Macro Extremes (week ending March 4, 2022)

March 7, 2022 Leave a comment

The following assets (on a weekly timeframe) registered an Overbought reading or traded more than 2.5 standard deviations above its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations)

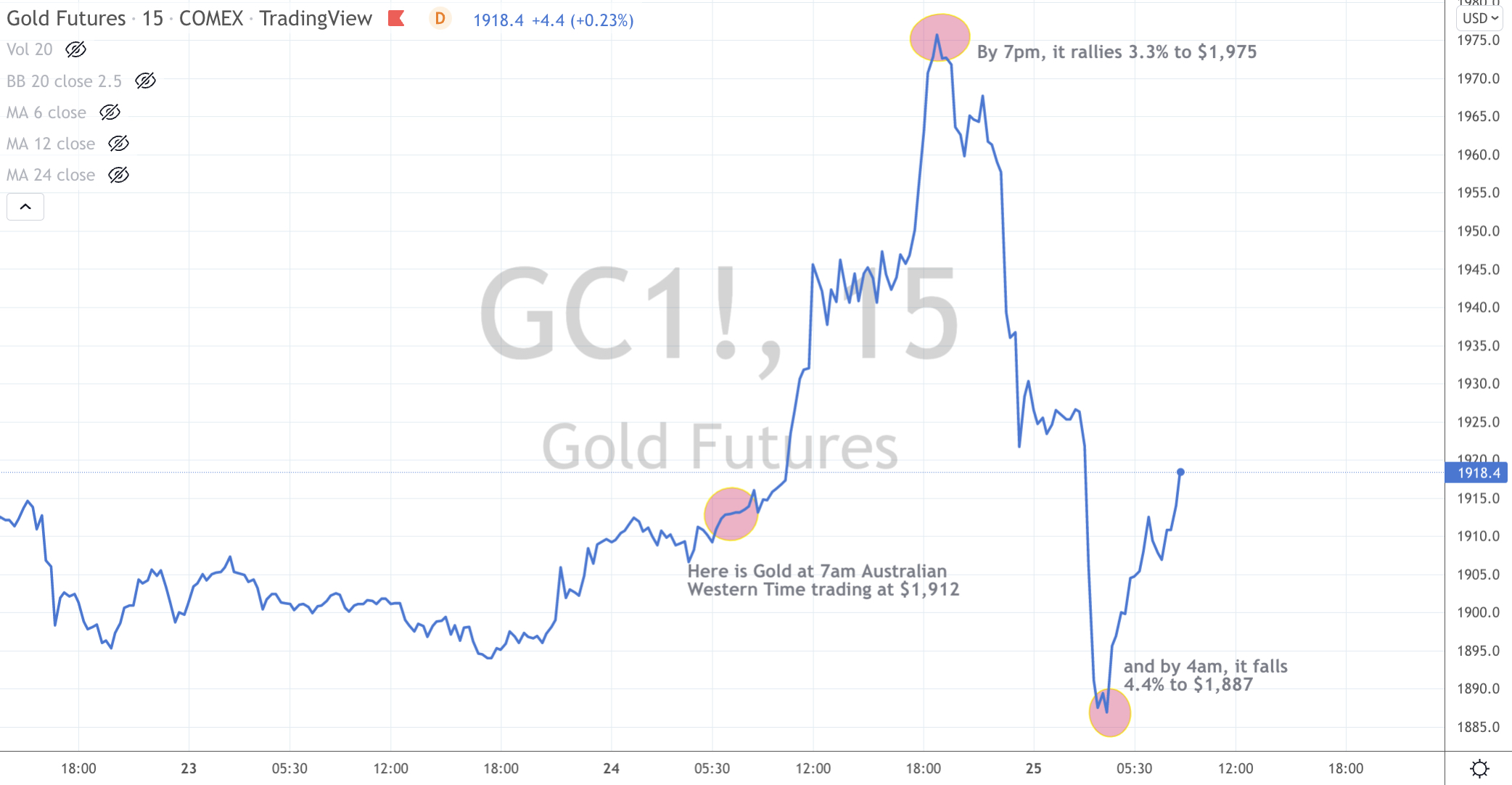

Gold

LNG

Copper

USD Index (DXY)

