Today’s price of WTI Crude Oil is the same as it was 3 weeks ago (on February 4th). Doesn’t that sound astonishing in light of ‘Russia’s move into Ukraine territory’.

‘Tops’ often happen earlier than you may care to remember.

It seems that investors and/or market commentators forget when the peaks actually occurred.

In the charts below, I’m showing you the peak in Salesforce.Com and PayPal occurred in November 2021 and July 2021 respectively.

Many may think the peaks were only in the last few weeks.

I think Russia and Ukraine may re-unite in the years to come. It’s quite plausible.

I predict that Ukraine will do so willingly following a few more years of economic coercion by the Russians.

Some other questions I’m debating include;

In terms of its citizens, are Russian’s and Ukrainian’s actually ‘brothers’ and ’sisters’?

Well, polls I have seen suggest that Ukrainian’s view Russian’s in a favourable light.

While I understand the ideology, Ukrainian politicians will tow the line of protecting their sovereignty because they would not be able to reap ‘corruption dollars’ if they are swallowed by Putin and Russia.

Perhaps a ‘merger’ is better for the Ukrainian citizens but not for the corrupt elite and more so, the politicians?

Ukraine is Europe’s most corrupt nation, ranking 122nd out of 180. Russia isn’t any better with a rank of 136.

It would be foolish to believe that people become politicians in highly corrupt nations driven by an urge of public service.

Let’s take the current Ukraine 🇺🇦 political set-up.

President Zelensky was a comedian and sitcom actor.

He is funny.

In 2003, Zelensky co-founded a television entertainment production company called LLC Kvartal 95.

One of his best mates from childhood, Ivan Bakano was the head of LLC Kvartal 95.

In May 2019, Bakanov was appointed as First Deputy Chief of the Security Service of Ukraine (SBU), while Vasyl Hrytsak was the Head of the Security Service.

Following this announcement, Hrytsak went on vacation, and Bakanov began to perform his duties.

Hrytsak never returned to his post in the SBU and Zelensky officially appointed Bakanov as his successor on 29 August 2019.

The star of the TV shows is now the President and his childhood friend is the head of the intelligence services.

The October 2021 Pandora Papers revealed that Bakanov and Zelensky and his chief aide, Serhiy Shefir (another co-founder of the TV production company), operated a network of offshore companies in the British Virgin Islands, Cyprus, and Belize. These companies included some that owned expensive London property.

On February 1, 2022, Boris Johnson meets Zelensky in Kyiv offering aid to the tune of GBP 1.7 billion pounds to help build naval bases. Johnson also said the U.K. will provide an additional GBP 2 billion pounds for joint infrastructure and energy projects.

The news flow actually carries onto other promises too.

You couldn’t make up this stuff.

Irrespective, how the media frames the current palaver, does Johnson think building naval bases can be completed quick enough to pose a deterrent to the current situation?

Hey Boris, building naval bases isn’t a quick proposition.

Secondly, I bet British taxpayers won’t be too impressed with this.

Let’s see how much of British naval base building money makes its way into bank accounts controlled by Zelensky, Bakanov & Shefir.

While I see rotation in amongst sectors and various buying opportunities in equity markets appear, Tesla is not one of them.

Further risk and declines in Tesla’s stock price and a few other stocks which have distorted indices are the reasons why ‘the market’ could fall further.

Within this ‘market’, continue to pick out the stocks which are cheaper and ripe for some (stock)picking.

Russia says they will not invade Ukraine and are open to using diplomacy while America says they will invade and are poised to do so very soon.

I believe Russia will not initiate an invasion.

Firstly, Putin doesn’t have the money nor the troops.

Also, you don’t invade in the mud. You wait until the ground has dried.

However, Russia will retaliate and blame NATO if they throw the first stone.

Russia may already have a claim if they cite the threats of sanctions.

For the U.S. has already sanctioined companies involved in the NordStream 2 pipeline. Germany isn’t happy.

An outlier call is that Russia walks across the border and Ukraine accepts their terms of a ‘merger’.

My belief is that Biden is ‘creating a war’ for various reasons. He needs to improve his fall in the polls and he’ll do that by being tough on Russia (and China) while also increasing government spending.

Remember than Obama was softer and friendlier to Russia, which included assisting Russia joining the WTO in 2012.

Obama was also continuing the austerity measures adopted at the end of the Global Financial Crisis.

The Democrats lost heavily in the 2014 midterm elections and Biden has not forgotten Obama’s soft and friendly stance.

With Biden’s infrastructure spending bill not being passed, another way he can spend money is to increase military expenditures, especially as the Iraq and Afghanistan campaigns have ended.

The charts below show the ebbs of current U.S. military spending in the form of 1) as a percentage of GDP and 2) as a percentage of general government expenditure.

