The following assets (on a weekly timeframe) registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations)

Copper/Gold Ratio

Overbought (RSI > 70)

Cattle

Orange Juice

TBT and TBX bond ETF’s

U.S. 2, 5, 10, 20 and 30 year government bond yields

German 2 and 5 year government bond yields

U.S. 5-7 year corporate bond yields

U.S. 10 year minus Australian 10 year bond yields

Divide the difference between the yield of the U.S. 10’s and Australian 10’s

U.S. 5 year bond yield minus U.S. 5 year breakeven inflation rate

U.S.10 yer bond yield minus U.S. 10 year breakeven inflation rate

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

None

Extremes “below” the Mean (at least 2.5 standard deviations)

Coffee

Oversold (RSI < 30)

Tin

Hot Rolled Coil Steel (HRC)

IEI, IEF & TLT bond ETF’s

Taiwan’s TAIEX index

INR/USD

IDR/USD

JPY/USD

The Oversold Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

None

Notes & Ideas:

This past week’s big news is bonds were mainly bid higher causing many yields to fall, even after the Bank of England, Australia’s Reserve Bank and the U.S. Federal Reserve all lifted interest rates.

It was a case of ‘sell the rumour and buy the fact’.

In this week’s list ‘extremes’ above, I have added some stranger bond yield relationships to create some curiosity.

Commodity indices had a strong week.

Many more currencies aren’t showing ‘extreme’ weakness against the U.S. Dollar.

