The market cap destruction of Russian equities is one of the most amazing things I’ve seen in capital markets.

Gazprom’s market cap 2 months ago was $65 billion.

This a screenshot from my phone last night, while trading was happening in Gazprom’s London listed GDR equities.

Last night’s low was 2 cents per share (from US$9.00).

It’s market cap was $250 million.

Trading was halted more than 15 times in the first couple hours during Wednesday’s trade.

The stock closed at 60 cents.

An asymmetric trade

The mind boggles as to the money lost and the speculators (market makers) who made 20 times return, from the low by the end of the close of the day’s trading.

So, let say $1 million was outlaid (which is just as you’d own 0.5% of all of Gazprom) and the asymmetric bet was…buying at 3 or 5 cents means that this stock EITHER goes to Zero (so you lose $1 million) OR it works its way back to $2 (not $5 nor $9), thus making you $40 million.

Easy to say, if you don’t fathom a 100% loss or if the exchange halts trading or your broker no longer allows you to trade the stock or provide custody. (see sizing your bet appropriately)

But, all in 1 day, You are up 12 times….Hmmmm, so what’s next ?

Halve it, Hold, Cut it or something in between?

#asymmetric

* this is a capital markets post, in no way is any humanitarian insensitivity meant.

For those reading/watching my selected stock calls, if you’ve ‘squeezed out’ an extra 10% since I wrote this, Woodside Energy is close to the notable $30.85 resistance.

The following assets (on a weekly timeframe) registered an Overbought reading or traded more than 2.5 standard deviations above its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations)

Gold

Lean Hogs

Palladium

Platinum

Corn

Overbought (RSI > 70)

Australian 2, 3 and 5 year government bond yields

U.S 2, 5 & 10 year government bond yields

German 5 year government bond yields

Spanish, French, Greek, Italian, Japanese, Portuguese and New Zealand 10 year government bond yields

CRB Index

Australian Coal

Aluminium

Gasoil

Tin

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Australian & Russian 10 year government bond yields

