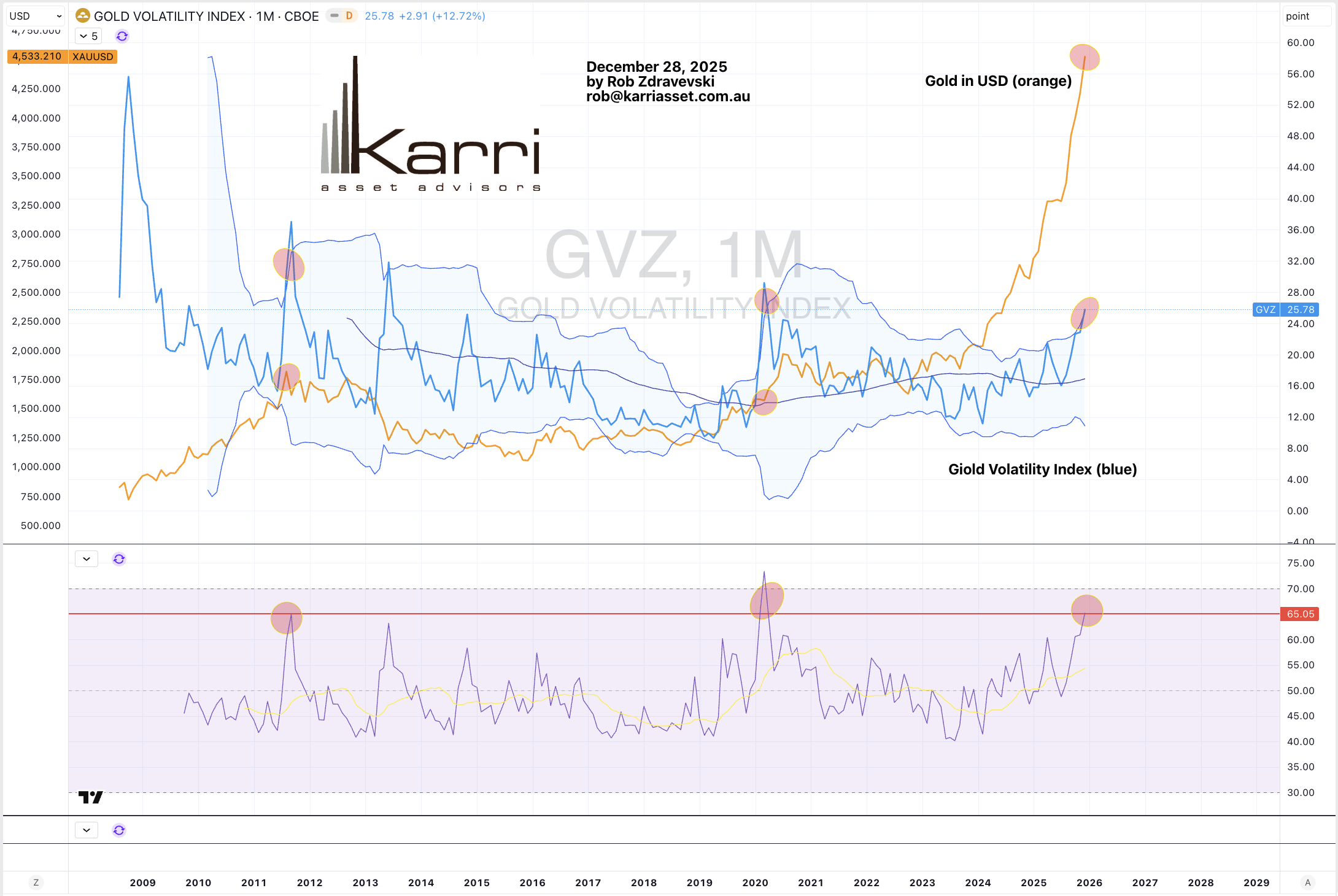

A relationship with Gold

December 28, 2025 Leave a comment

The attached study depicts the relationship between the price of Gold and the Gold Volatility Index

Trying to hear what's not being said

December 28, 2025 Leave a comment

The attached study depicts the relationship between the price of Gold and the Gold Volatility Index

December 21, 2025 Leave a comment

A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) either registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

n.b. pricing of (commodity) futures contracts is only considering the immediate front month.