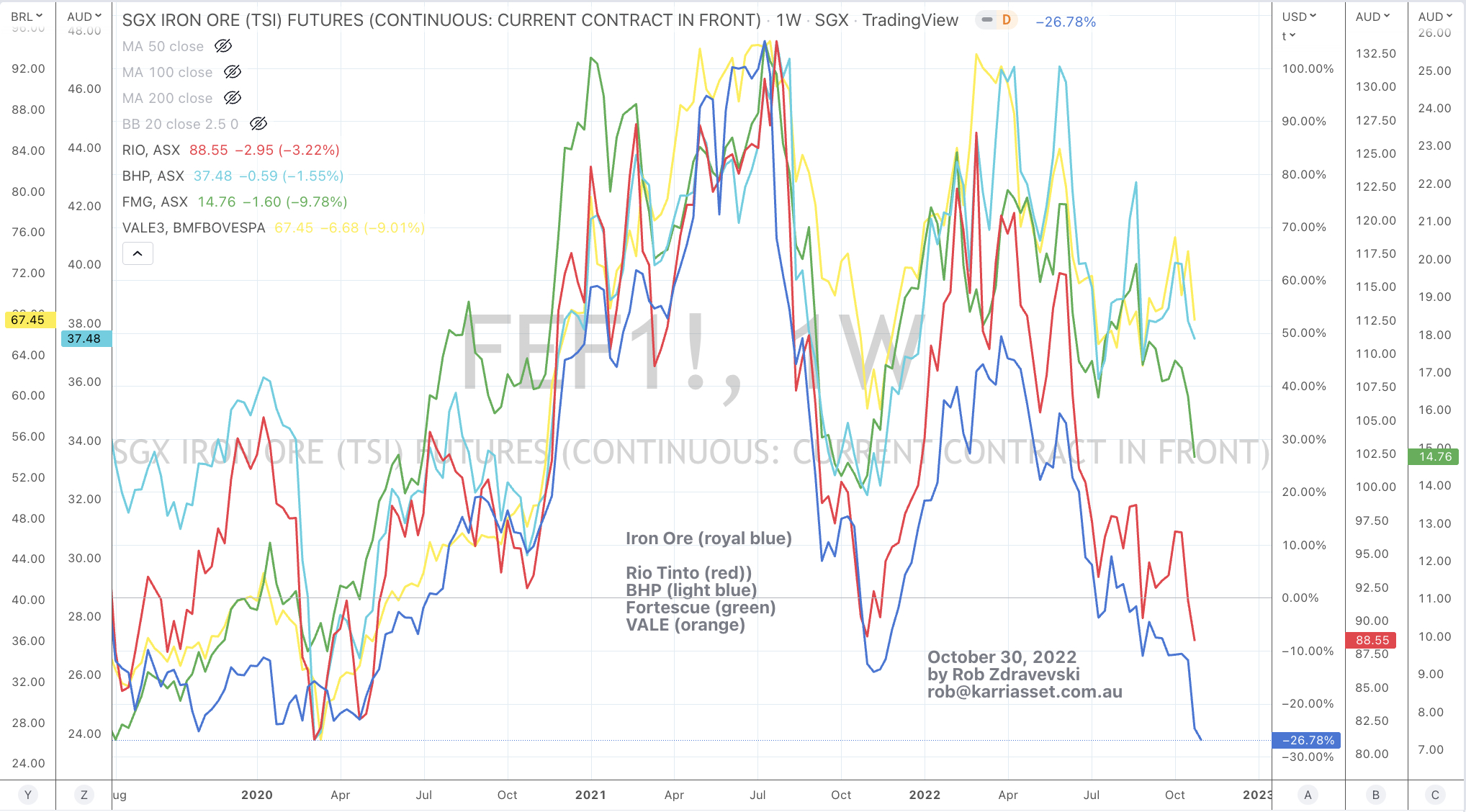

Iron Ore, Cotton and Hong Kong/Chinese equities are no longer at ‘extremes’. They bounced from their recent oversold levels. The Hang Seng index rose 9% for the week.

Other examples of prices bouncing off their recent extreme lows include the KOSPI rising 8.5% over the past 5 weeks and the U.K.’s FTSE 100 is up 6.7% in 3 weeks.

If you made 7% in a month, would you be tempted to close the books and take the next 11 months off?

The U.S. equity markets seemed to give off a feeling that they had a positive week, when the opposite occurred.

