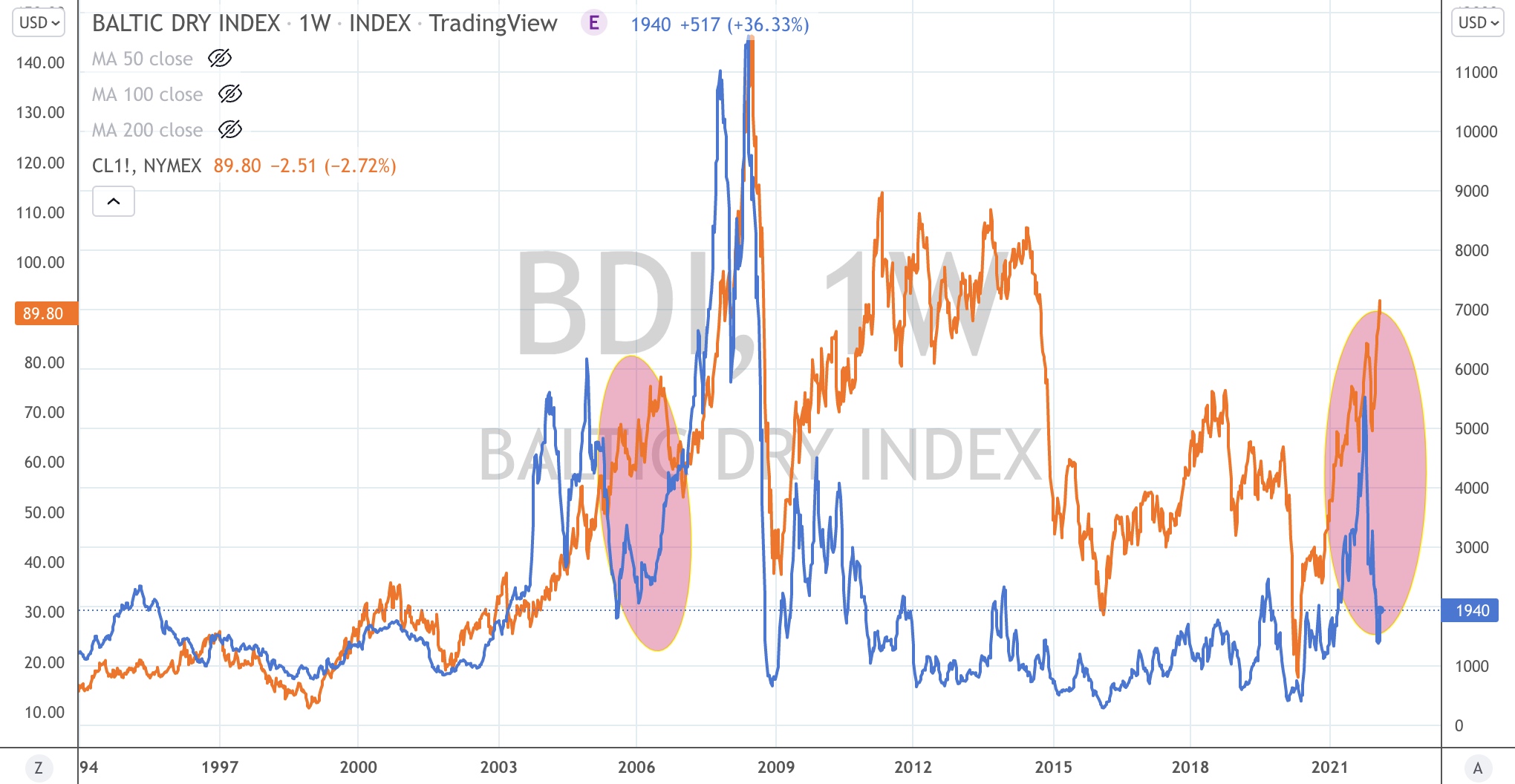

The coming convergence between the prices of the Baltic Dry Index (BDI) and West Texas Intermediate (WTI) Crude Oil.

There have been 2 distinct divergences between the prices of these two prices over the past 30 years.

We are in amongst one of them now.

I’ve recently written about the ‘satisfied’ lows in the BDI and only days ago, cited Overbought conditions in the WTI as its poised on a ‘support’ line.

My bet is that shipping prices rise again and the price of oil moderates.

With recording its 7th straight “up” week (those streaks don’t occur too often) along with a Weekly Overbought RSI, next month OPEC+ will increase output by 400,000 barrels and oil rig counts are rising….and then, what if, what if Ukraine/Russian tensions subside??

I’ll watch if WTI Crude holds this support line.