* denotes multiple week inclusion

Extremes above the Mean (at least 2.5 standard deviations)

Chilean 10 year minus 2 year bond yield spread

European 5 and 10 year bond yields

U.S. 5 year bond yield minus U.S. 5 year inflation breakeven spread

U.S. 10 year minus U.S. 2 year bond yield spread

Australian Coking Coal

ZAR/USD

Italy’s MIB Index

Malaysia’s KLSE Index

Nasdaq Transports *

Overbought (RSI > 70)

Australian 10 year minus U.S. 10 year bond yield spread *

Japanese 2, 5 and 30 year bond yields

Aluminium (LME price)

Palladium

Silver in AUD & USD

Gold in AUD, CAD, CHF, EUR, GBP & USD *

AUD/JPY *

CAD/JPY *

CHF/JPY *

CNH/USD *

EUR/JPY *

MYR/USD *

Hungary’s BUX Index *

Egypt’s EGX Index *

IBB biotech ETF *

Spain’s IBEX *

Nasdaq Biotech Index *

OMX Helsinki Index

South Africa’s SA40 equity index *

Chile’s IGPA *

Israel’s TA35 *

Canada’s TSX equity index *

FTSE 100 Index

And the S&P Biotech ETF *

The Overbought Quinella (Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Danish 10 year government bond yield

Euro 20 and 30 year bond yields

Japanese 10 year government bond yields *

Tin

Platinum

GBP/JPY *

Austria’s ATX equity index *

U.S. KBW Bank Index *

Czechia’s PX Index *

Extremes below the Mean (at least 2.5 standard deviations)

Brent Crude Oil

JKM LNG in Yen

Wheat

AUD/THB

BRL/USD

Oversold (RSI < 30)

U.S. 10 year minus the Australian 10 year bond yield spread *

U.S. 10 year minus the European 10 year bond yield spread *

U.S. 10 year bond yield divided by Australian 10 year yield spread

Richards Bay Coal *

Lumber *

Sugar #16 *

Rice *

JPY/USD

The Oversold Quinella (Both Oversold and Traded at < 2.5 standard deviations below the weekly mean)

None

Notes & Ideas:

Government bond yields rose, again, again.

The Australian yield curve has climbed for 4 weeks.

Japanese 2 and 5 year bond yields have risen for 5 weeks straight.

Kiwi 10 year yields fell and broke 8 weeks of advance.

The U.S. 10 year minus Australian 10 year bond yield spread has fallen for 8 weeks.

And Chilean 2 year bond yields have fallen for 4 weeks.

Equities were mixed.

Many indices appearing in last week’s overbought list, are no longer so.

The All World Developed Index, Austria’s ATX, Dow Jones Transports, Italy’s MIB, Spain’s IBEX, Norway’s OBX, Czechia’s PX, South Africa’s SA40, Israel’s TA-35, and the ASX Financials are in 4 week winning streaks.

U.S. Regional Bank Index has risen for 5 weeks.

Pakistan’s KSE has climbed for 6 consecutive weeks.

The Nasdaq Transportation Index fell and broke its 4 week winning streak.

Chile’s IGPA fell and broke a 9 week winning streak.

Commodities were mixed, again.

Orange Juice, Silver, Platinum, Palladium, Uranium, Nickel and Lithium were the notable gainers.

Shipping Rates, Coffee, Gases, Distillates, Soybeans and Cocoa dominated the losers category.

Platinum has soared 30% in the past week.

Orange Juice has climbed 33% in the past fortnight.

Heating Oil has fallen 10% over the last 2 weeks,

While the Baltic Dry Index has given up 27% over the same time.