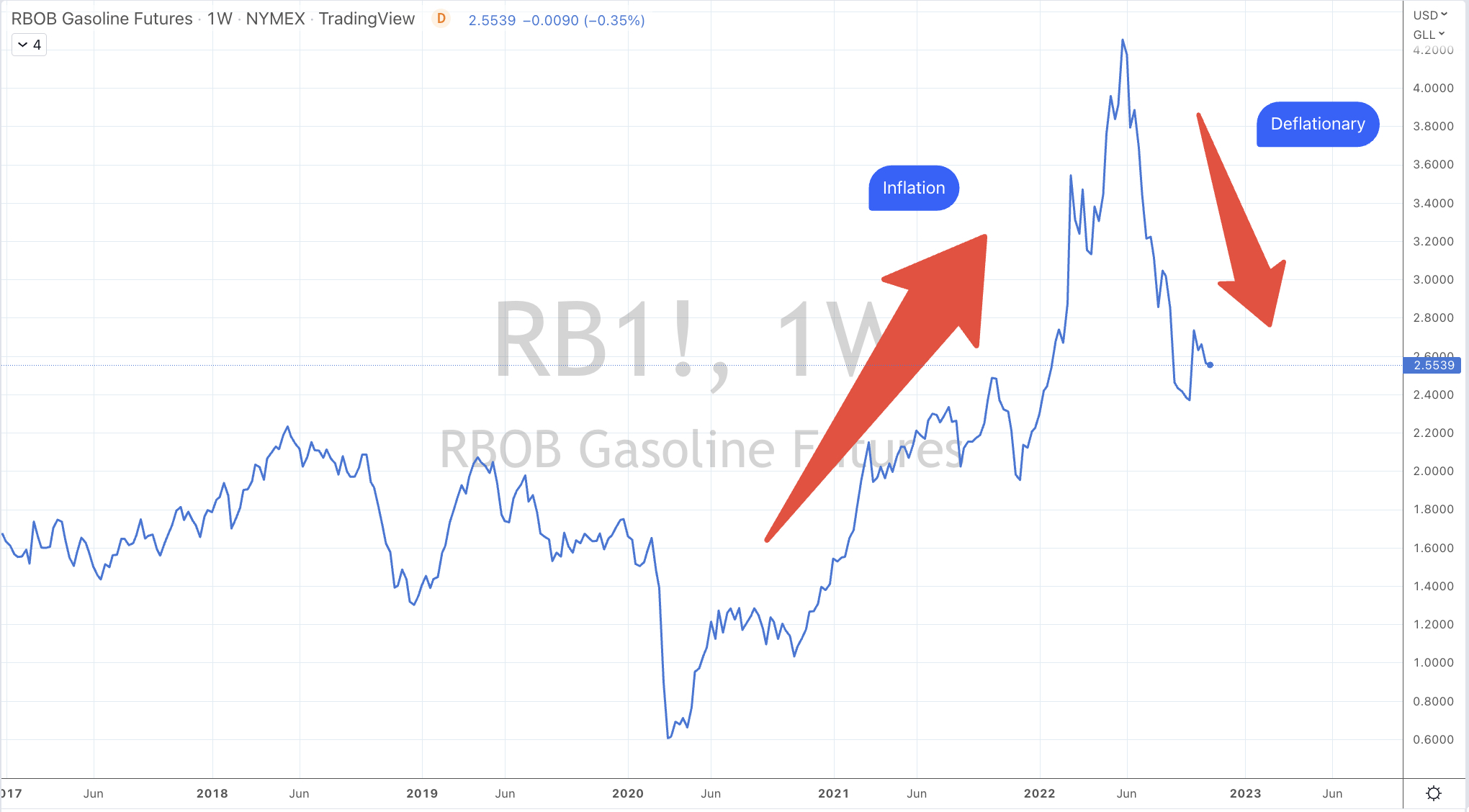

In addition to this week’s list of notable movers, over the past fortnight, Natural Gas has soared 27%, Silver is up 14% and WTI Crude has risen 9%.