If not, it may be a quick $8-$9 decline.

It would certainly be welcomed, for rising energy costs will surely crimp corporate earnings in the next couple quarters.

Extremes “above” the Mean (at least 2.5 standard deviations)

Japanese, Chinese and Swedish 10 year government bond yields

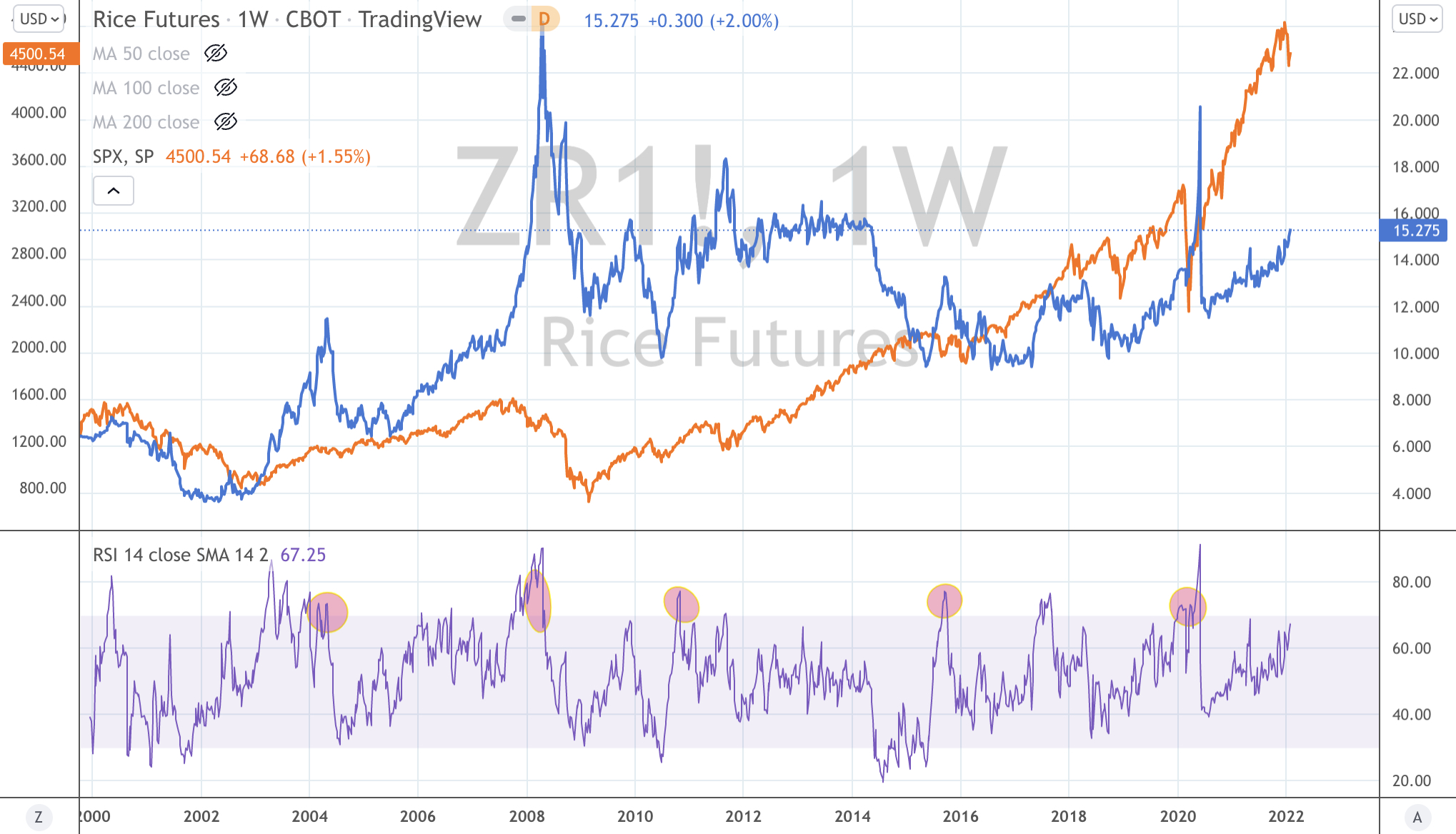

Rice

US dollar Index (DXY)

Palladium

Overbought (RSI > 70)

Australian 2 and 5 year bond yields

U.S. 2 and 5 year government bond yields

Russian, Korean and U.K. 10 year government bond yields

Australian Coal

Heating Oil

Brent Crude

Cattle

Cotton

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

German 2, 5 and 10 year government bond yields

Spanish, French, Greek, Italian and Portuguese 10 year government bond yields

CRB Index

Bloomberg Commodity Index

WTI Crude

Gasoil

Soybeans

Extremes “below” the Mean (at least 2.5 standard deviations)

KBW U.S. Bank Index

Shanghai Composite

CSI 300

South Korea’s KOSPI

Nikkei 225

ASX 200

Oversold (RSI < 30)

U.S. 10 year minus 2 year government bond yield spread

Hot Rolled Coil Steep (HRC)

The Oversold Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

None

Notes & Ideas:

This week’s big news was a combination highs not seen for some time in the CRB Index and certain bond yields.