Uranium

Overbought (RSI > 70)

Australian 2, 3 and 5 year government bond yields

U.S. 2 year government bond yields

Greek & New Zealand 10 year government bond yields

Tin

Soybean

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Russian 10 year government bond yields

Bloomberg Commodity Index

CRB Index

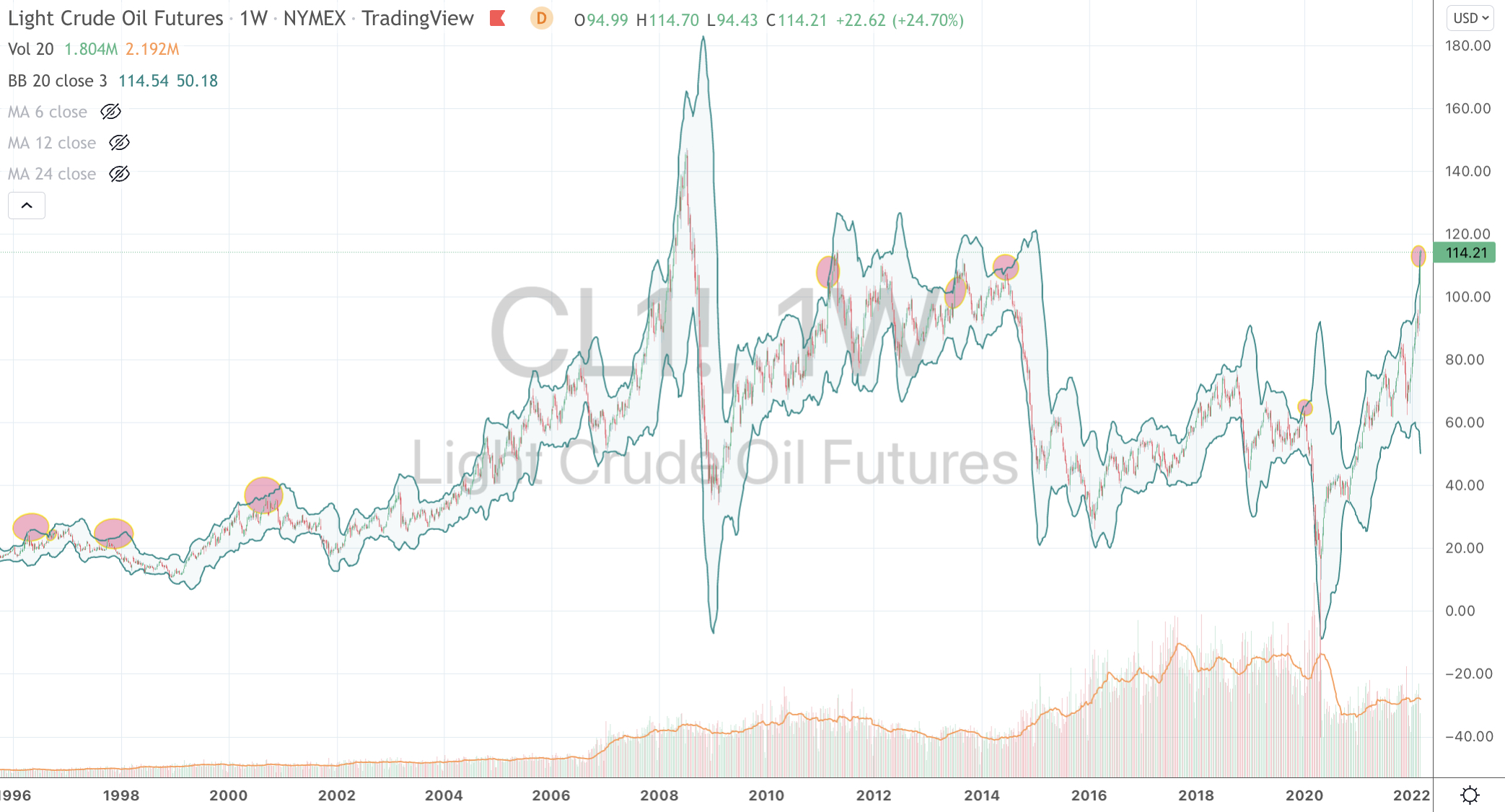

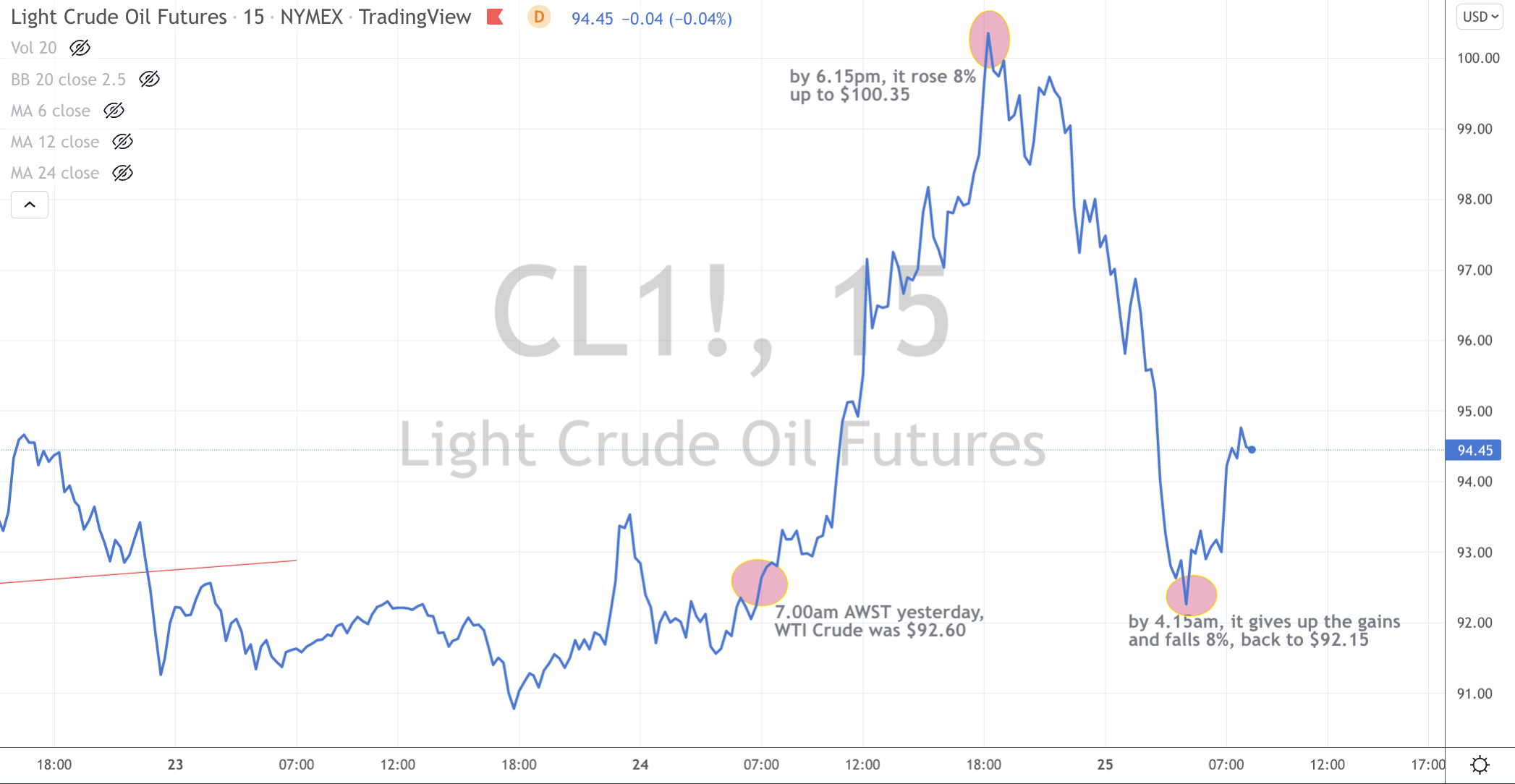

WTI Crude Oil

Brent Crude Oil

Gasoline

Heating Oil

Gasoil

Dutch TTF Gas

Aluminium

Rotterdam Coal

Australian Coal

Palladium

Nickel

Corn

Wheat

Rice

Nikkei 225 Index

Gold Volatility Index

Assets (securities) which touched the other side of the extreme, being Oversold (where the RSI is < 30) or were at least 2.5 standard deviations below its mean are;