Bloomberg Commodity Index

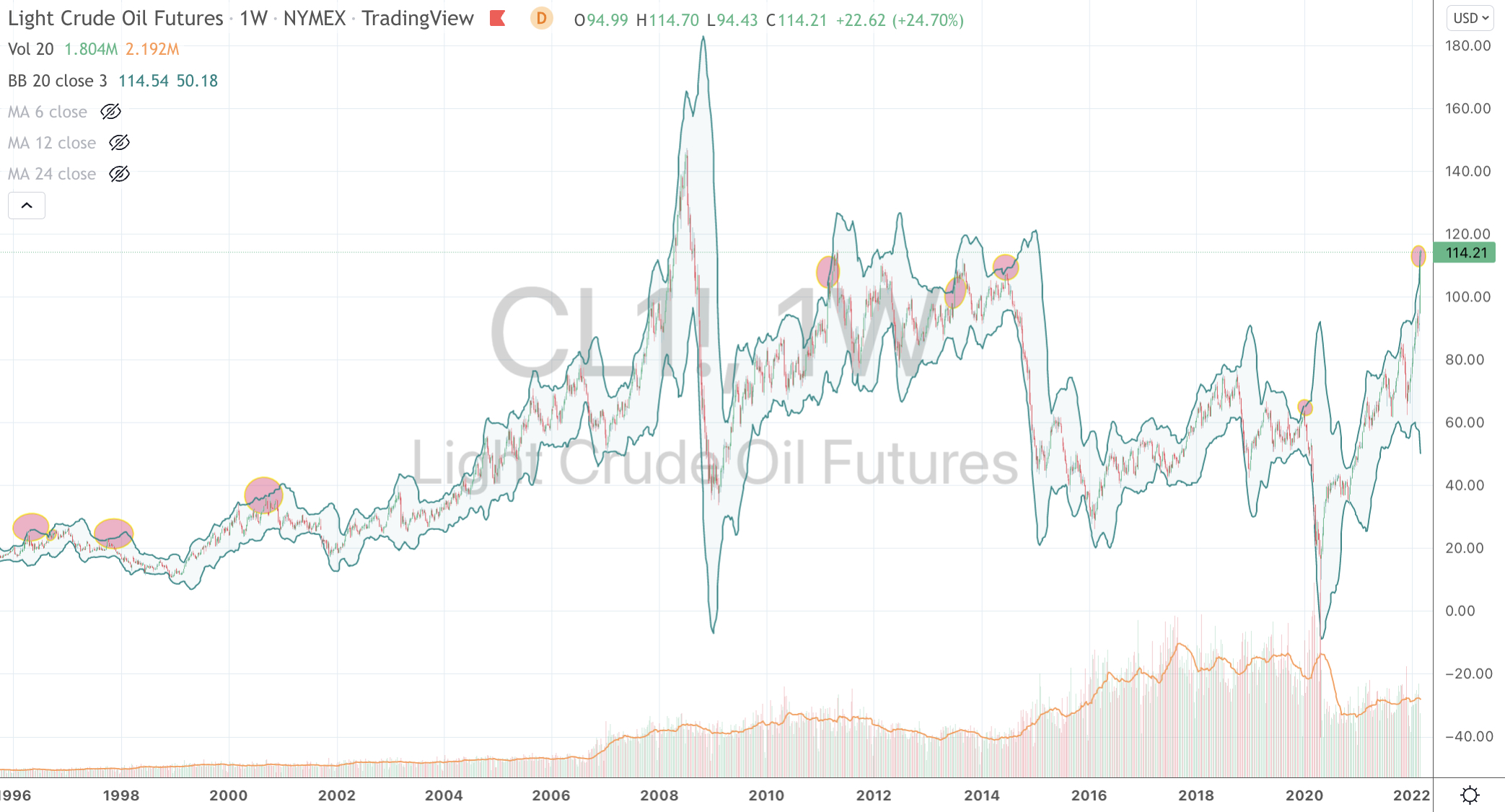

WTI Crude Oil

Brent Crude Oil

Gasoline

Nikkei 225 Index

Assets (securities) which touched the other side of the extreme, being Oversold (where the RSI is < 30) or were at least 2.5 standard deviations below its mean are;

Extremes “below” the Mean (at least 2.5 standard deviations)

Korean Won / USD

AEX, CAC, DAX, DJIA, MIB, IBEX, S&P Midcap 400, Nasdaq 100, Sensex, Copenhagen, Swiss SMI and the S&P 509

Oversold (RSI < 30)

U.S. 10 year minus 2 year government bond yield spread

Hot Rolled Coil Steel (HRC)

Korea’s KOSPI Index

The Oversold Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Russian Ruble / USD (it weakened 8%)

Notes & Ideas:

