Macro Extremes (week ending August 13, 2021)

August 15, 2021 Leave a comment

The following assets (on a weekly timeframe) registered an Overbought reading or traded more than 2.5 standard deviations above its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations)

Cocoa

Sugar

USD/KRW (meaning a weak Korean Won)

Germany’s DAX

Overbought (RSI > 70)

Tin (for the 16th week)

Hot Rolled Coil Steel (for the 46th consecutive week)

Switzerland’s SMI equity index (for the 10th week)

Australia’s ASX 200 (for the 4th week)

India’s NIFTY-50 equity index

France’s CAC-40 index

the S&P 500 and Nasdaq 100

and the Oslo, Stockholm, Copenhagen and Helsinki equity indices.

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Amsterdam’s AEX index

Italy’s MIB equity index

Assets (securities) within my immediate universe which touched the other side of the extreme, being Oversold (where the RSI is < 30) or were at least 2.5 standard deviations below its mean are;

Extremes “below” the Mean (at least 2.5 standard deviations)

Gold, Silver & Platinum (all oversold extremes occurred on Monday, due to a large Gold sell order and the precious metals are reacted suit)

Oversold (RSI < 30)

Chinese Government 10 year bond yield (suggesting bonds where being bought aggressively)

The Oversold Quinella – Both Oversold and Traded at < 2.5 standard deviations above the weekly mean)

Nil

Notable deletions from last week’s list include;

a range of Government 10 Year bond yields and Chinese related equity indices from their Oversold extremes.

Notes & Ideas:

Since their recent overbought readings, energy commodities continued to decline and seeming to commence new downtrends.

The decliners included Iron Ore (4%), Lumber (10%), Natural Gas (7%), Taiwan’s TAEIX (3%).

Advancers were dominated by soft commodities where Sugar rose 6.8% for the week (adding to last week’s 7%), Wheat climbed 6%, Soybean & Corn advanced 2%, Coffee soared 6%, Platinum bounced 5%, while equity indices such as the Swiss SMI, Italy’s MIB and the U.S. KBW Banks rose 2%.

It’s worth to review two of the major longer term (Lean Hogs and Lumber) Overbought extremes seen in the earlier part of 2021. They are now 30% and 71% below their respective June and May highs, and yet they are not yet ‘Oversold’.

While, this past week saw Wheat close at its contract high since February 2013.

The 10’s remain bound in a larger range but we watch it as broader capital markets could become explosive is the 10’s break decisively either below 1.15% or above 1.45%. They closed on Friday at 1.28%.

The risk of lower commodity prices remains as the U.S. Dollar Index (DXY) strengthens and trends higher, although the DXY needs to break above 93.10 to confirm so.

The Copper/Gold ratio seems to be trending higher, telling us the economy is healthy. A turn lower will change this view and aid the correlation of lower interest rates.

The Australian 10 Year Government bond yield continue to trend lower, although the trend and yields seem close to bottoming. A lower yield will correlate with a weaker AUD while the Kiwi 10 Year bond yields are establishing an early, new upward trend.