Beyond flooding his mates in Ukraine with more American weapons and ammunition, other incentives for Biden to cite that a war is imminent is that he’ll be able to blame Russia’s aggression for the higher oil and gasoline prices his citizens are experiencing.

(It’s also plausible Ukraine has some ‘dirt’ on the Biden’s too)

In turn, higher energy prices creep into corporate operating costs which may lead into a lower GDP figure in the coming quarters.

Then corporations can also be blamed for passing on higher costs.

The main point is that Biden isn’t blamed for rising costs and inflation because he really needs to wins these mid-term elections in December.

Also, have you noticed France’s involvement in trying to broker talks.

In 2019, Macron declared NATO brain-dead.

Today, Macron has ‘arranged’ for a summit between Putin and Biden.

In the interim, I am surprised by Blinken’s rhetoric recently changing from pacifist to belligerent, to side more with Biden’s stance.

This is contrary to the paper Blinken wrote in 1987, titled Ally vs Ally.

Should Biden ‘negotiate a retreat’, he will certainly take credit for his toughness hoping this elevates his standing in the polls.

Although, if a war does eventuate, it’ll be brought to you by CBS News, CNN and the lobbyists for various U.S. military manufacturers and suppliers.

The following assets (on a weekly timeframe) registered an Overbought reading or traded more than 2.5 standard deviations above its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations)

German 5 & 10 year government bond yields

U.S., Japanese & Portuguese 10 year government bond yields

KBW Banking Index

Gold (in AUD)

Overbought (RSI > 70)

Australian 2, 3 and 5 year government bond yields

U.S 2 & 5 year government bond yields

Korean, Russian and New Zealand 10 year government bond yields

CRB Index

Bloomberg Commodity Index

Australian Coal

Aluminium

Tin

WTI Crude

Cattle

Soybeans

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Australian 10 year government bond yields

Spanish, French, Greek & Italian 10 year government bond yields

Lean Hogs

And Singapore’s Strait Times Index (for 2 consecutive weeks)

Assets (securities) which touched the other side of the extreme, being Oversold (where the RSI is < 30) or were at least 2.5 standard deviations below its mean are;

Extremes “below” the Mean (at least 2.5 standard deviations)

CSI 300

Helsinki OMX 25

Oversold (RSI < 30)

U.S. 10 year minus 2 year government bond yield spread

Hot Rolled Coil Steel (HRC)

The Oversold Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

None

Notes & Ideas:

The big news is the careering of short duration bond yields into the stratosphere. Government 2 and 3 year bonds are now where 10 year bonds were yielding only 5 months (October 2021) ago.

After 6, 7 or 8 consecutive rising weeks, streaks come to an end and that was the case for many energy prices.

As was the case for last week’s overstretched prices in Coffee & Cotton.

Incidentally, Gasoline, Heating Oil and forward contracts in WTI Crude made bearish outside reversal weeks.

There is merit in referring back to the previous few weeks editions of ‘Marco Extremes’ to remind you of the relevance of the watching for the swings in the pendulum.

The larger advancers over the past week comprised of;

Gold 3.1%, Hogs 20.9%, Natural Gas 12.4%, Nickel 2.5%, Palladium 6.6%, Platinum 5.7%, Silver 2.7% and Gold in AUD rose 2.1%.

The group of decliners included ;

Rotterdam Coal (2.9%), Cocoa (6.1%), WTI Crude (3.1%), Gasoil (1.9%), Heating Oil (4.5%), JKM (3.1%), Coffee (2.4%), Lumber (3.5%), Gasoline (2.5%), Cotton (3.3%), Dutch TTF Gas (4.7%), Oats (8.4%), KBW Banking Index (3%), AEX (2.2%), DAX (2.5%), Dow Jones Industrial (1.8%), Milano MIB (1.7%), HSCEI (2.8%), Hang Seng (2.3%), IBEX (2.4%), MOEX (4.3%), Nasdaq 100 (1.7%), Nikkei 225 (2.1%), Oslo (2%), Copenhagen (2.8%), Helsinki (2.9%), Stockholm (4.2%), Swiss SMI (1.8%), FTSE 100 (1.9%) and the S&P 500 fell 1.6% (having fallen 3.4% in the past 2 weeks.

This chart below (and commentary) shows you when you should be buying Aluminium or associated proxies (such as Alcoa) and the power of operational leverage that a corporation can provide shareholders.

The blue line is the rolling 200 week moving average.

Gravity does exist.

While the theme of “having industrial capacity in moments of output gaps” remains intact, at this moment, it is a sellers market.

Beware of chasing the bullish (metals and energy) commodity prices higher.

It’s also the start of an odd period where higher prices of finished goods (due to the higher price paid by buyers of raw/base/industrial commodities) may be left on the shelf.

