The AUD Gold price is seemingly full

January 9, 2023 1 Comment

Listed Australian gold equities have had a stellar run, especially in the past month or so.

However, I have been a seller and not initiating any new buys.

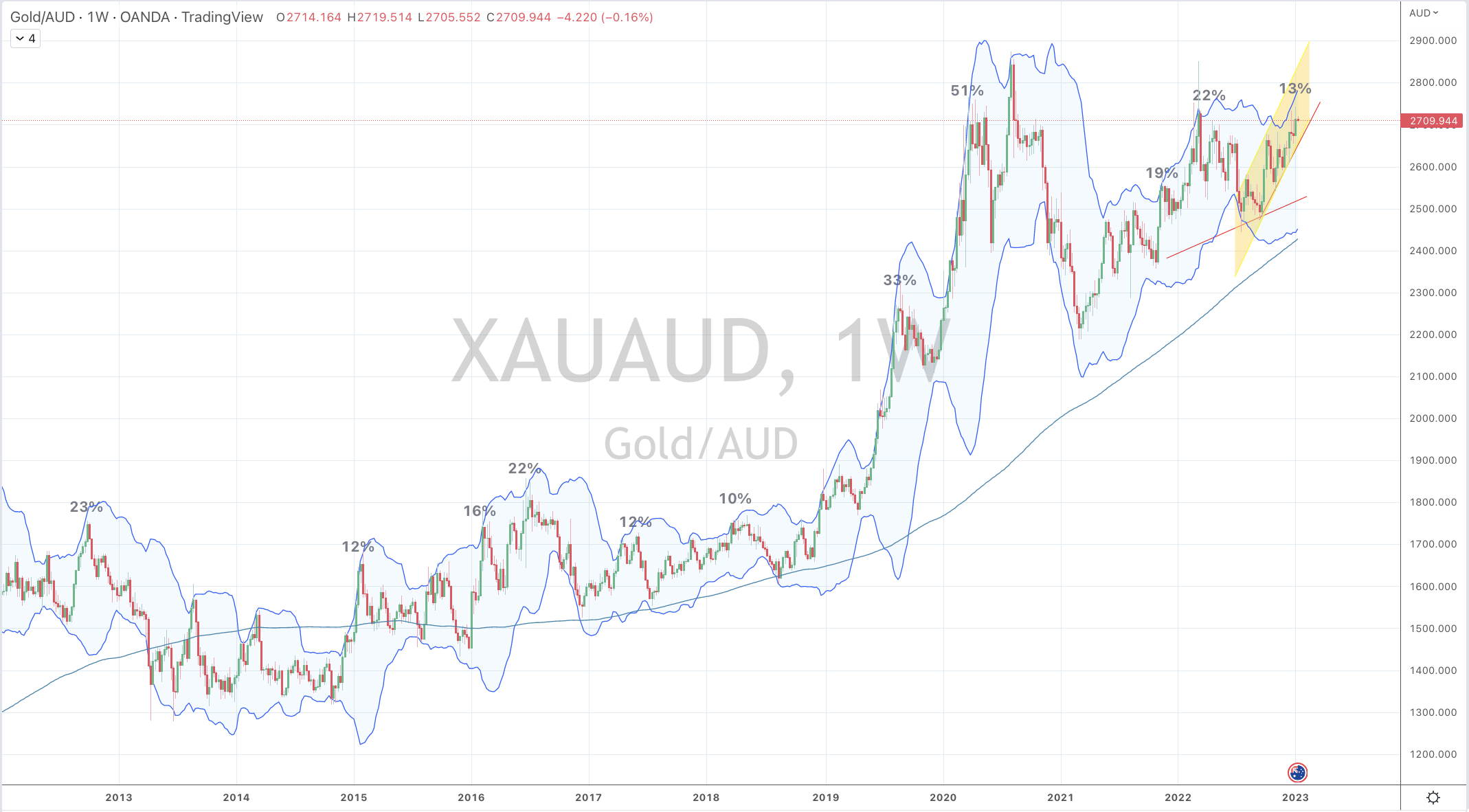

Albeit the Australian Dollar (AUD) Gold price has been acting well as it has been making higher lows and higher highs, some context is required.

Since December 1, 2022, the AUD Gold price has only risen 2.4%, (as the shorter time frame chart illustrates below) while some gold related equities have risen 15%-20% over the same time. The excitement doesn’t quite correlate.

For more context, the AUD Gold price has traded within a 9% band for the past 12 months.

Now, if I zoom out and place the recent ‘spike’ in perspective, the AUD Gold price is beginning to trade near 2.5 standard deviations above its weekly mean and trading at 13% above its 200 week moving average. In the second chart below, I’ve denoted other historically ‘stretched’ moments.

Incidentally, Gold priced in Canadian Dollars is exhibiting ‘greater’ Overbought tendencies.

This is a story about knowing where the pendulum is and not necessarily lamenting about missing out on the last 20% or selling too early, as I have indeed done. Regarding the latter, I do tend to enter too early and sell early. Its part of my philosophy of enjoying the ‘fat part of the trade’.

I think anyone acquiring gold assets priced in AUD at current levels (whether bullion, listed equity or exploration tenements) isn’t getting a bargain but instead falling victim to a smaller scale of FOMO.

In the coming weeks, I’ll be watching for any news relating to ‘insiders’ selling shares and whether specific stocks make higher highs

The larger warning is that there are ‘gaps’ below in many trading charts which typically get ‘filled’ at some time.

There will be other chances to buy.

January 9, 2023

by Rob Zdravevski

rob@karriasset.com.au