Lithium Hydroxide is no longer oversold.

Cattle, Tin and Silver (in USD) have risen for 4 weeks.

While Silver as priced in AUD is in a 7 week winning streak.

Newcastle Coal, Gasoil and Rice has fallen for 5 straight weeks.

Wheat is in a 7 week slump.

Currencies were active.

The Yen’s weakness continues and is seen in various pairs such as against the CAD & GBP across a 6 week losing streak.

The Aussie mostly fell and as a result, all of last weeks overbought readings are no longer so.

AUD/JPY and MYR/USD have risen for 4 consecutive weeks.

CAD/JPY has climbed for 6 weeks.

The British Pound was higher.

The USD firmed enough to move certain pairs out of oversold territory.

And the USD/Chinese Yuan is oversold.

The larger advancers over the past week comprised of;

Australian Coking Coal 2.4%, Aluminium 3%, Copper 2.8%, Lithium Carbonate 7.4%, Lithium Hydroxide 4.1%, Tin 2.7%, Nickel 3.8%, Orange Juice 21.4%, Palladium 15.8%, Platinum 14.5%, Dutch TTF Gas 1.7%, Urea U.S. Gulf prices 1.6%, Uranium 3.8%, Silver in AUD 9.2%, Oats 4.2%, Gold in AUD 1.6%, ATX 2.6%, MIB 2.9%, IBEX 1.9%, KLSE 1.7%, FTSE 250 2%, PX 3.3%, SMI 2.2%, FTSE 100 2.6% and Vietnam rose 3.5%.

The group of largest decliners from the week included;

Baltic Dry Index (8.3%), Cocoa (6.9%), WTI Crude Oil (1.4%), Palm Oil (2.9%), Heating Oil (3.3%), JKM LNG (1.7%), Arabica Coffee (7.8%), Natural Gas (3.1%), Gasoline (2.4%), Robusta Coffee (8.4%), Sugar (1.4%), Gasoil (3.5%), Soybeans (2.4%), EGX (2.6%), FCATC (2.3%), HSCEI (2%), S&P SmallCap 600 (1.4%), TAIEX (1.8%), KOSPI (3.5%), Nikkei 225 (2.6%), PSE (1.9%) and the ASX Material Index fell 1.8%.

December 21, 2025

By Rob Zdravevski

December 20, 2025 Leave a comment

📈 Calendar year-to-date (1 Jan–20 Dec 2025):

• S&P 500: +16.2% (USD, ex-dividends)

• S&P 500: +9.3% (AUD)

• ASX 200: +5.7% (AUD)

📆 Australian financial year to date (since 1 July 2025):

• S&P 500: +8.8% (AUD)

• ASX 200 (price): +0.9%

Across either timeframe, clients should be pleased with the outperformance delivered at the portfolio level, particularly given the broader market backdrop.

November is a good example.

While major indices were broadly flat, most client portfolios rose ~2%. At the same time, several widely followed “super-star” hedge funds reportedly fell ~2%.

Relative outcomes matter — especially when markets aren’t doing much.

A few broader points worth noting:

1) Currency matters — a lot.

The currency you invest in, measure in, or convert back to can materially change outcomes. I expect far more action in currency markets over the coming years, and currency selection will remain a deliberate part of my global strategy.

2) The herd delivers herd results.

Moving with the crowd usually produces the same outcome as the crowd.

Diversification helps you lose less than someone else — it is not designed to produce above-average returns.

3) A different kind of bubble is forming.

Not in prices — but in expectations.

When a potential 20% return is met with, “Is that all?”, it’s worth remembering that the ASX 200 has risen only ~5% over the past 12 months.

Perspective still matters.

December 20, 2025

rob@karriasset.com.au

December 18, 2025 Leave a comment

It has been some time since my July 17, 2025 newsletter.

I haven’t had anything new to say.

In that edition, along with the June and April 2025 versions, my main message was;

“I don’t (didn’t) see any structural problems in the global equity market”.

