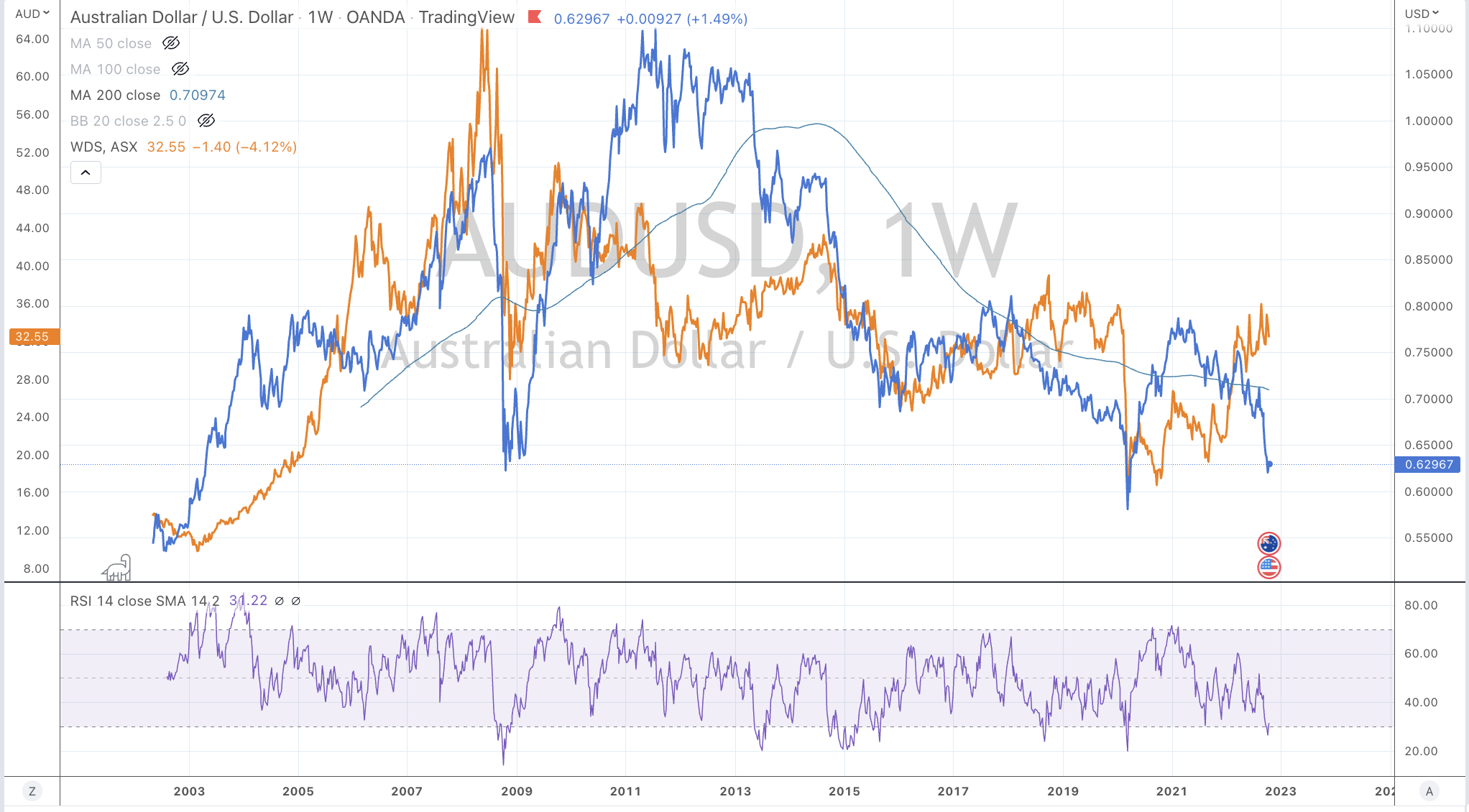

The next directional move in Woodside shares hinge on the direction in and or a combination of the Japan/Korea LNG Marker, the U.S. Natural Gas price, the West Texas Intermediate (WTI) Crude Oil prices along with the AUD/USD.

The charts below show the various correlations between Woodside shares and those assets.

My analysis of Woodside shares suggests that has a further 15% downside risk to $28, which is where I will be a buyer.

I may perform this exercise across other energy related equities.

JKM LNG Marker (in blue) versus WoodsideHenry Hub Natural Gas (in blue) versus WoodsideWTI Crude Oil (in blue) versus Woodside AUD/USD (in blue) versus Woodside

Overnight WTI Crude, Brent Crude, Heating Oil, Gasoline all fell 2%. Natural Gas fell 10%.

What is more important is last night’s trading session produced a bearish outside reversal day in all of mentioned commodities. This is where prices traded outside the previous day’s range, meaning today’s high and low was higher and lower than yesterdays range and the closing price was below yesterdays. It’s a bit more bearish because today’s close was lower than yesterday’s intra-day low.

Lately, I’ve been calling an interim top in Crude, highlighting extreme overboughts in Gasoline, Heating Oil and Distillates and a peak in the Australian Dollar.

Natural Gas has also touched some extreme overboughts where a Long trading exit target of $4.07 was hit.

Now, I think petroleum prices ease lower over the medium term while Natural Gas may nearly halve in price in the next 10 months or so.

Crude prices lead Natural Gas prices. Crude is down $12 since I made my recent ‘top’ call.

Below is picture of how I think it may play out.

You can see the resistance and supports it needs to test or break and this will help tell me if I’m wrong.

If the scenario below evolves, you’ll also see weaker (commodity) currencies such as the AUD and CAD while the U.S. Dollar strengthens.

While I have hinted that I am bullish on nuclear energy and uranium……I have been an avid watcher of thorium which has been seen as a nascent alternative but in truth it has existed for some time. Its evolution has been retarded for a host of political and capitalist reasons.

An extract from this article says, “China has some of the world’s largest reserves of thorium, a silvery metal with weak radioactivity. By some calculations it has enough to meet the country’s energy needs for at least 20,000 years. By contrast, China has some of the lowest uranium reserves of any nuclear-capable country”.

Brent Crude has fallen 12% since my note (3 weeks ago) called a peak.

Last night’s 6% decline (to $68.75) suggests and adds a little more strength to the downward trend.

The two links below discuss my bias for lower prices.

For now the $62 mark is a spot to watch and certain technicals over the coming weeks will help me decide if a new Long position is established there or around the $57 level.