Macro Extremes (week ending September 26, 2025)

September 28, 2025 Leave a comment

A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) either registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

n.b. pricing of (commodity) futures contracts is only considering the immediate front month.

* denotes multiple week inclusion

Extremes above the Mean (at least 2.5 standard deviations)

Australian 3 year government bond yields

Chinese, Czech, South Korean and Swedish 10 year government bond yields

Italian 2 and 10 year government bond yields

Uranium

Gold in ZAR

AUD/IDR *

AUD/CAD *

COP/USD

USD/IDR

Overbought (RSI > 70)

Lean Hogs

CHF/JPY

EUR/JPY

Shanghai Composite Index *

CSI 300 *

IDX Composite

China’s FCATC *

Spain’s IBEX

Taiwan’s TAIEX *

Nasdaq Composite *

Pakistan’s KSE Index *

South Korea’s KOSPI *

Nikkei 225

Japan’s Nikkei 225

Czechia’s PX Index *

South Africa’s SA40 *

Chile’s IGPA and IPSA indices *

Philadelphia Semiconductor Index (SOX) *

Canada’s TSX *

Vietnam’s VN Index *

And the ASX Small Cap Index *

The Overbought Quinella (Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Silver in AUD & USD *

Gold in AUD, CAD, CHF, EUR, GBP and USD

Mexico’s IPC Index

Extremes below the Mean (at least 2.5 standard deviations)

None

Oversold (RSI < 30)