Those newsletters contained a host of analysis illustrating that the currency and bond markets told me that the “prospects for equities is OK” and we were not experiencing any peaks nor bubbles.

Since and during, I have been accumulating various equities and building portfolios for clients with the focus on “making money in any type of market conditions”.

I also wrote about the opportunities observed in the healthcare and transport industries, along with Chinese equities and commodities such as Palladium.

They have all performed well.

The latter has soared 70% since it was mentioned in my June 20, 2025 newsletter which is notably more than the 27% rise seen in the Gold price, over the same time.

And the markets have been very kind.

You may want to read the April 1, 2025 and April 10, 2025 newsletters where I was stating the case for “buying” rather than running and selling.

Since my April 10, 2025 newsletter, the MSCI All Country World Index (ACWI) and the S&P 500 have risen 23%, while the ASX 200 climbed 16%. Those returns should temper and place the giddiness of Gold’s advance within perspective.

While the price of various (and many other) stocks have doubled or more.

Those returns were achieved amidst the cited ‘noise’ and ‘concern’.

That’s why its important to ignore the noise or narrative and rely on the data, mathematics and signals.

This reminder remains intact.

Between April 2025 and now, I have taken profits in selected stocks and started positioning portfolios is a new series of stocks which seem to be unwanted and trading at much cheaper valuations than I’ve seen at any time over the past few years.

Furthermore, there are so many high-quality companies which are attractively priced that investors don’t need to trawl through the gutters of speculation.

My current areas of interest include a range of companies in software, online marketplaces, data and verification providers, brand name chemical companies, cloud accounting and some selected biotech’s.

Coming soon, I anticipate including energy and building materials companies to that list.

And I still don’t see any structural problems in the global equity markets.

Thank you for being a reader of my various opinions and views and I hope you find a nugget of value within them.

Also, thanks to those who forward to and share my newsletter with others.

Season’s Greetings to all and wishing you a prosperous and healthy 2026.

Until next time,

Rob Zdravevski

rob@karriasset.com.au

.

In between newsletters, you can read my varied commentary across a range of markets and asset classes on my blog or Linkedin page.

Feel free to pass this onto your friends and professional associates. They are also welcome to contact me on +61 438 921 403 or send an email to rob@karriasset.com.au

“I think diversification and all the stuff they’re teaching at business school today is probably the most misguided concept everywhere” – Stanley Druckenmiller

“If you can’t accept volatility in the value of your assets, allow me to introduce you to a bank term deposit” – Me

December 18, 2025 Leave a comment

Q: What was the reason ‘you’ bought Oracle stock at $320 in September 2025?

A: Because that was the day when ORCL reported its Q1 earnings and announced a massive contract with OpenAI.

Today, the stock price is $178.46 and within 4 months, those buyers have nearly halved their money.

The circles in the study below tell you have you have no ’empirical’ reason to have been a buyer of Oracle shares.

For the disciplined, you may get to buy it at $138 (for a trade) or the bargain hunters may wait for their pitch in the $105 – $98 zone.

December 18, 2025

rob@karriasset.com.au

December 17, 2025 Leave a comment

Here is a look at the correlation between Bitcoin and Equities (S&P 500)

December 14, 2025 Leave a comment

A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) either registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

n.b. pricing of (commodity) futures contracts is only considering the immediate front month.

* denotes multiple week inclusion

Extremes above the Mean (at least 2.5 standard deviations)

Austrian, Australian, Danish, Spanish, Greece, Indian, Dutch, Norwegian and Swedish 10 year bond yields

U.S. 5 year bond yield minus U.S. 3 month bill yield spread

U.S. 10 year minus U.S. 2 year bond yield spread

Australian Coking Coal

AUD/CHF *

AUD/EUR *

AUD/USD

CLP/USD *

THB/USD

Austria’s ATX equity index *

Dow Jones Transports *

S&P MidCap 400

Copenhagen’s OMX

Nasdaq Transports *

Overbought (RSI > 70)