The CRB Index touched its highest level since December 2014 and is currently Overbought and trading at a notable resistance level. (A previous post makes a call for lower commodity prices)

The biggest move in bond yields was seen in the German 2 year’s which rose from (0.67%) to (0.26%). The German 10’s traded ‘positive’ up to 0.2%, for the first time (and their highest) since April 2019.

The yields in the U.K. Gilts haven’t seen their current level since October 2018 and the JGB’s (Japan) are re-visiting their January 2016 levels.

On the other side of the bond market, saw the Chinese 10 year yields at their lowest since May 2020.

While the U.S. yield curve has flattened and is at its lowest since October 2020. This is a reasonably positive signal for equities, which I highlighted in this article, dated July 8, 2021.

Meanwhile Gold is trading around an important support level….

And today, 1 barrel of Oil is buying the least amount of ounces of Gold since April 2019, thus moving back into its historically average range. I monitor this via the Crude (WTI) Oil / Gold ratio.

Amongst the agricultural’s, the price of rice is seldom discussed, yet it is rising and often carries more acute concerns around food security.

The chart below also shows the coincidence of when a parabolic move in Rice (accompanied by an Overbought weekly) signal, also leads to a temporary peak in equities resulting in either a decline or sideways travel.

In other news, equity markets bouncing from oversold levels seen 10 days ago. One example is Korea’s KOSPI bouncing 3.3% off a 14 month low

And we’ll watch the AUDJPY.

The larger advancers over the past week comprised of;

WTI Crude 6.3% (up 21% in 5 weeks), Gasoil 6.2%, Australian Coal 6.2%, Bloomberg Commodity Index 2.3%, Baltic Dry Index 3%, Cocoa 7%, Copper 4.1%, Heating Oil 3.2%, HRC 1.7%, Coffee 2.5%, Lumber 4.4%, Nickel 2.9%, Platinum 1.8%, Gasoline 5.5%, CRB Index 3.3%, Brent Crude 2.3%, urea 3%, Rice 2%, Soybeans 5.7%, Oats 8.2%, Cotton 2.4%, KBW Bank Index 4.2%, HSCEI 4.6%, Hang Seng 4.3%, Kospi 3.3%, Midcap 400 1.8%, Nasdaq 100 1.7%, Nikkei 225 2.7%, Sensex 2.5%, Oslo Bors 1.9%, Russell 2000 1.7%, Philadelphia Semiconductor Index (SOX) 4.5%, S&P 500 1.6%, Straits Times 2.6% and the ASX 200 rose 1.9%.

The group of decliners included ;

Japan Korea ‘JKM’ Marker (5.5%), Orange Juice (8.4%) – remember to was Overbought last week, Dutch TTF Gas (9.9%), Corn (2.4%), Whet (2.9%), Palladioum (3.6%) and Istanbul (2%).

In the absence of value, using the word ‘blue chip’ as your margin of safety when buying shares is perilous, as Facebook’s 25% one day decline clearly illustrates.

I’ve been banging on recently about pending mean reversions in the price of many assets. In today’s news, it’s Facebook’s (Meta) turn.

They reported poor quarterly earnings and the stock has fallen 23% in after-market trading.It’s going to erase some serious market capitalisation.

It’ll be wiping out the same amount as the combined sharemarket value of ANZ Bank, National Australia Bank, Westpac Bank, Wesfarmers and Telstra.

Facebook’s stock price is well on its way to a long term mean reversion.

In my charts (see below), I use a 200 week moving average. I want to reiterate, this is a 4 year rolling mean.

I’m not rejoicing the decline but I’m highlighting that when managing investment portfolios, ‘alpha’ can be strangely achieved by not owning assets which are overpriced or perilously stretched.

As I don’t short stocks, telling people when to stay away doesn’t show up in any performance reports.

said, “Meanwhile, the other three of the “FAANGM’s gang, being Netflix, Amazon and Facebook have already broken below their corresponding (or sympathetic) support lines.”

