The following assets (on a weekly timeframe) registered an Overbought reading or traded more than 2.5 standard deviations above its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations)

Nil

Overbought (RSI > 70)

Tin (for the 15th week)

Hot Rolled Coil Steel (for the 45th consecutive week)

Natural Gas

Switzerland’s SMI equity index (for the 9th week)

Australia’s ASX 200 (for the 3rd week)

India’s NIFTY-50 equity index

France’s CAC-40 index

the S&P 500 and Nasdaq 100

and the Stockholm, Copenhagen and Helsinki equity indices.

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Amsterdam’s AEX index

Assets (securities) within my immediate universe which touched the other side of the extreme, being Oversold (where the RSI is < 30) or were at least 2.5 standard deviations below its mean are;

Extremes “below” the Mean (at least 2.5 standard deviations)

the US Government 5 and 10 year bond yields,

the UK, Canadian and German 10’s,

AUD/JPY (signifying a strong Yen versus a weaker AUD),

AUD/GBP (telling us the Pound is strengthening),

the Hang Seng Index,

the Hang Seng China Enterprises Index (now at the same price as March 2020 and 25% below its mid-Feb 2021 high)

Oversold (RSI < 30)

Nil

The Oversold Quinella – Both Oversold and Traded at < 2.5 standard deviations above the weekly mean)

Chinese Government 10 year bond yield (suggesting bonds where being bought aggressively)

Notable deletions from last week’s list include;

a weaker Korean Won, which since strengthened,

Gasoil, Heating Oil ,Gasoline all declined from their higher prices,

as did Coffee and Orange Juice.

Notes & Ideas:

The decliners included Brent Crude (6.5%), WTI Crude (7.6%), Gasoil (5.4%), Heating Oil (5%), Lumber (11%), Platinum (7%), Gasoline (3%), Silver (4.8%), Copper (3%).

Advancers were dominated by soft commodities where Sugar rose 4.3% for the week and Wheat & Corn advanced 2%, Bitcoin was +8%, Ethereum rose 14% and Natural Gas climbed 5.8%.

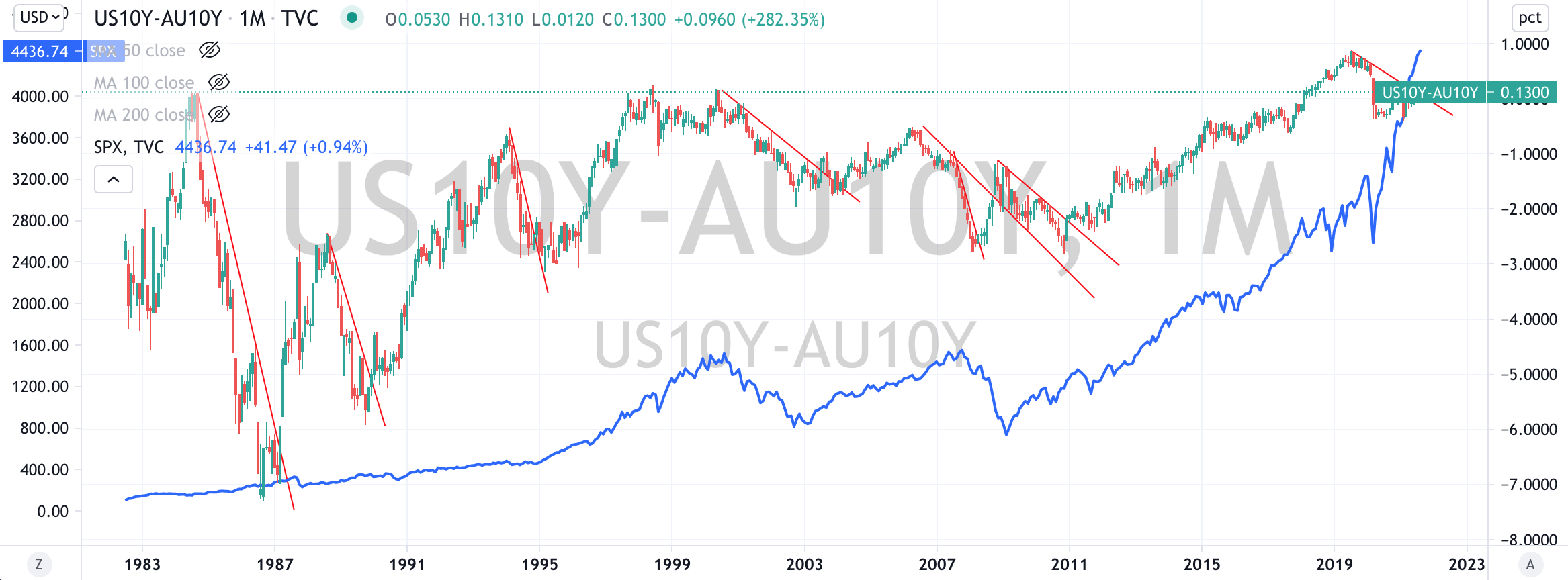

Much action was again seen in falling government bond yields with the U.S. 10 year touching a low of 1.127% before bouncing and closing the week at 1.30%, which is higher than last week’s 1.23% close.