Australian 10 year minus U.S. 10 year bond yield spread *

The Euro bond yield curve

Korean 10 year government bond yield *

Silver in AUD

Gold in AUD, CAD, CHF, EUR, GBP & USD

AUD/JPY *

CAD/JPY

CHF/JPY

CNH/USD *

EUR/JPY *

GBP/JPY *

Hungary’s BUX Index *

Indonesia’s IDX Composite *

Egypt’s EGX Index *

IBB biotech ETF *

Spain’s IBEX

Brazil’s BOVESPA

Taiwan’s TAEIX

Pakistan’s KSE Index *

South Korea’s KOSPI *

Nasdaq Biotech Index *

Czechia’s PX Index *

South Africa’s SA40 equity index *

Chile’s IGPA *

Singapore’s Strait Times Index

Israel’s TA35 *

Canada’s TSX equity index *

The S&P Biotech ETF *

And Australia’s ASX Materials Index

The Overbought Quinella (Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Australian 2, 3 and 5 year government bond yields

Euro 20 and 30 year bond yields

Japanese 2, 5 and 10 year government bond yields *

Tin

Silver in USD *

AUD/INR *

MYR/USD*

USD/INR *

U.S. KBW Bank Index

Extremes below the Mean (at least 2.5 standard deviations)

Belgian and Finnish 10 year government bond yields

Lithium Hydroxide *

Dutch TTF Gas *

CHF/AUD *

USD/MXN

USD/SEK

Oversold (RSI < 30)

Chilean 10 year government bond yield *

U.S. 10 year minus the Australian 10 year bond yield spread *

U.S. 10 year bond yield divided by Australian 10 year yield spread

Richards Bay Coal *

Lumber *

Sugar #16 *

Urea (U.S. gulf)

Rice *

The Oversold Quinella (Both Oversold and Traded at < 2.5 standard deviations below the weekly mean)

None

Notes & Ideas:

Government bond yields rose, again.

Except for short dated U.S. paper and the British yield curve.

Swiss 10’s soared.

A bunch of new bond yields appear in this weeks list.

The Australian, Euro and Japanese yield curves are overbought.

Kiwi 10 year yields have climbed for 8 weeks,

Whilst Japanese 10 year yield fell slightly, which ends its 7 week rising streak.

Turkish 10 year yields have fallen for 4 weeks, as have U.S. 3 month bills.

And the U.S. 2 year bond is yielding less than the U.S. 3 month bill.

Equities had a slightly higher bias.

More indices joined the overbought extreme list.

While most indices closed either +/- 1% from last week but intra-week there were gyrations.

Brazil’s Bovespa returns overbought territory.

U.S. Regional Bank Index and the Nasdaq Transportation Index have risen for 4 weeks.

Vietnam, the Sensex and XBI biotech ETF fell and broke their 4 weeks of advance.

Chile’s IGPA is in a 9 week winning streak.

Commodities were mixed, again.

Cocoa, Orange Juice, Platinum, Silver and Tin were the notable gainers.

Shipping Rates, Oil, Gases and Distillates, Oats and Palm Oil dominated the losers category.

Natural Gas tanked 22% and erased half of the 39% gain seen in the previous 7 week winning streak.

The Baltic Dry Index also fell hard, wiping 19% of the 34% seen in the 5 week winning streak.

U.S. Gulf Urea prices rose and snapped 5 weeks of decline.

Rice is in a 4 week losing streak.

Wheat has slumped for 6 weeks.

And the Copper/Gold Ratio looks like it’s about to change direction in trend.

Currencies were active.

The Yen’s weakness sees various pairs such as against the CAD & GBP is a 5 week losing streak.

The Aussie fell except against the INR, JPY and USD.

Against the Yen, the Aussie is overbought for the first time since July 2024.

The Loonie was firmer.

The Swissie rose.

Euro as stronger, reversing last weeks weakness.