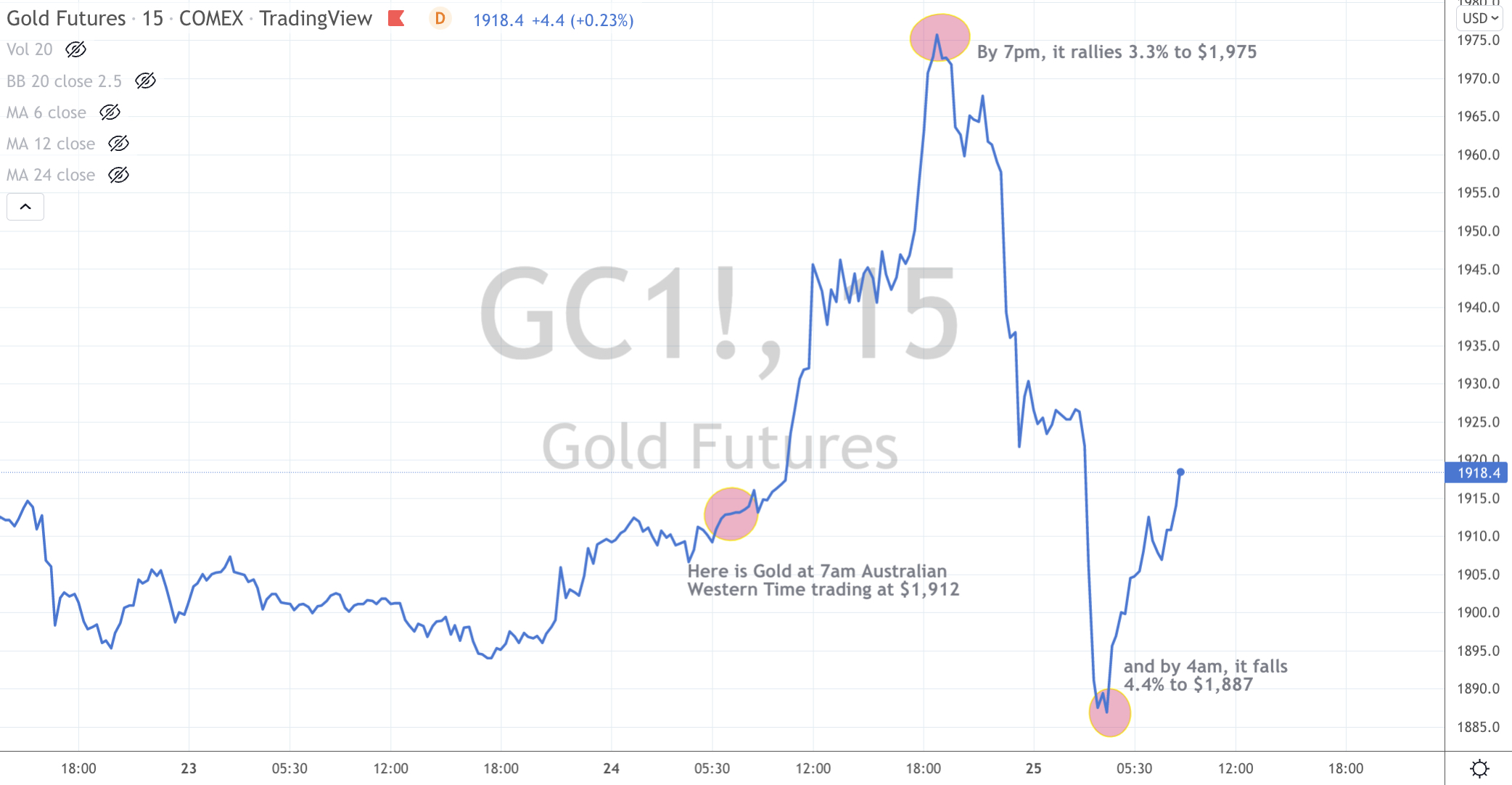

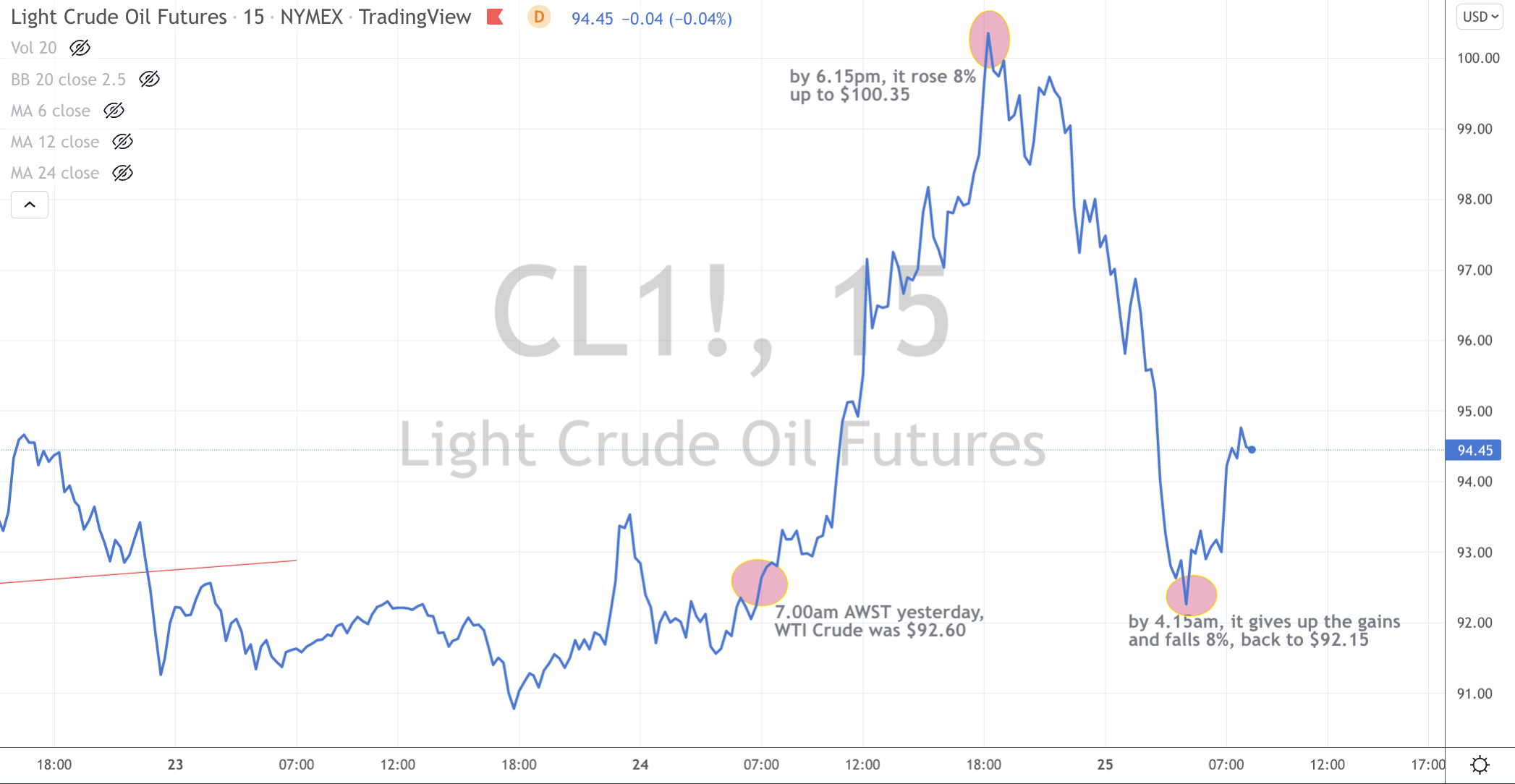

This week’s big news was the savage decline (and reversal) in prices due to the initial reaction of Russia attack on Ukraine.

For example, at their highest points Heating Oil, Natural Gas, Crude Oil, Soybeans and Corn rose between 10%-11%.

Wheat advanced 19% at one stage, Dutch TTF Gas soared 80%, Gasoline climbed 15% and Gold rose 4% to only close ‘flat’ on the week.

On the flip side, the U.S. KBW Banking, DAX and CAC were down 7% at their lowest ebb during the week.

Such volatility is not only a test of one’s metal and resolve but is a costly lesson for those ‘whipsawed’ through their stop losses.

I illustrated some of the intra-day moves in this post.

Russian 10 year bond yields move from 9.8% to 12.2% and Turkish 10’s went from 20.8% to 23%.

However, there are some misnomers in the Oversold equity indices readings as they breached their 2.5 standard deviation moves ‘intra-week’ before reversing higher.

Incidentally, the Baltic Dry Index rose 11% on the week. This measure of the cost of shipping dry, bulk goods is up 68% since my ‘bottom’ call on January 24th.

Since they appeared and were cited in this weekly note a few weeks, Coffee and Orange Juice are down 8% and 13% respectively since they registered Overbought Extremes.

And the ‘surprise’ was the U.S. indices finished in the black for the week.

You can read a note written this week which recalled when U.S. equities rose during the 1991 Iraq aerial attack and how equities rose throughout those 32 days.

I needed to make a note of yesterday’s volatility in Russian equities.

Lukoil fell 57% at one stage to close ‘only’ down 22% on the day.

Gazprom’s intraday low was 41% below the previous day’s close.

