The following assets (on a weekly timeframe) registered an Overbought reading or traded more than 2.5 standard deviations above its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations)

China Coal

Gasoil

Heating Oil

Japanese Korean (JKM) LNG Marker

Tin

Nymex LNG

Platinum

Palladium

Dutch TTF Gas

Uranium

Rice

AUD/GBP

Overbought (RSI > 70)

Australian 2, 5 & 10 year government bond yields

U.S. 2 & 5 year government bond yields

Greek, Spanish, Turkish & New Zealand 10 year government bond yields

Soybeans

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Australian 3 year government bond yields

U.S. Dollar (DXY) Index

Bloomberg Commodity Index

CRB Index

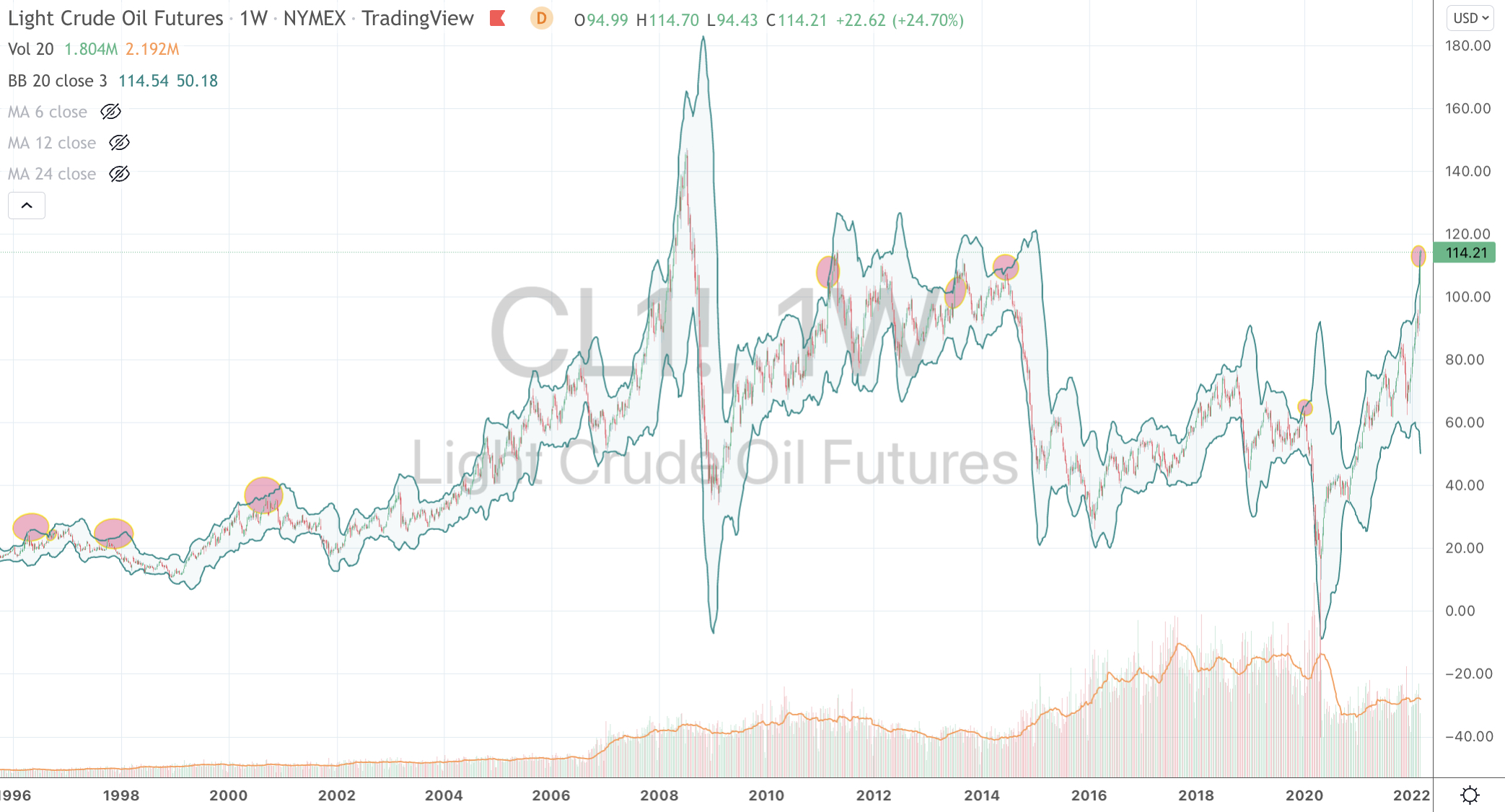

WTI Crude Oil

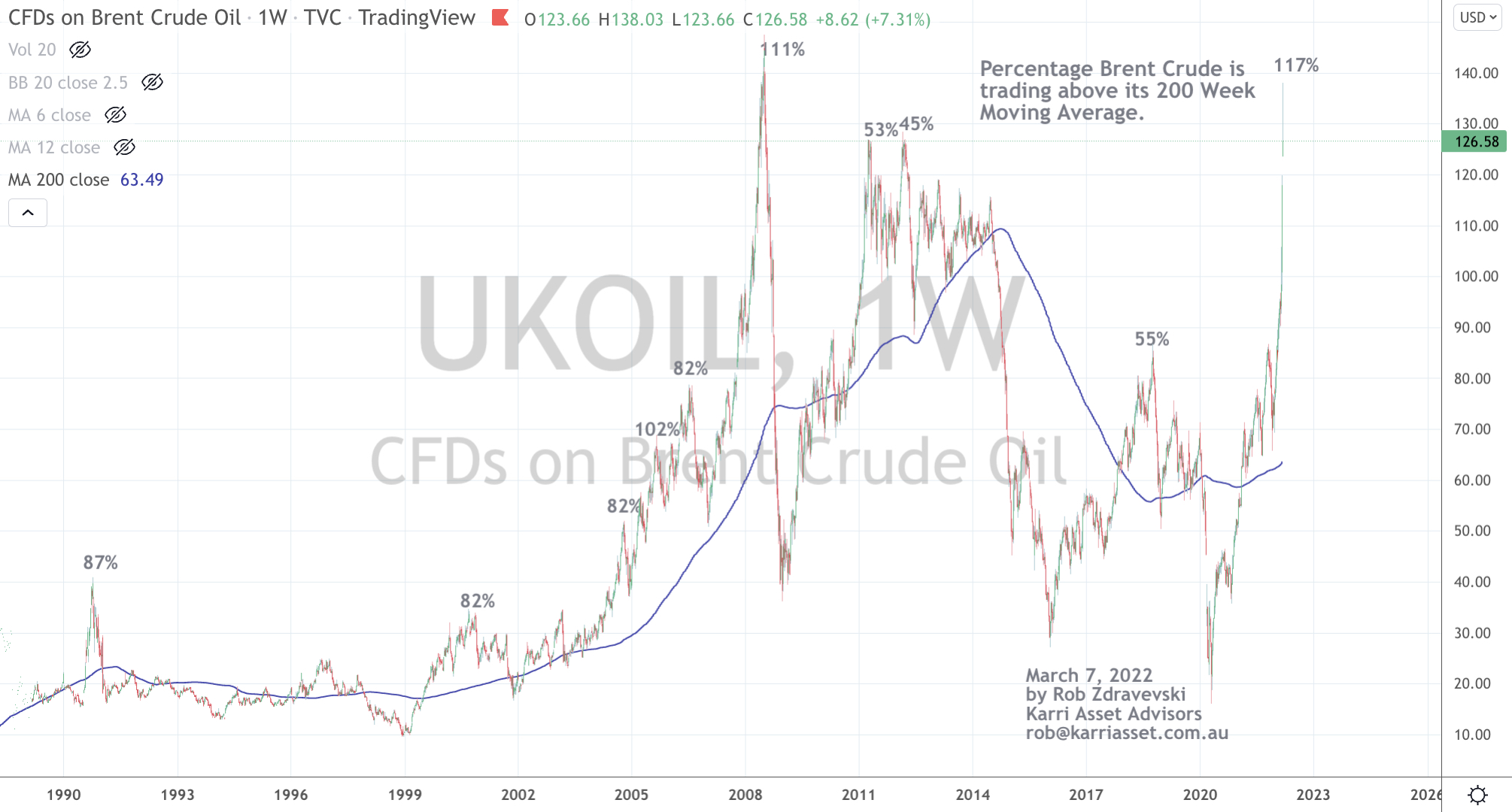

Brent Crude Oil

Gasoline

Rotterdam Coal

Australian Coal

Nickel

Corn

Wheat

Gold Volatility Index

Gold (in AUD & USD)