The 10’s remain bound in a larger range but we watch it as broader capital markets could become explosive is the 10’s break decisively either below 1.25% or above 1.65%.

In fact, we saw a bullish outside reversal week for the U.S. 10’s.

Now, probability of higher yields increases, which means bonds will be sold and a likelihood that monies are moved into equities.

Next weekend, look for news headlines reporting that the ‘reflation trade’ has returned. Banks and Cyclicals are the immediate beneficiaries of such money flows.

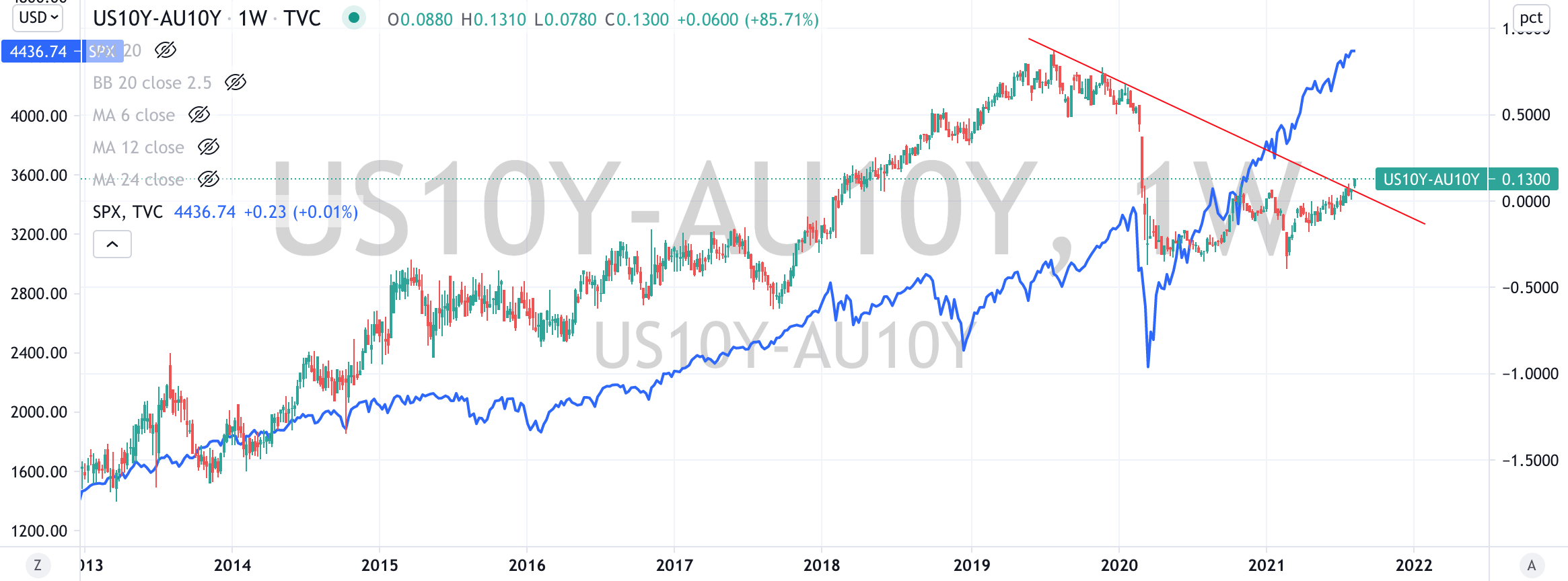

Another signal boding well for higher equity prices, is the troughing in the AUD/JPY price and the Japanese 10 Year bond yield rose from 0.00% to 0.022%. Not a big deal to some, but significant to me. Risk appetites are about to reverse and increase.

The 10’s remain bound in a larger range but we watch it broader capital markets could become explosive is the 10’s break decisively either below 1.25% or above 1.65%.

The risk of lower commodity prices remains as the U.S. Dollar Index (DXY) strengthens and trends higher.

In turn, lower commodities would be welcome relief to ‘end-producers’ benefitting from lower input costs.

Such an example is currently being seen with Iron Ore now back at prices seen in April 2021, but when coupled with extended high prices in Hot Rolled Coil Steel being beneficial for steel producers.

No cryptocurrencies registered any Extreme readings.

And lastly, Bitcoin is trading 200% above its 200 Week Moving Average, which is higher than last week’s 193% reading and notably higher than the reading of 140% seen 2 weeks ago, while certainly lower when compared to its 466% peak in mid-April 2021.

August 7, 2021

by Rob Zdravevski

rob@karriasset.com.au