After all of that, it closed down 29%.

Sberbank was down 57% at one stage yet closed a respectable negative 37% while TCS Group (a financial services firm) tanked 80% and then rallied to close down 59%.

and the whole index (the MOEX) was down 51% at its lowest point and closed down 33% on the day.

It is extraordinary that a whole index halved in value.

It may be an immediate signal that sanctions had an effect.

Rarer still, some of these moves were 4 standard deviations below their weekly mean.

In this morning’s trading session, these stocks are +10%, (4%), (4%) and +33% respectively, while the MOEX has bounced a further 6%, albeit it seems unconvincing.

Did anyone notice Imran Khan (the leader of the world’s 6th largest army and 8th largest air force) visiting Putin (who is in charge of the world’s 5th largest army and 2nd largest air force)

….only hours after the commencement of the Russian/Ukraine invasion.

Incidentally, Pakistan has a population of 220 million compared to Russia’s 144 million.

News reports say they are “expected review the entire array of bilateral ties including energy cooperation besides exchanging views on major regional and international issues, along with Mr Khan expecting to push for the construction of a long-delayed, multi-billion-dollar gas pipeline to be built in collaboration with Russian companies”.

This makes for interesting analysis especially since Pakistan still receives millions of dollars in aid from the U.S. (notwithstanding Trump having cut $1.3 billion of that flow) including 33 million does of COVID-19 vaccines.

More so, Pakistan pays $10-$13 billion per annum on external debt servicing.

Other ties to watch are between Russia and Kazakhstan.

Kazakhstan happens to be Central Asia’s largest country and has a GDP similar to Ukraine ($160 billion).

In January 2022, Kazakhstan asked for Russian help to quell protests and riots (227 died in a week of unrest) over the rising cost of fuel. Russia acquiesced with a military presence.

There are Caspian pipelines involved and Kazakhstan produces 40% of the world’s uranium.

In January 1991, I was in Seattle, when we were taking batting practice in the cages, just when our head baseball coach came barreling around the corner in his Ford Bronco. He jumped out of the car and said; “Holy Shit”, we’re bombing Baghdad”.

He declared practice over and sent everyone home.

Being Australian, I wasn’t too perturbed and asked another coach if he could stay back with me to throw me some extra balls to hit.

90 minutes later, I arrive back at my apartment to find my room (and team) mates on their way to drunkenness as they watched the bombardment on CNN.

They were already talking about moving to Canada as rumours of reinstating compulsory military service were spreading.

Today’s media noise about Russia, Ukraine, NATO, the U.N. and the United States sounds just like the ‘noise’ I was hearing when Iraq was invading Kuwait and then the U.S. (and coalition) started their bombing campaign.

Wikipedia says, “The Gulf War was a war waged by coalition forces from 35 nations led by the United States against Iraq in response to Iraq’s invasion and annexation of Kuwait arising from oil pricing and production disputes.”

Incidentally, it was also believed that the coalition forces also commenced the bombings in order to protect Saudi Arabia.

That extensive aerial bombing campaign lasted from 17 January 1991 to 23 February 1991.

Ironically, on the day the campaign began, WTI Crude Oil rose 6.4%.

Over the next 32 days, the price of Oil then fell 44%.

(funnily shares in companies such as Exxon and Occidental rose 10% through this time)

The U.S. 10 year bond yield fell from 8.2% to 7.7%

and the S&P 500 rose 20%

It’s not exactly the same, but it kind of ‘rhymes’.

What is telling at this moment, is that it doesn’t seem that the U.S., NATO or any coalition is about to fly in and defend Ukraine let alone bomb Moscow or St. Petersburg.

It’s more telling that they are using stern words of “condemnation’ and rolling waves of sanctions instead.

With that, Zelensky may tip his King (chess piece) over because there isn’t a larger army coming up behind him.

For the statistic fans, Moscow and St. Petersburg are Europe’s 2nd and 4th most populous cities.

Istanbul is 1st, London 3rd, Berlin is 5th, Madrid 6th and Kyiv and Rome shares 7th and 8th place.