Rising prices have been evident but we can’t assume that higher prices are automatically paid for.

I’m watching if Woodside Energy’s (WPL.AX) stock price breaks $27.60 this week.

If it does, it portends a move to the $30 level into a late March/early April window, with $30.85 being major resistance.

A break above $27.60 means the stock is making a ‘higher high’ than the same price seen in January 2021.

This is a market where I’m watching whether stocks are making ‘higher highs’ or ‘lower lows’ than their previous mark.

The overall message is that it’s a sellers market at these various levels.

And if the $27.60 level fails to be broken, selling at $26.50 (on the way down) will also be appropriate.

Buyers at today’s prices are playing for the last possible 10%, while medium term downside is 15% (back to $23.40)… makes for a terrible risk/reward consideration.

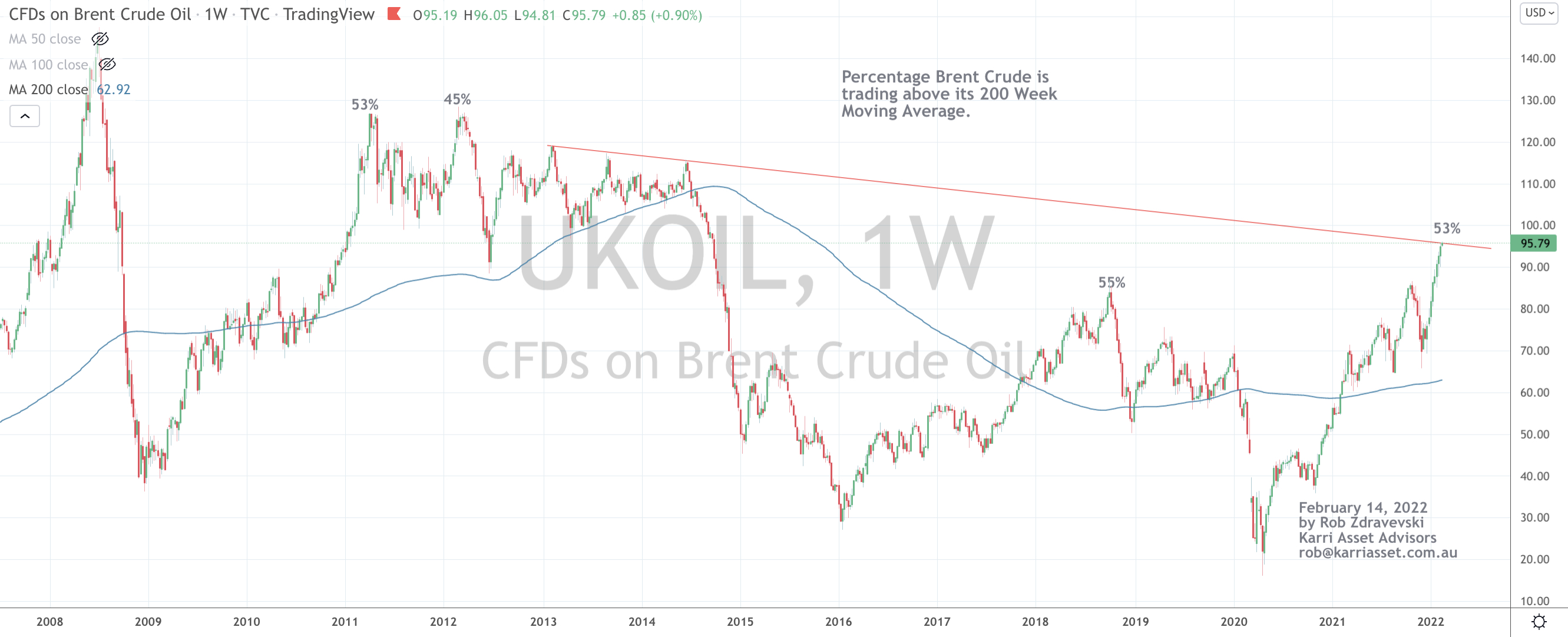

Coinciding with my Overbought Brent note (which I published immediately prior to this), Woodside’s stock price is also overbought on a Weekly basis and only its 6th such occurrence since 2007.

Furthermore, Woodside is mean reverting towards its 200 week moving average (that’s the blue line on the chart below).

