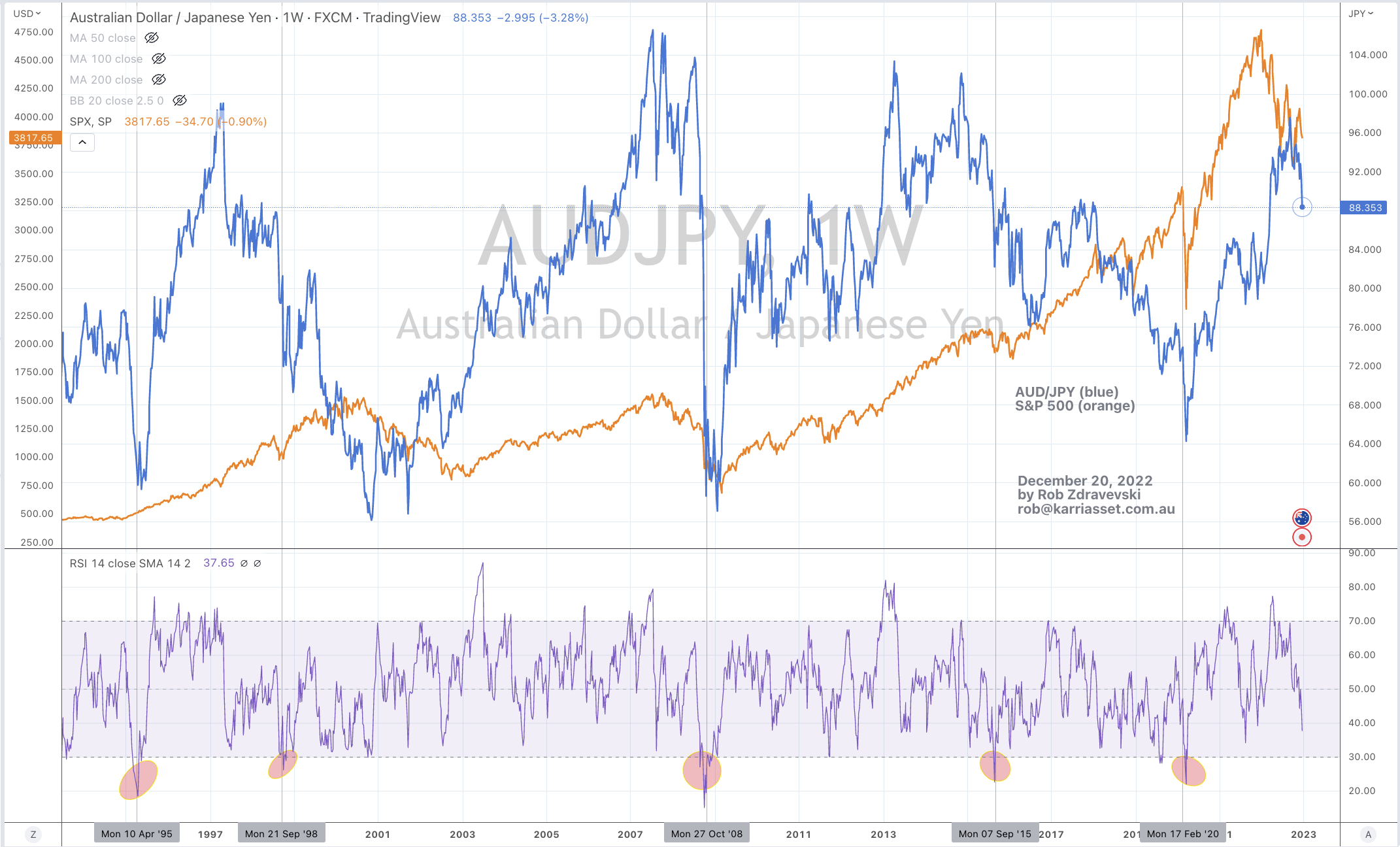

A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities

The following assets (on a weekly timeframe) registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations)

Chinese 10 year government bond yields

Silver

Sugar

Overbought (RSI > 70)

German 2 year government bond yields

Cattle

Istanbul’s BIST Index

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

None

Extremes “below” the Mean (at least 2.5 standard deviations)

U.S. 10 yer bond yield minus German 10 year bond yield spread

Brent Crude Oil

BOVESPA

Oversold (RSI < 30)

Hot Rolled Coil Steel (HRC)

U.S. 5 year yield minus U.S. 3 month bill yield spread

Chilean 10 year bond yield

The Oversold Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

None

Notes & Ideas:

The big news for the week was that Brent Crude Oil touched the lower of its standard deviations extreme.

After being bearish for 12 months, Oil is nearing a Buy signal.

Otherwise, we saw European government bond yields rise (ECB President Lagarde scared them with rhetoric), while U.S. bond yields fell.

Moreover, the U.S. series of bond yields started making newer, recent lows and I found it interesting to see the U.S. 10 year breakeven inflation rate fall to 2.13%, which is its lowest since January 2021. This is down from its 3% April 2022 reading,

Meanwhile the Korean 10’s are marching closer towards a long term mean reversion as is the price of Gasoline.

The Baltic Dry Index has risen 28% over the past month,

The Nordic bourses joined the weakness seen in U.S. equities,

Palladium hit a new 52 week low,

I’m watching the Bovespa and the weaker Real,

the Dow Jones Transport only fell 0.2% for the week,

equally small cap indices aren’t over exaggerating declines in the large caps,

Hot Rolled Coil Steel remains Oversold for the 25th consecutive week,

Lastly, Nickel isn’t overbought anymore.

The larger advancers over the past week comprised of;

Baltic Dry Index 12.6%, JKM LNG 6.6%, China Coal 2.8%, WTI Crude 4.8%, Gasoil 8.7%, Lean Hogs 5.2%, Heating Oil 11.7%, Coffee 4%, Natural Gas 5.7%, Sugar 2.5%, CRB Index 1.9%, Brent Crude 3.3%, Rice 1.9%, Wheat 2.6%, Istanbul 2.5% and the S&P GSCI Index rose 2.8%.

The group of decliners included;

Aluminium (3.1%), Rotterdam Coal (10.2%), Iron Ore (1.8%), Copper (3%), Lumber (6.3%), Nickel (7.6%), Orange Juice (2.3%), Palladium (13.3%), Platinum (3.5%), Dutch TTF Gas (17%), Urea U.S. Gulf (2.6%), Uranium (4.8%), AEX (3.3%), KBW Banking Index (2.8%), CAC (3.4%), DAX (3.3%), DJ Industrials (1.9%), MIB (2.4%), HSCEI (2.9%), HSI (2.2%), IBEX (2.1%), BOVESPA (4.3%), Nasdaq Composite (2.7%), S&P MidCap 400 (2.4%), Nasdaq 100 (2.8%), Stockholm (3.3%), Helsinki (3.9%), Copenhagen (2.6%), Russell 2000 (2.3%), S&P SmallCap 600 (2.7%), SMI (2.7%), SOX (3.1%), S&P 500 (2.1%), TSX (2.5%), FTSE 100 (1.9%), and Australia’s ASX 200 and ASX Small Ordinaries both declined 0.9% for the week.

December 18, 2022

by Rob Zdravevski

rob@karriasset.com.au