And the USD/Chinese Yuan is oversold.

The larger advancers over the past week comprised of;

Cocoa 10.2%, Lean Hogs 3.6%, Lumber 3.4%, Lithium Carbonate 1.9%, Tin 3.4%, Orange Juice 12%, Palladium 2.7%, Platinum 6.1%, Sugar 2%, Uranium 2.6%, Silver in AUD 5.9%, Silver in USD 6.1%, Gold rose between 1.5% – 2.4% across various currencies, All Word Developed ex USA 1%, KBW Banks 3.6%, DJ Transports 1.9%, BOVESPA 2.2%, S&P Small Cap 600 2.1%, Russell 2000 1.2%, KRE Regional Banks 1.7%, KOSPI 1.6%, Copenhagen 2.3%, PSE 1.5%, PX 1.7%, S&P 600 2%, TA35 3.6%, Nasdaq Transports 2.3%, WIG 3.5%, ASX Financials 1.7%, ASX Materials 2.8% and Türkiye’s BIST rose 2.8%.

The group of largest decliners from the week included;

Aluminium (1.7%), Bloomberg Commodity Index (2.7%), Brent Crude (4.1%), Baltic Dry Index (19.1%), WTI Crude Oil (4.4%), Palm Oil (3.2%), Copper (1.9%), Heating Oil (7%), JKM LNG (1.7%), JKM LNG in Yen (3.8%), Newcastle Coal (2.4%), Natural Gas (22.2%), Nickel (2.5%), Gasoline (4.5%), Robusta (4%), S&P GSCI (3.4%), CRB Index (2.5%), Gasoil (6.9%), Oats (7.3%), Soybeans (2.6%), HSCEI (1.3%), Nasdaq Composite (1.6%), Nasdaq 100 (1.9%), SET (1.5%), SOX (3.6%), S&P 500 (0.6%) and Vietnam fell 5.4%.

December 14, 2025

By Rob Zdravevski

December 10, 2025 Leave a comment

In September 2012 I wrote this note calling for lower Oil prices by 2020….

And here the Oil chart circling prices in 2012 and 2020….

Today, we have similar news and tensions…..involving America’s thirst for Oil, how the Saudi’s want to control the price, Venezuela’s reserves and China and India’s willingness to buy it.

It’s not about cocaine smugglers on small boats !

December 10, 2025

rob@karriasset.com.au

December 7, 2025 Leave a comment

A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) either registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

n.b. pricing of (commodity) futures contracts is only considering the immediate front month.

* denotes multiple week inclusion

Extremes above the Mean (at least 2.5 standard deviations)

Australian government bond yield curve *

Norwegian 10 year bond yields

Euro 2, 5 and 30 year bond yields

AUD/CHF

AUD/EUR

AUD/INR

CLP/USD *

Austria’s ATX equity index *

Dow Jones Transports

Nasdaq Transports

Overbought (RSI > 70)

Korean 10 year government bond yield *

Silver

Gold in CAD, CHF, EUR, GBP & USD

AUD/JPY

CNH/USD

EUR/JPY *

GBP/JPY

Hungary’s BUX Index *

Indonesia’s IDX Composite

Egypt’s EGX Index *

IBB biotech ETF *

Pakistan’s KSE Index *

South Korea’s KOSPI *

Nasdaq Biotech Index *

Czechia’s PX Index *

South Africa’s SA40 equity index *

Chile’s IGPA *

Israel’s TA35 *

Canada’s TSX equity index *

And the S&P Biotech ETF *

The Overbought Quinella (Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Australian 10 year minus U.S. 10 year bond yield spread *

The Japanese government bond yield curve *

Swedish 10 year government bond yields

Baltic Dry Index *

Tin

MYR/USD*

USD/INR

Extremes below the Mean (at least 2.5 standard deviations)

Brazilian 10 year government bond yield

CHF/AUD

Oversold (RSI < 30)

Chilean 10 year government bonds

U.S. 10 year bond yield divided by Australian 10 year yield spread

Richards Bay Coal *

Lumber *

Lithium Hydroxide

Sugar #16 *

Rice *

JPY/AUD

NZD/AUD

The Oversold Quinella (Both Oversold and Traded at < 2.5 standard deviations below the weekly mean)

U.S. 10 year bond yield minus Aussie 10 year bond yield spread *

Dutch TTF Gas *

Notes & Ideas:

Government bond yields rose, again.