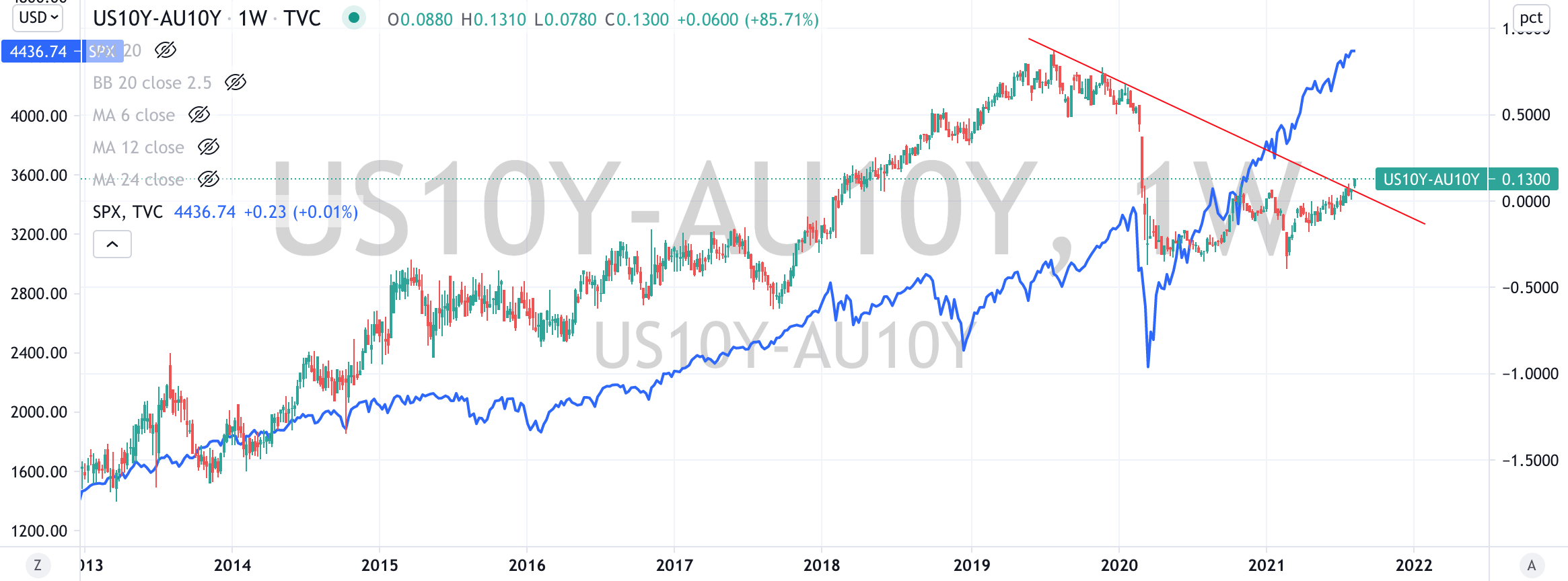

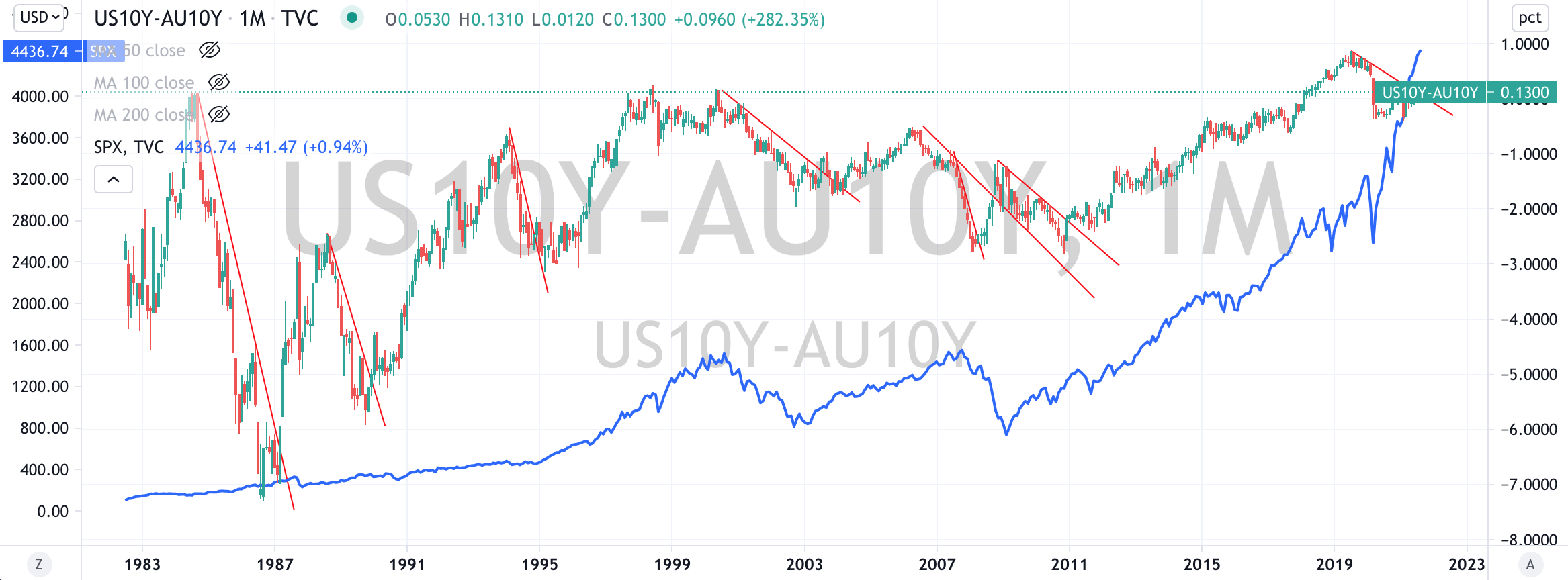

This in turn will affect the US 10 year minus Australian 10 year yield spread the most interesting indicator to watch. Last weeks poke higher (to a 2.5 standard deviation extreme) and subsequent reversal suggests a weaker S&P 500 for the next 2 weeks.

Another risk indicator to watch is the AUD/JPY. Whilst it remains below 81.65, the risk of lower equity prices also remains, especially the divergence currently being seen against the S&P 500.

And I continue to watch the Japanese 10 Year bond yield which needs to stay above 0.00% to assist a bullish equities case. It’s currently 0.009%.

What a week coming up !

No cryptocurrencies registered any Extreme readings.

And lastly, Bitcoin is trading 215% above its 200 Week Moving Average, which is higher than last week’s 200% reading and notably higher than the reading of 140% seen 2 weeks ago, while certainly lower when compared to its 466% peak in mid-April 2021.

August 13, 2021

by Rob Zdravevski

rob@karriasset.com.au