The Thomson Reuters (core commodity) CRB Index hits its highest level since November 2014.

Weightings are particularly heavy towards energy and agricultural contracts.

The CRB is a whisker away from the target mentioned in this story written a few days ago, while the AUDUSD has hit my target of 0.7135.

This is part of my call of a peak for broader commodity prices.

Just take a look around the prices of Oil, Gasoline, Heating Oil, Corn, Wheat, Coffee, Cattle, Oats etc etc.

Also, the price action in Crude Oil is suggesting the recent run is waning.

#meanreversion

In turn, I am not owning any related equities across Oil & Gas, Bulk producers of grains and even miners of raw industrial/base metals.

It’s as good as it’s going to get for in this current wave.

So, what else to do…..

Well, I’ll wait…..

then I’ll watch the stock prices of companies who buy these raw commodities such as Kellogg, Starbucks, Kraft Heinz, Nestle, Nucor or Nippon Steel, as their input costs will fall, thus improving their margins.

…….also, the unloved precious metals are worthy of some attention, while the AUD/USD isn’t acting very constructively.

To many, it might seem perverse to Buy USD (and sell your AUD 0.7130) but that is what the market is telling me.

I’m also seeing divergences in currency correlations.

Take a look at the chart below showing the AUDUSD laid over the CRB Index and then the other is the price of BHP over the same currency cross.

I believe currency before I believe the equity.

For extra kicks, I’ve thrown a chart showing the price of Woodside Energy mimicking the CRB Index.

Geopolitics and machinations of war are the smokescreen for the real M&A play, being Economic.

Much like Ukraine having certain assets or businesses of interest to Russia (Ukraine is the world’s 4th or 5th largest exporter of Iron Ore, Wheat and Corn)……China would like to control Taiwan Semiconductor.

There is no company of meaningful national interest as Taiwan’s……Taiwan Semiconductor Manufacturing Company (TSMC)

TSMC is a giant. Its capital expenditure plans for 2022 alone will be $44 billion.

Japan is courting them to open up facilities or move more of their operations there.

Certain states in the U.S. have offered TSMC incentives to move there, with a new plant being built in Arizona.

With 54% global market share of the semiconductor foundry market, it’s no wonder.

These guys build and design a bucket load of the world’s semiconductor chips.

Furthermore, they make 92% share of the world’s most sophisticated and advanced chips found in phones, cars etc.

They are the exclusive provider of chips in Apple’s iPhones and most Mac computers.

In fact, Apple accounts for 25% of TSMC’s annual revenue of $57 billion.

Qualcomm, Broadcom, AMD and Nvidia are also major customers. Or put another way, they rely heavily on TSMC.

TSMC is also an important company for the United States.

And TSMC knows it.

Under the category of self-interest, this is why the world is either trying to either lure them towards their shores or help protect them (and their self-interest) out of fear that TSMC falls under Chinese control.

To illustrate the level of TSMC’s national importance, if we look at the $21 trillion GDP of the United States, its largest company, Apple has a market cap of $2.9 trillion. Then Microsoft is at $2.3 trillion, followed by Google at $2 trillion while Amazon is $1.55 trillion.

Germany has a GDP of $3.8 trillion.

Its largest company market caps are SAP at $165 billion, Siemens and Volkswagen are $130 billion, Allianz is $105 billion while Merck, Daimler and Deutsche Telekom are all around $90 billion each.

While Japan’s GDP is $5 trillion, Toyota’s market cap is $248 billion and Sony is $148 billion

and within Australia’s GDP of $1.3 trillion, the listed market caps of its national goliath’s include BHP at $169 billion, Commonwealth Bank is $168 billion and CSL comes in at $130 billion.

In Taiwan, its GDP is $760 billion.

Taiwan Semiconductor has a market capitalisation of $613 billion.

No other company globally comes close to having a market cap as large as the whole of its ‘home’ nations entire annual GDP.

Across various measures, Coffee is overbought and stretched.

In the chart below, the month of December 2021 shows the contract price of Arabica coffee at 105% above its 200 weekly moving average.

It’s quite uncanny that “105%” has been seen at previous peak moments.

And remember, parabolic moves are often met with a sharp retracement. The price should eventually come back and kiss that 200 week average.

A falling coffee price bodes well for companies such as Nestle and Starbucks. These companies can acquire beans at cheaper levels but not necessarily reduce their retail prices.

They can justify any backlash by citing rising labour or wage costs.

By the way, just like the price of beer, I’ve never seen the price of coffee decline at the retail and premium level.

So, in other words, the price of coffee beans may halve but the price of your coffee beverage will firm.