Canadian 10’s soared.

The whole of the Australian and Japanese yield curve is overbought and the Eurozone is nearly so.

Kiwi and Japanese 10 year yields have climbed for 7 weeks,

U.S. 10 year minus Australian 10 year yield spread has fallen for 6 weeks.

Equities moved higher, again.

Biotech’s added to its recent run higher.

Brazil’s Bovespa left overbought territory.

Vietnam, the Sensex and XBI biotech ETF have risen for 4 weeks.

Chile’s IGPA and IPSA indices are in a 8 week winning streak.

Commodities were mixed.

Shipping Rates, Silver Cocoa, Tin, Cattle and Natural Gas were the notable gainers.

Lithium, Orange Juice, Dutch TTF Gas, Sugar, Soybeans and Coffee dominated the losers category.

Soybeans fell and broke a 7 week winning streak.

Natural Gas have risen for 7 weeks and has soared 39% over that time.

Cattle & Palm Oil rose enough to leave their oversold extremes.

Richards Bay Coal is close to doing the same.

The Baltic Dry Index and Iron Ore prices have risen for 5 weeks.

The former has soared 34%in those 5 weeks.

North European Hot Rolled Coil Steel have declined for 4 weeks.

And Wheat and U.S. Gulf Urea prices have slumped for 5 weeks.

Currencies were orderly.

The Yen’s weakness sees various pairs such as against the CAD & GBP is a 4 week losing streak.

The Aussie rose, resulting in a few overbought results.

Against the Yen, the Aussie is overbought for the first time since July 2024.

The Euro was mostly weaker.

And the USD/Chinese Yuan is oversold.

The larger advancers over the past week comprised of;

Australian Coking Coal 3.8%, Aluminium 2.3%, Bloomberg Commodity Index 1.5%, Brent Crude Oil 2.2%, Baltic Dry Index 6.5%, Cocoa 3.5%, WTI Crude Oil 2.6%, Copper 3.6%, Heating Oil 2.6%, Cattle 4.3%, Tin 6%, Natural Gas 9%, SOGSCI 1.7%, Silver in USD 3.5%, Silver in AUD 2.1%, ATX 1.4%, BKX 3.2%, DJ Transports 3.6%, EGX 3.7%, IBEX 1.9%, KRE Regional Banks 2.8%, KOSPI 4.4%, Helsinki 1.7%, Stockholm 1.4%, SA40 1.5%, SOX 3.8%, TA35 3.4%, Nasdaq Transports 4.7%, Vietnam 3% and ASX Materials Index rose 3%.

The group of largest decliners from the week included;

JKM (1.9%), Arabica Coffee (1.7%), LNG in Yen (5.8%),Lithium Carbonate (4.4%), Lithium Hydroxide (5%), Newcastle Coal (1.4%), Orange Juice (6.6%), Platinum (1.5%), Robusta Coffee (5.9%), Sugar (2.7%), Sugar #16 (1.7%), Dutch TTF Gas (5.4%), Urea U.S. Gulf (4.3%), Gold in AUD (1.9%), Gold in CAD (1.7%), Gold in ZAR (1.6%), Oats (2.8%), Soybeans (2.9%), IBB (1.5%), WIG (1.7%) and ASX Industrials Index fell 1.6%.

December 7, 2025

By Rob Zdravevski

December 5, 2025 Leave a comment

Who on earth is going ‘long’ Silver during such parabolic moves?

Gravity (mean reversion) is a bitch.

December 5, 2025

rob@karriasset.com.au