U.S. 3 month bill yield *

Richards Bay Coal *

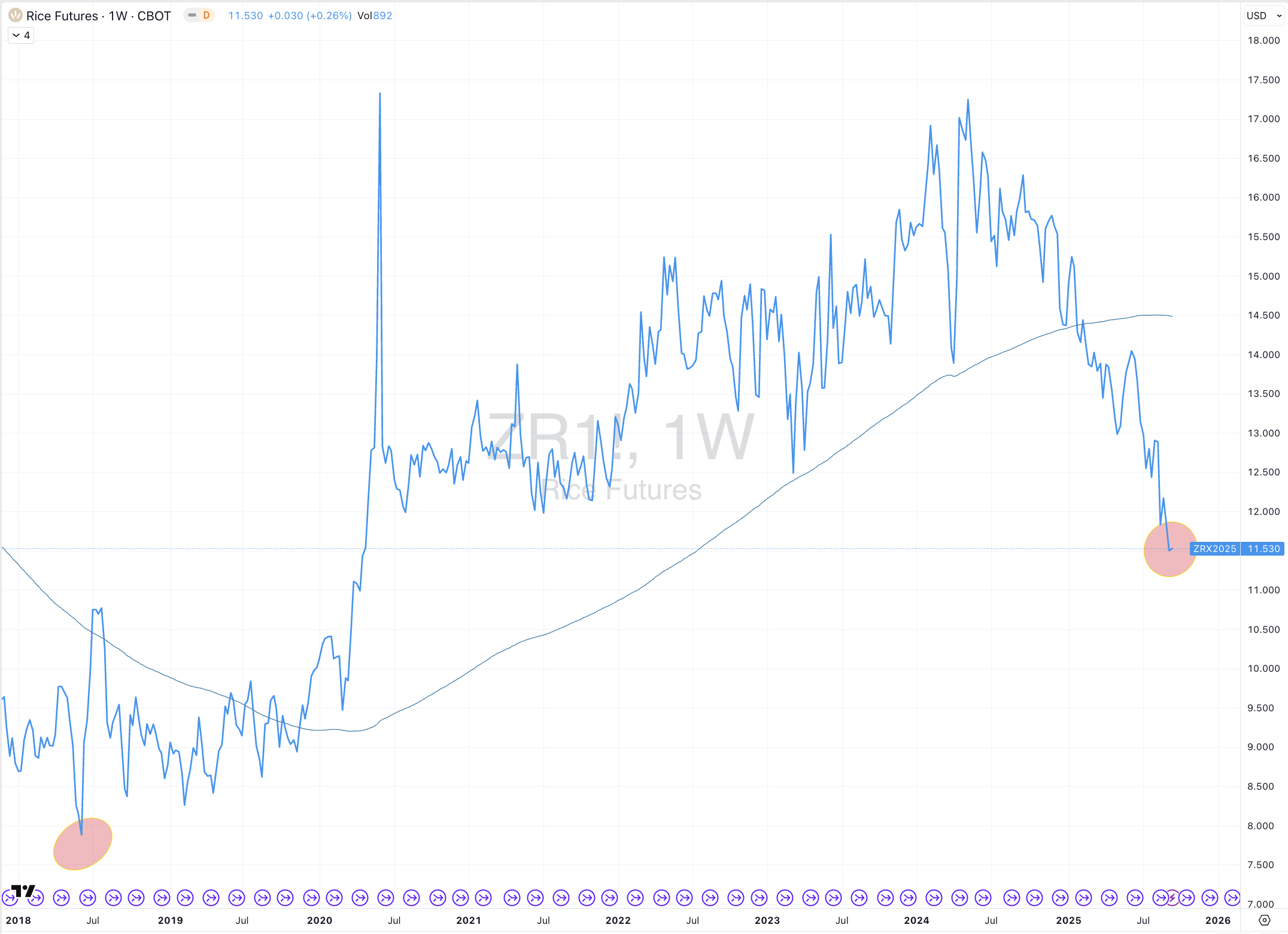

Rice

JPY/EUR

NZD/AUD

The Oversold Quinella (Both Oversold and Traded at < 2.5 standard deviations below the weekly mean)

Philippines PSE equity index

Notes & Ideas:

Government bond yields were quiet.

U.S. corporate bond yields (and the high yield effective yield) are a whisker from oversold levels and at are at their most oversold since December 2020.

Czech 10 year yields and the U.S. 5 year minus U.S. 3 month yield have risen for 4 weeks.

Swiss 10 year bond yields have fallen for 5 weeks.

And Swedish, Italian and Korean 10 year yields are in oversold territory.

Equities were mostly lower, again.

The S&P 500 eased slightly, which was enough to leave overbought land.

We see a return of Spain’s IBEX and Japan’s Nikkei 225 to the overbought list.

HSCEI Index and Brazil’s BOVESPA equity index are no longer at overbought extremes.

The TAIEX and Nikkei 225 have risen for 5 weeks.

The ASX Industrials have fallen for 5 weeks, while the Dow Jones Transports rose and broke its 4 week losing streak.

AEX, KSE, N225, PX and SOX are in 4 week winning streaks.

The TAIEX has risen for 5 weeks.

The DJ Transports rose and broke 4 weeks of loses.

The Russell 2000 fell and broke a 7 week streak of advance.

Canada’s TSX technically broke its 7 week winning streak by falling a mere 0.02%.

While the ASX Small Caps stretches its winning streak to 8 weeks.

Commodities were busy and mostly firmer.

Oils, Precious Metals, Lumber, Copper, Coffee and Sugar were amongst the notable gainers.

Cocoa, Steel, Urea, Oats and Rice dominated the losers category.

Uranium joins Gold in overbought territory.

Lumber rose and isn’t oversold.

The Copper/Gold ratio is nearing oversold levels.

Gasoil has climbed for 4 consecutive weeks.

Lean Hogs, Silver in AUD & USD along with Gold in AUD, CAD, CHF, and ZAR are all in a 6 week rising streak.

Platinum has risen for 8 weeks.

Cocoa has declined for 6 weeks.

Richards Bay Coal and U.S. Gulf urea prices are in 9 week losing streaks.

Currencies were active, again.

There have been some changes in this weeks currency entrants and some streaks are developing and extending.

The Aussie was weaker, again.

The Euro and CHF were firmer.

Swissie/Yen has risen for 6 weeks, but CHF/USD fell and broke its 6 week winning streak.

The Loonie eased.

Yen was weaker and we are seeing JPY/EUR fall for 4 weeks and Yen/USD down for 5 weeks.

The USD has fallen for 4 weeks against the South African Rand,

And the Kiwi has slumped for 8 weeks against the Aussie.

The larger advancers over the past week comprised of;

Bloomberg Commodity Index 2.1%, Brent Crude 5.2%, Baltic Dry Index 2.5%, WTI Crude 5.3%, Lean Hogs 3.6%, Copper 3.1%, Heating Oil 5.4%, Arabica Coffee 3.2%, Lumber 4.6%, Palladium 12.1%, Platinum 11.2%, Gasoline 4%, Robusta Coffee 1.6%, Sugar 2.7%, S&P GSCI 2.8%, CRB Index 2%, Gasoil 5.7%, Uranium 5.9%, Silver in AUD 7.7%, Silver in USD 6.9%, Gols in AUD 2.8%, Gold in CAD 3.2%, Gold in CHF 2.4%, Gold in EUR 2.4%, Gold in GBP 2.6%, Gold in USD 2%, Gold in ZAR 2%, Mexico 1.8%, XBI Biotechs 2.5%, ASX Materials 5.9%.

The group of largest decliners from the week included;

Cocoa (4.6%), U.S Midwest Hot Coiled Steel (3%), LNG in Yen (2.1%), Urea Middle East (1.8%), Oats (3.8%), Rice (2.2%), HSCEI (1.8%), Hang Seng (1.6%), KRE (1.8%), KOSPI (1.7%), NIFTY (2.7%), Copenhagen (2.2%), PSE (3.8%), SENSEX (2.7%), SMI (1.5%) and Nasdaq Transports fell 1.5%.

September 28, 2025

By Rob Zdravevski