Macro Extremes (week ending October 14, 2022)

October 16, 2022 Leave a comment

The following assets (on a weekly timeframe) registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations)

EUR/AUD

Overbought (RSI > 70)

U.S. Dollar Index (DXY)

TBX

U.S. 2,5, 10, 20 and 30 year government bond yields

German 2, 5 & 10 year government bond yields

British 5 year government bond yields

Spanish, French, British, Greek, Italian, Korean, Portuguese and New Zealand 10 year government bond yields

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

TBT

Extremes “below” the Mean (at least 2.5 standard deviations)

INR/AUD

AUD/CAD

Shanghai Composite

CSI 300

FTSE 100

Oversold (RSI < 30)

Tin

Hot Rolled Coil Steel (HRC)

TLT

IEF & IEI

CAD/USD

EUR/USD

NZD/USD

CNH/USD

DKK/USD

JPY/USD

ZAR/USD

KRW/USD

SEK/USD

Hang Seng’s HSCEI and HSI equity indices

And Taiwan’s TAIEX equity index

The Oversold Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

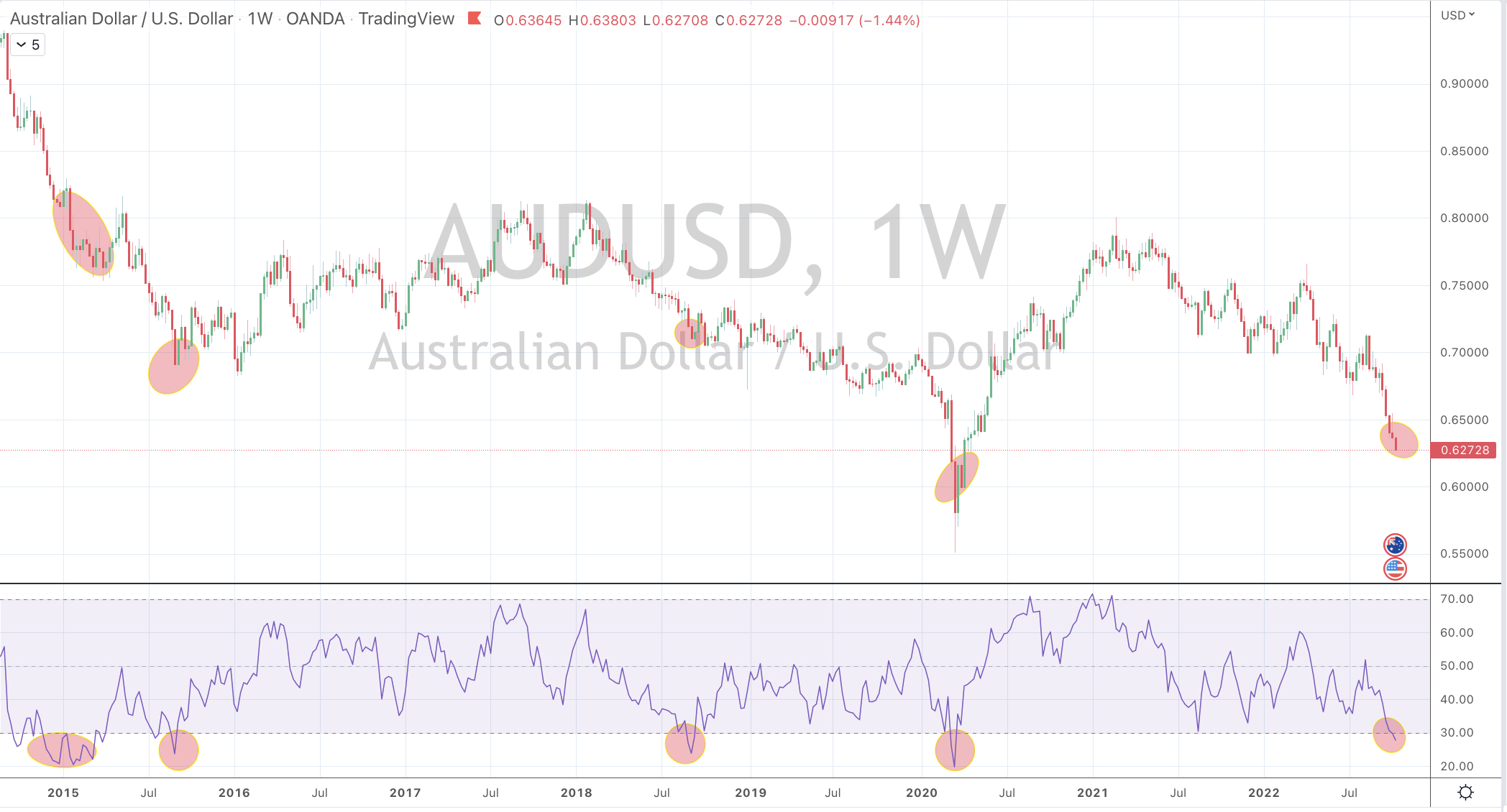

AUD/USD

AUD/SGD

Notes & Ideas:

The big news for the week was the first visit for the AUD/USD into a quinella of Oversold readings not seen for 2.5 years, which last occurred in March 2020.

The Aussie was also weak against the Singapore Dollar and the Euro (it has lost 8% vs EUR in a month) although more interestingly against another commodity sensitive peer, being the Canadian Loonie.

There will be a seperate post about my thoughts on the AUD/CAD currency cross.

This somewhat correlates with the was weakness in the energy commodities complex but that is OK for in last week’s edition I wrote, “ Gasoline, Brent, Heating Oil and Diesel rose somewhere between 15% and 26% in a single week”.

In other news, equities were mostly muted except for the movers in the list below while Palladium and Silver had a rough week.

If you are a ‘market person’ you’d know that many government bond yields (albeit they rose for the week) are not higher than seen 3 weeks ago.

The British Pound against the USD and other currencies is no longer Oversold. In fact, the Aussie has weakened 8% against Pound Sterling in the past 2 weeks. That’s a heck a move for a developed world currency cross however the fact that the AUD/GBP is no longer overbought isn’t a surprise as it was reported at such an extreme in this publication 3 weeks ago.