Assets (securities) which touched the other side of the extreme, being Oversold (where the RSI is < 30) or were at least 2.5 standard deviations below its mean are;

Extremes “below” the Mean (at least 2.5 standard deviations)

U.S. 10 year minus Australian 10 year government yield spread

Copper/Gold Ratio

Oil/Gold Ratio

EUR/AUD

EUR/GBP

EUR/USD

DKK/USD

JPY/USD

Dow Jones Industrial Average

S&P 500

U.S. (KBW) Banking Index

Sensex, IBEX, Nikkei 225, DAX, FTSE-100 and Italy’s MIB equity indices

Oversold (RSI < 30)

U.S. 10 year minus 2 year government bond yield spread

(Now at the same level as March 9th, 2020)

The Oversold Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

KRW/USD

SEK/USD

HKD/USD

AEX, CSI 300, HSCEI, Hang Seng, Helsinki, Stockholm & Switzerland’s SMI equity indices

Notes & Ideas:

Broadly, we have seen an opposite of the previous week. It was a resumption of weakness for American indices and a rebound in Europe. For some context, a 4% bounce in an Oversold DAX merely recovers part of the previous week’s 10% decline and Helsinki’s 7% rise recouped part of last week’s 1% slump.

But we did see reasonable declines amongst Asian bourses.

Last week, I wrote that it “was a week for the record books”.

Alas, that has all been trumped by even higher intra-week highs, some resembling ‘blow-off tops”and then followed by wicked retracements and reversals.

For example, Gasoil (diesel) was up 40% at one stage to end up closing the week 14.6% lower. JKM was up 34%, Palladium surged 39% and then registered a 6% decline on the week, Nickel soared 152% and saw a 13 standard deviation weekly move while Copper traded 4 standard deviations above its mean.

If you didn’t look at the numbers, you’d think Oil was up on the week while mild mannered Cocoa was steady and unchanged.

Incidentally, it’s OK that Wheat fell 8% for the week because it rose 40% last week.

In other reversal news, bond yields rose, meaning prices fell suggesting geopolitical risk was waning.

While it remains a sellers market in commodities, it is a buyers market in selected equities.

As I’ve written in recent newsletters, I am finding the most amount of investible opportunities than I’ve seen in the past 15 months.

The larger advancers over the past week comprised of;

Baltic Dry Index 26.5% (which is + 76% in 6 weeks), Aust. Coal 9.8%, Gold 1%, Hogs 2.3%, Nickel 25.4%, Silver 1.4%, Cotton 4%, Urea 4.2%, Uranium 16.5%, Gold (in AUD) 2.1%, Corn 1.1%, CAC 3.3%, DAX 4.1%, MIB 2.6%, IBEX 5.5%, Sensex 2.4%, Helsinki 6.6%, Stockholm 4.3%, SMI 1.7%, FSTE 2.4% and Istanbul rose 4%.

The group of decliners included;

Aluminium (11%), Rotterdam Coal (15.9%), China Coal (11%), WTI Crude (5.5%), Gasoil (14.6%), Copper (6.3%), Heating Oil (9.5%), HRC (4.3%), JKM (3.9%), Lumber (11.6%), Nymex LNG (33.3%), Tin (5%), Natural Gas (5.8%), Orange Juice (6.2%), Palladium (6.2%), Gasoline (6.5%), Brent Crude (4.8%), Rice (3.6%), Wheat (8.5%), Shanghai (4%), KBW (2.3%), CSI 300 (4.2%), DJIA (2%), HSCEI (8.2%), HSI (6.2%), IBOV (2.4%), Kospi (2%), S&P Midcap 400 (1.7%), Nasdaq (3.9%), Nikkei (3.2%), SMI (3.5%), S&P 500 (2.9%), TAIEX (2.7%), DJ Transports (3.8%) and Australia’s ASX 200 only declined 0.7%, erasing part of last weeks 1.6% advance.

March 13, 2022

by Rob Zdravevski

rob@karriasset.com.au