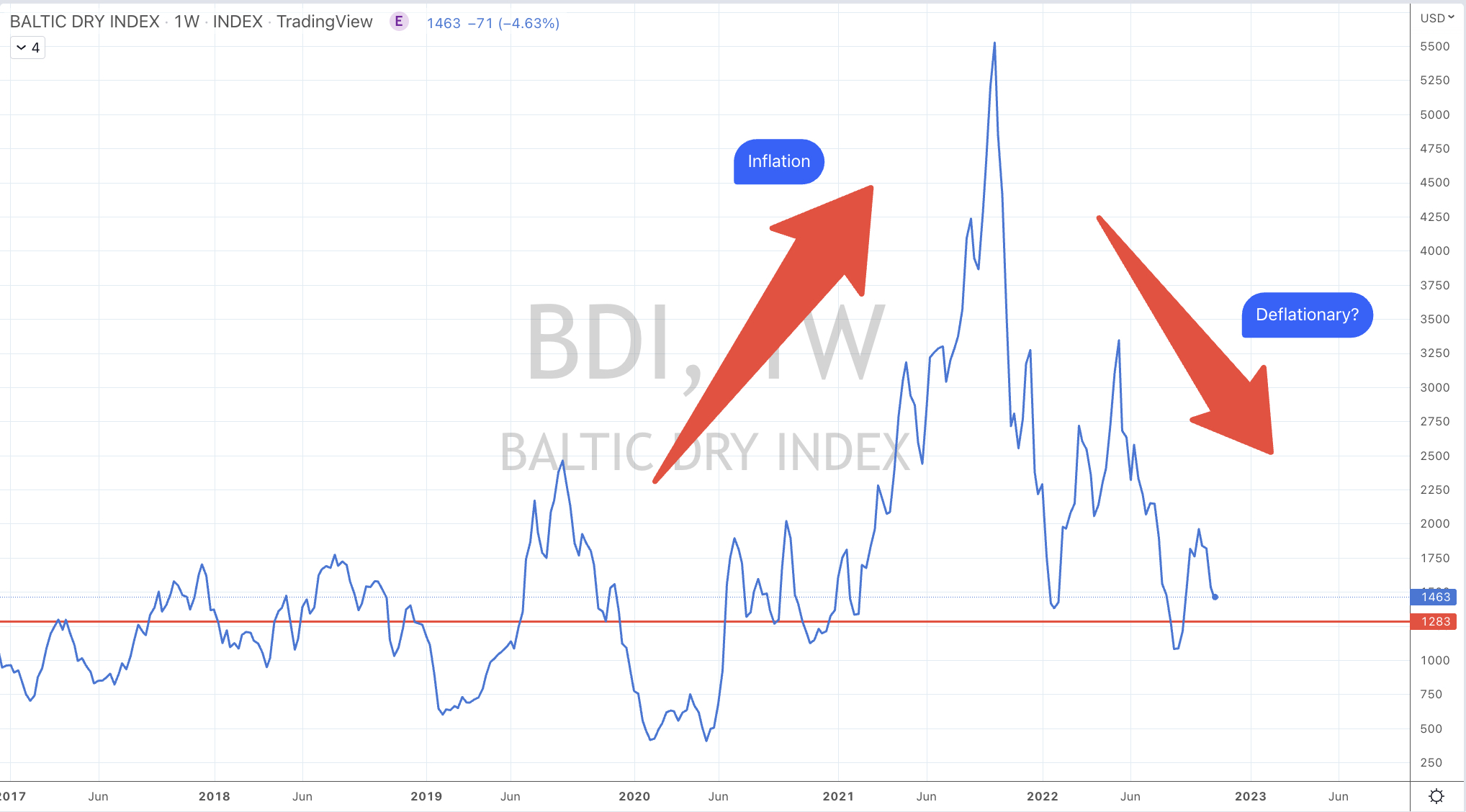

On the downside over the last fortnight, Hot Rolled Coil Steel has eased 11%, Rotterdam Coal has fallen 21% and the Baltic Dry Index has tanked 29%.

And don’t let the news headlines fool you. Even with wheat being blockaded from leaving Ukraine, the price of Wheat is flat over the past 2 weeks.

The larger advancers over the past week comprised of;

Aluminium 7.7%, Bloomberg Commodity Index 5.1%, Cocoa 5.7%, WTI Crude 5.4%, Copper 7.5%, Copper/Gold Ratio 5.5%, Coffee 3.5%, Natural Gas 12.6%, Nickel 6%, Orange Juice 6.3%, Gasoline 6.7%, Sugar 3.4%, Silver 8.3%, CRB Index 5.5%, Cotton 20.6%, Brent Crude 4.7%, Urea Middle East 6.8%, Silver in AUD 7.3%, Gold 2.2%, Oats 6.6%, Rice 7.2%, Soybeans 4.4%, Wheat 2.2%, S&P GSCI 4.6%, Shanghai Composite 5.3%, KBW Banking Index 0.7%, CAC 2.3%, CSI 300 6.4%, DAX 1.6%, MIB 3.3%, HSCEI 9%, Hang Seng Index 8.7%, BOVESPA 3.2%, KOSPI 3.5%, Oslo 3%, Helsinki 2.5%, Sensex 1.7%, Straits Times 2.3%, TAIEX 1.9%, FTSE 4.1%, Istanbul 8% and Australia’s ASX 200 rose 1.6%, for the 2nd consecutive week.

The group of decliners included;

Rotterdam Coal (10%), Baltic Dry Index (13.8%), China Coal (5.7%), Lean Hogs (3.6%), Hot Rolled Coil Steel (HRC) (4.5%), Heating Oil (14%), JKM LNG Gas (4.1%), Lumber (4.4%), Tin (3.4%), Palladium (3%), Dutch TTF Gas (17.6%), Uranium (3.2%), DJ Industrials (1.4%), DJ Transports (0.7%), S&P MidCap 400 (1.2%), Nasdaq 100 (6%), Russell 2000 (2.6%), SOX (1.5%), S&P 500 (3.4%), S&P SmallCap 600 (2.1%) and the Nasdaq Composite fell 5.7%

November 6, 2022

by Rob Zdravevski

rob@karriasset.com.au