The following assets (on a weekly timeframe) registered an Overbought reading or traded more than 2.5 standard deviations above its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations)

U.S. 10 year government bond yields

KBW Banking Index

Cocoa

Copper

Rice

Palladium

Overbought (RSI > 70)

Australian 2, 3 and 5 year bond yields

Russian and New Zealand 10 year government bond yields

CRB Index

Bloomberg Commodity Index

Australian Coal

Aluminium

Tin

Heating Oil

Brent Crude

WTI Crude

Gasoil

Gasoline

Cattle, Cotton and Coffee

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Australian 10 year government bond yields

U.S. 2 and 5 year government bond yields

German 2, 5 and 10 year government bond yields

Spanish, French, Greek, Italian, U.K. Japan, Korean, Swedish and Portuguese 10 year government bond yields

Soybeans

And Singapore’s Strait Times Index

Assets (securities) which touched the other side of the extreme, being Oversold (where the RSI is < 30) or were at least 2.5 standard deviations below its mean are;

Extremes “below” the Mean (at least 2.5 standard deviations)

Shanghai Composite

CSI 300

South Korea’s KOSPI

ASX 200

Oversold (RSI < 30)

U.S. 10 year minus 2 year government bond yield spread

Hot Rolled Coil Steel (HRC)

The Oversold Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

None

Notes & Ideas:

The big news is the careering of short duration bond yields into the stratosphere. Government 2 and 3 year bonds are now where 10 year bonds were yielding only 5 months (October 2021) ago.

Subjectively, this tells me rate rises are being factored into and the longer bond yields are a better indicator than the distorted short end.

Watch for retracements following parabolic price moves.

Equities were mostly higher global for the week, with the exception of major U.S. indices. Asian equity markets caught a bid (whilst remaining unloved), Korea’s KOSPI is bouncing off an Oversold position while the U.K.’s FTSE 100 is approaching Overbought territory.

In other ‘big news’, the price of shipping soared 39% for the week.

The pullbacks and predictions of a low appear here;

It’s no surprise to see lower Gasoline and Gas related prices lower, while recent extremes in currencies have abated.

In other tidbits of interest, the SOX is trading at the same price as last June (2021), WTI Crude, albeit squeezes out a 8th consecutive ‘up’ week, although it only rose 0.9% for the week amidst Russian/Ukraine tensions and Bitcoin can’t close above $44,000 on a weekly basis.

Continuing from last week, he CRB remains Overbought, German 10 year bond yields are above Zero, a bunch of bonds yields (as per last week’s ‘Extremes’) are at multi-year highs,

Inversely, not many think yields or commodity prices can retrace or abate…

Reiterating at week’s comment, the U.S. yield curve has flattened and is now at its lowest since March 2020. This is a reasonably positive signal for equities, which I highlighted in this article, dated July 8, 2021.

And I’m also repeating that 1 barrel of Oil is now buying the least amount of ounces of Gold (the Oil/Gold Ratio is $19.80) not seen since April 2019.

In fact, the Oil/Gold ratio is now back to $19.80, a level not seen since April 22, 2019.

Incidentally, that date also signalled the high in WTI Crude Oil and was followed by a 23% decline over the next 6 weeks. That peak was not re-broken until March 2021.

Equally, Copper put in a high of $3.00 that week, to then dropped 33% over the next 11 months.

That peak of $3.00 was not re-broken until the week of August 3, 2020

Spookily, that decline in Copper from its April 2019 levels, started from a lower low which was 9% below the previous high which was set 11 months earlier.

Today, Copper is 9% below a higher high, which was set 11 months earlier.

Inversely, Gold found a floor that same week and commenced a notable rally from $1,200 and peaked at $2,075 in the week of August 3rd, 2020.

So your trade positioning is exiting your overpriced Oil and Copper exposures (this will aide my Short Commodities and CRB call) and accumulate Long’s in Gold and perhaps other precious metals.

And we’ll watch the AUDJPY whether it makes a higher high or a lower low.

The larger advancers over the past week comprised of;

Aluminium 5.4%, Rotterdam Coal 3.6%, Baltic Dry Index 39%, China Coal 11.4%, Cocoa 5.4%, Gold futures 1.9%, Gold in AUD 2%, Gold in USD 2.8%, Gold in EUR 3.8%, Hogs 4%, Coffee 4.2%, Lumber 13.7%, Gasoline 2.2%, Silver 4%, Brent Crude 2.4%, Corn 4.9%, Oats 2.6%, Soybeans 1.9%, Wheat 4.5%, Shanghai 3%, AEX 1.9%, DAX 2.2%, IBEX 2.4%, FTSE 100 1.9%, HSCEI 2.3%, TAEIX 3.3%, Russia’s MOEX 4.2%, Straits Times 2.9% (rising 5.5% in 2 weeks) and Istanbul 4.6%.

The group of decliners included ;

Gasoil (2.9%), JKM (3.1%), LNG (11%), Natural Gas (13.8%), Palladium (4.2%) down 8% in 2 weeks, Dutch TTF Gas (6.3%) down 17% in 2 weeks), Urea (11.7%), Nasdaq (3%), Philadelphia Semiconductor Index ‘SOX’ (2.5%) and the S&P 500 fell 1.8%.