A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) either registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

* denotes multiple week inclusion

Extremes above the Mean (at least 2.5 standard deviations)

Spanish, French, Greek and Italian 10 year government bond yields

Natural Gas

India’s Nifty and Sensex indices

Overbought (RSI > 70)

Brazilian 10 year government bond yield *

Biodiesel *

Rubber *

AEX *

KSE

S&P 500

and Taiwan’s TAEIX *

The Overbought Quinella (Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Nasdaq Composite

Philadelphia Semiconductor Index (SOX)

Nasdaq 100

Extremes below the Mean (at least 2.5 standard deviations)

Australian 10 year minus Australian 2 year government bond yield spread *

Australian 10 year minus Australian 5 year government bond yield spread *

U.S. 10 year inflation break-even rate

U.S. 5 year inflation break-even rate

Lean Hogs

CAD/GBP *

COP/USD

EUR/GBP

DJ Transports Index

BOVESPA *

Mexico *

Indonesia’s IDX

And Thailand’s SET equity index *

Oversold (RSI < 30)

Chilean 2 year government bond yield *

North European Hot Rolled Coil Steel *

U.S. Midwest Hot Rolled Coil Steel *

Lumber *

Lithium Hydroxide *

BRL/USD

PHP/USD *

The Oversold Quinella (Both Oversold and Traded at < 2.5 standard deviations below the weekly mean)

RMB/USD

MXN/USD

Notes & Ideas:

Government bond yields were mostly lower, again and notably so.

While readers will see a few European yields in the overbought extremes category; those moments were seen earlier in the week.

Yields have been easing lately, which has been commensurably seen with the Copper/Gold Ratio declining for the past 4 consecutive weeks.

German 5’s and 10’s had outside bearish reversal weeks.

Chilean 2 year yields have fallen for 8 consecutive weeks. Their oversold reading may lead the world in a trough in yields.

The U.S. 10 year yield minus German 10 year yield spread snapped its 8 week declining streak.

And Japanese yields declined for another week.

Equities were mostly weaker, as seen in the All-World ex-USA Index’s decline of 2.4%.

The exception was the Nasdaq, SOX, TAEIX and the S&P 500.

All 4 indices appear in overbought extreme categories, as do India’s Sensex and Nifty.

Amazingly, the Nasdaq 100 has soared 15% in the past 8 weeks.

France’s CAC and Italy’s MIB had a terrible week, both sinking 6%.

The Shanghai Composite, CSI 300, ATX, Bovespa, Helsinki, SET, TSX and the ASX XMJ are in 4 week losing streaks.

While, the Nasdaq Transports Index and FTSE 100 are in 5 week losing streaks.

Budapest and Amsterdam are at all-time highs.

Commodities were mixed.

Cocoa, Oil, Livestock, Gases, Rice and Urea gained the most.

Cocoa has risen 37% over the past 4 weeks of its new winning streak.

While Robusta Coffee snapped its 4 weeks of consecutive advance.

Coal, Aluminium, Nickel were amongst the weakest performers for the week, again.

Lumber and Steel prices remain oversold for a few weeks now. I’ll presume this is a positive for construction industry?

Some grains were weaker too.

And Lithium Hydroxide has now spent 48 consecutive weeks in weekly oversold territory.

Currencies continue to provide action.

The Aussie was higher.

The CHF/AUD has a 4 week rising streak.

The Euro was weaker as was the Yen.

And the PHP/USD broke its 5 week losing streak.

The larger advancers over the past week comprised of;