Extremes “below” the Mean (at least 2.5 standard deviations)

KRW/USD

EUR/AUD

EUR/USD

DKK/USD

SEK/USD

RUB/USD

Dow Jones Industrial Average

Sensex

Swiss SMI

Oversold (RSI < 30)

U.S. 10 year minus 2 year government bond yield spread

(Now at the same level as March 9th, 2020)

The Oversold Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

AEX, CAC, DAX, MIB, IBEX, Helsinki & Stockholm equity indices

Notes & Ideas:

It was a “relative” mute week for American indices but not so for European counterparts.

Helsinki’s bourse took a bruising by falling 11.4% in the week, due to proximity to Russia and murmurs of them yielding neutralism and possibly joining NATO, while France;s CAC and the German DAX both 10% for the week.

It was a week for the record books.

While the biggest news in in the energy complex, there are interesting parables such as Natural Gas still not above its September 2021 highs.

Some of the moves were extraordinary. Rotterdam delivered coal rose 99% in a week and Gasoil (diesel) soared 42%.

The second biggest news is the moves in bond yields.

Aussie 10’s (which aren’t overbought) moved from 2.25% to 2.10%.

Canadian 10’s yields fell from 1.90% to 1.66%, while the yield in French 10’s collapsed from 0.70% to 0.44%.

Inversely, the Russian Central Bank double its policy rates and thus the traded 10’s rose from 12.2% to 19.9%.

For owners of French bonds, I wonder how tempting it may be to cash in their 0.44% yielding bonds, convert EUR into a very weak Ruble to Buy 20% yielding government bonds.

While the French rely on Russian nuclear fuel to power the nuclear power stations which generates 70% of their electricity, the analysis is will the Russian Government be creditworthy to pay back that bond and not default.

The larger advancers over the past week comprised of;

Aust. Coal 30%, Aluminium 13.7%, Rotterdam Coal 99.3%, Brent Crude 19.9%, Baltic Dry Index 3.5%, WTI Crude 26.3%, DXY 2%, Iron Ore 2.2%, Gasoil 41.6%, Copper 10.1%, Heating Oil 32.5%, Hot Rolled Coil Steel 16.3%, JKM 40.5%, Lumber 9.3%, LNG 58.6%, Natural Gas 12.2%, Nickel 20.7%, Orange Juice 8.8%, Palladium 26.3%, Platinum 6.3%, Gasoline 23.3%, Sugar 7.6%, Silver 7.4%, CRB 13.4%, TTF 106.7%, Urea 15.9%, Uranium 7.9%, Gold in AUD 2.3%, Gold in USD 4.3%, Corn 14.4%, Oats 8.3%, Rice 6.7%, Soybeans 4.8%, Wheat 40.6%, KOSPI 1.4% and Australia’s ASX 200 1.6%.

The group of decliners included;

Hogs (3.1%), Coffee (6%), Cattle (4.3%), AEX (7.7%), KBW Banking Index (4.4%), CAC (10.2%), DAX (10.1%), MIB (12.8%), HSCEI (3.8%), Hang Seng (3.8%), IBEX (9%), S&P 400 Midcap (1.8%), Nasdaq 100 (2.5%), Nikkei (1.9%), Sensex (2.5%), Helsinki (11.4%), Stockholm (7.3%), Russell 2000 (2%), SMI 5.7%, SOX (5.6%), Singapore’s STI (2.1%) and FTSE 100 fell (6.7%).

March 7, 2022

by Rob Zdravevski

rob@karriasset.com.au