In other news, Bitcoin hit an intra-week low of $18,131. It’s lowest since June 13, 2022. The prior time that it traded that low was in December of 2020.

Cotton and Toronto’s TSX mean reverted to its 200 week moving average.

The New Zealand 10 year yields reappeared into Overbought territory.

The South Korean KOSPI isn’t Oversold this week.

The Philadelphia Semiconductor Index (SOX) has now fallen 30% in the past 10 weeks.

The second biggest news was that most of the energy complex (attributing much to the CRB Index percentages rise) had a cracker of a week with Gasoline, Brent, Heating Oil and Diesel rose somewhere between 15% and 26% in a single week……all except Gas, including Natural Gas which saw an intra-week low of $6.30 and closing in on my $5.00 target.

Dutch TTF Gas and the Japan-Korean LNG Marker continue their string of notable weekly declines.

It’s not a surprise that Rotterdam delivered coal rose 5% follow a 34% drubbing over the past 5 weeks and after touching an Oversold extreme last week and that the Baltic Dry Index fell 6% following its tear of 81% over the past 5 weeks.

The larger advancers over the past week comprised of;

Australian Coking Coal 3.9%, Aluminium 1.8%, Rotterdam Coal 4.7%, Lumber 10.9%, Uranium 4.1%, Oats 5%, DAX Index 1.3%, Copenhagen 2.6% and Helsinki rose 1.9%.

The group of decliners included;

Bloomberg Commodity Index )3%), Baltic Dry Index (6.3%), WTI Crude (7.6%), Gasoil (13.7%), Gold (3%), Lean Hogs (11.5%), JKM LNG Marker (6.4%), Coffee (9.8%), Tin (2.2%), Natural Gas (4.4%), Palladium (8.9%), Platinum (2.5%), Gasoline (3.8%), Silver (9.2%), CRB Index (3.1%), Dutch TTF Gas (9.1%), Brent Crude (6.8%), Silver in AUD (6.9%), Wheat (2.3%), SP GSCI (5.2%), AEX (2.6%), HSCEI (7.3%), HSI (6.5%), Bovespa (3.7%), Nasdaq 100 (3.2%), Oslo (2%), SOX (8.3%), STI (3.4%), TAIEX (4.2%), FTSE 100 (1.9%), Nasdaq Composite (3.1%) and Australia’s ASX 200 was flat for the week. It fell 0.06%.

October 16, 2022

By Rob Zdravevski