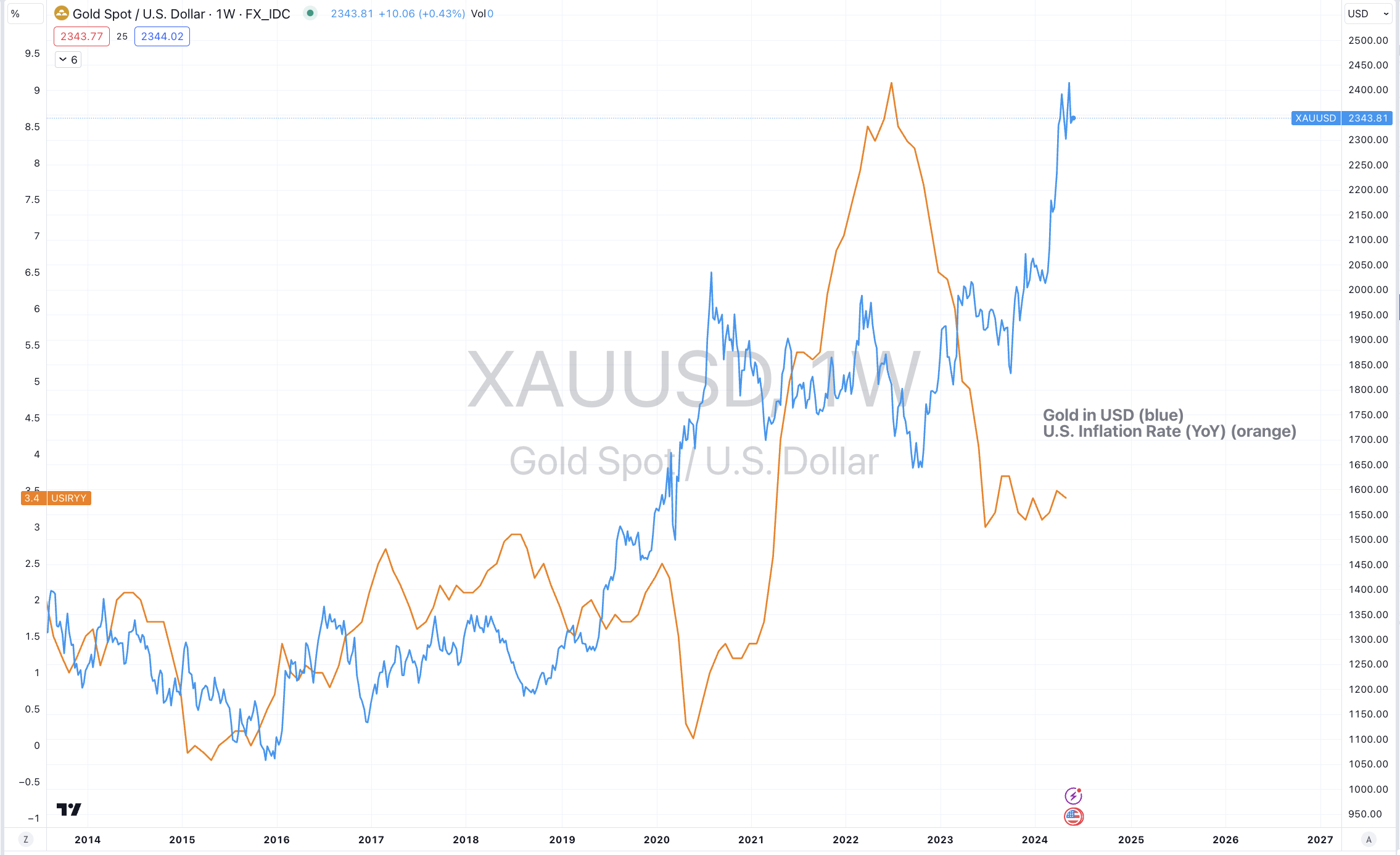

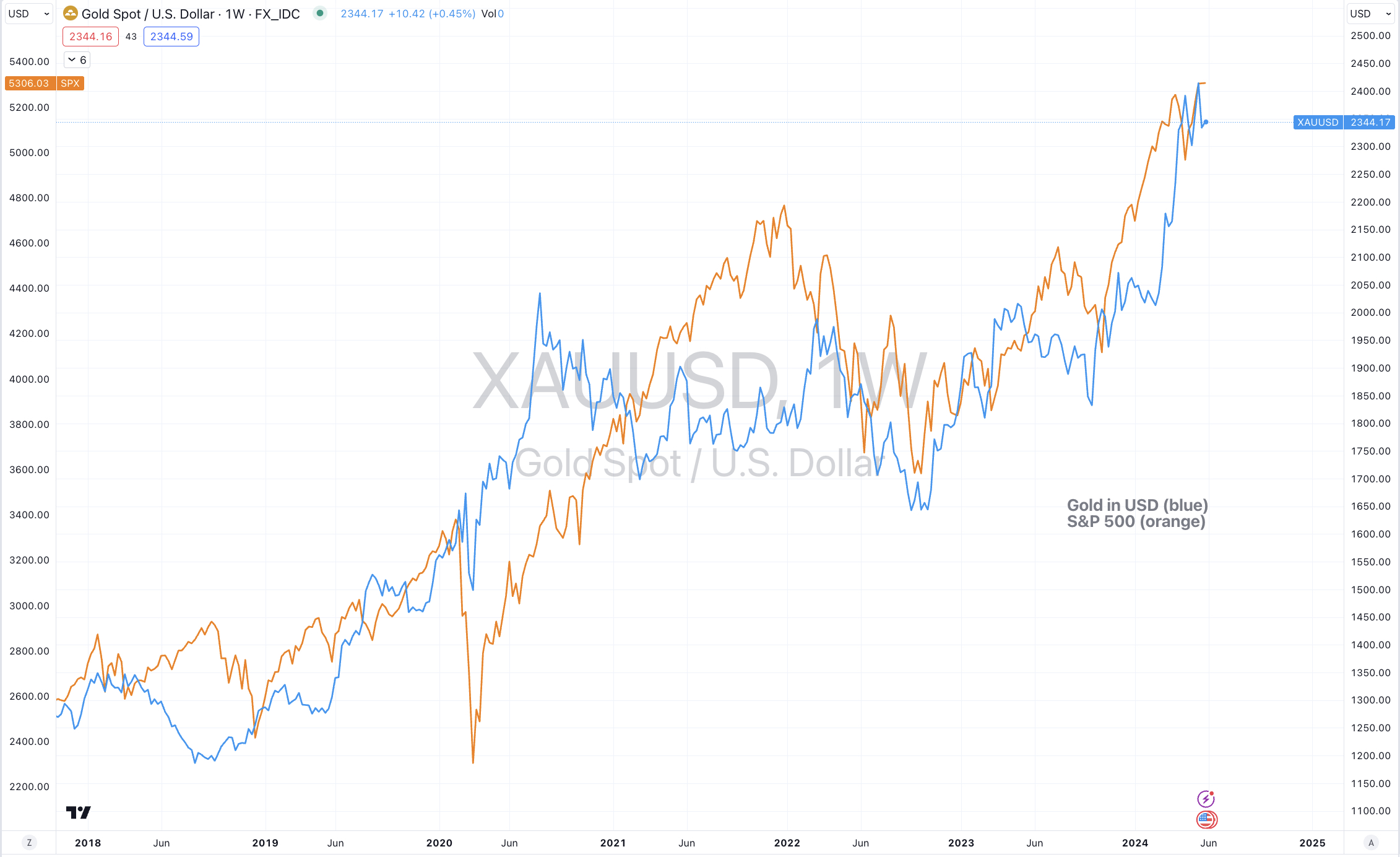

Baltic Dry Index 3.6%, Cocoa 5.9%, WTI Crude Oil 3.9%, Lean Hogs 4.9%, Heating Oil 4.9%, Cattle 3.4%, LNG in Yen 8.8%, Tin 1.9%, Newcastle Coal 1.6%, Sugar 2.3%, S&P GSCI 1.9%, Dutch TTF Gas 6.8%, Urea U.S. Gulf 5.1%, Brent Crude 3.9%, Gasoil 5.5%, Gold in CAD 1.5%, Gold in EUR 2.6%, Gold in GBP 2%, Gold in USD 1.7%, Rice 3.5%, Nasdaq Composite 3.2%, Pakistan’s KSE 4%, Nasdaq 100 3.5%, SOX 5.9%, S&P 500 1.6%, BIST 3.3% and the TAEIX rose 3%.

The group of largest decliners from the week included;

Aluminium (2.7%), China Cokign Coal (1.9%), Cotton (2.2%), Lumber (2.4%), Nickel (2.7%), Nickel MCX (5.6%), Palladium (2.7%), Robusta Coffee (3.7%), Oats (5.8%), Wheat (2.6%), All World ex-USA (2.4%), ATX (3.4%), KBW Bank Index (2.6%), CAC (6.2%), DAX (3%), MIB (5.8%), HSCEI (2.1%), HAng Seng (2.3%), IBEX (3.6%), IDX (2.7%), S&P SmallCap 600 (2.1%), KRE Regional Banks (2.3%), MCX (2.1%), Oslo (2.2%), Copenhagen (2.4%), Helsinki (2.2%), Stockholm (2.4%), PSE (2.1%), SET (2%), SMI (1.7%), Chile (1.7%), XJO (1.7%), ASX Materials (4.3%), ASX Industrials (2.4%) and the ASX Small Caps fell 2.2%.

June 16, 2024

by Rob Zdravevski

rob@karriasset.com.au