It’s nearly 10 years since Australian Iron Ore and Lithium mining company, Mineral Resources (MIN.AX) last traded this many percentage points below its 200 week moving average.

Today, #AngloAmerican (AAL) has said it received a #takeover offer from #BHP.

#AAL is now 48% higher since that December 13, 2023 note.

M&A activity is increasing and in this case, it is easier to buy existing copper and nickel mines, rather than developing them. BHP would also get 85% ownership of De Beers Group (diamonds) too.

If this deal closes, they won’t exactly become ‘private’ but certainly eases the quarterly investor and analyst palaver for AAL management.

Although, it is early at this dance, it’s always possible that a privately held suitor emerges with buying interest that doesn’t require any de-merger of Anglo American’s divisions or business lines.

Long time readers of my blog would confirm that I have had a structural bullish view on #uranium for some years.

For now (at least 3 or 4 weeks ago) the collective uranium basket is full.

If I could express what I think is next, through the NYSE listed share price of #Cameco, I’ll await for CCJ.N to come back to the $27-$30 mark somewhere in the May-July 2024 timeframe before adding some more.

In fact, why dig up the stuff if you are losing money on it or your costs are rising and crimping your margins?

but due to this news, the stock price fell 19% last Friday and 6% more in the following 2 days of trade.

Obviously, this would not happen if it was a privately held company.

And so, I think we’ll see a growing trend of listed companies becoming owned by private equity, sovereign and pension funds.

Benefits of such a trend would include allowing executives to move away from ‘short-termism’ and thus freeing up time that they currently spend appeasing public shareholders.

But the best part is not being forced to produce and grow at any expense, pressured by shareholder expectations and you also have most (if not all) of your funding and borrowing covered.

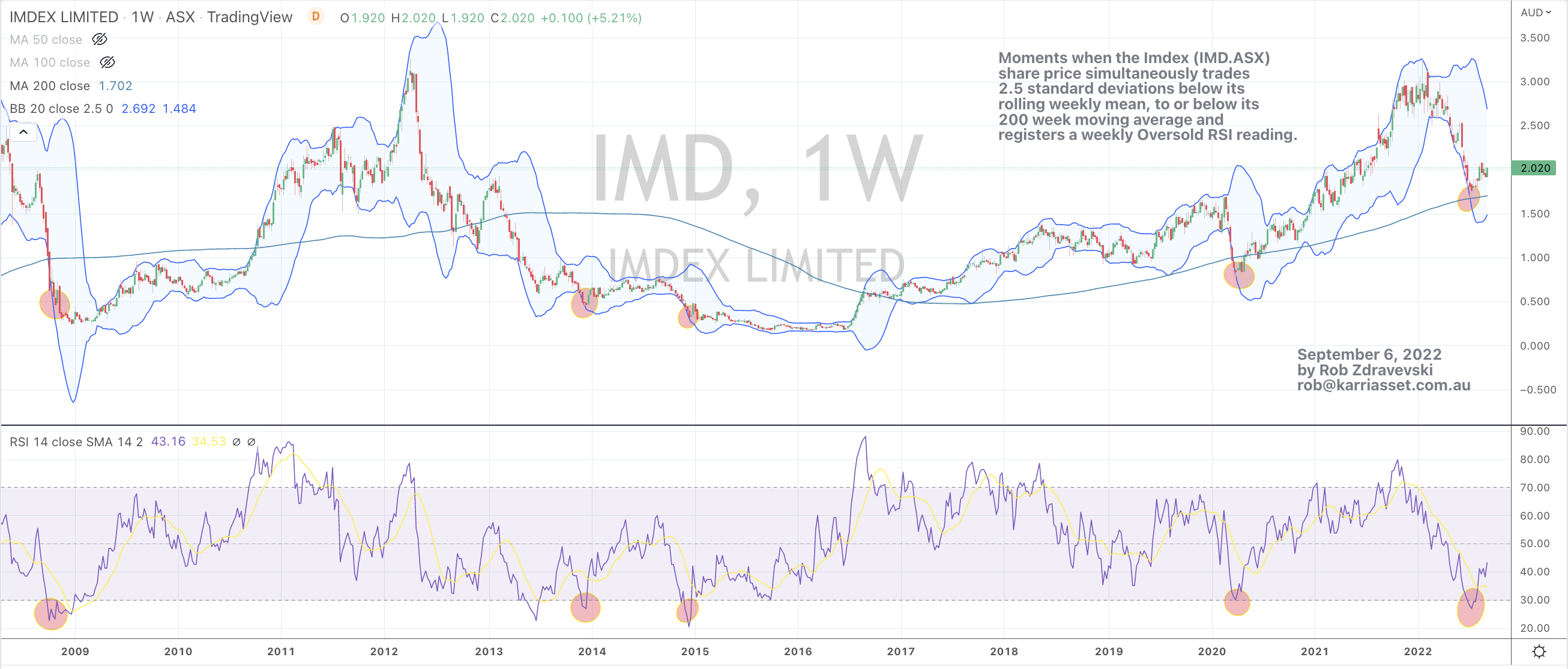

Accumulating shares in Imdex (IMD:ASX) is a one way I am expressing my view amid a larger theme of the world requiring more mining projects to supply a host of ‘ingredients’.

The bigger picture is that I expect mining exploration and production capex to rise over the next decade. While the easy and low hanging fruit (resources) have been had, better technology with be required to aide financing and feasibility decisions.

Imdex also falls into another investment theme which I like being the testing, certification and verification sector.

Put it this way, it’s akin to owning the ‘pick and shovels’ coupled with technological enhancements which assist speed, precision, efficiency and cost savings.

Recently, Imdex shares traded down my longer term ‘Oversold Trifecta’ for only the 5th time in the past 15 years.

Those metrics are a combination of when the share price simultaneously trades 2.5 standard deviations below its rolling weekly mean, (at least) down to or below its 200 week moving average and registers a weekly Oversold RSI (Relative Strength Indicator) reading.

The volume of drilling activity in the global gold industry has fallen by 55 per cent in the past 12 months, new data from research group IntierraRMG has found.

Less exploration means supply.

Less gold supply should mean a higher gold price, ONLY if gold demand stays steady or rises.

Such a scenario will benefit gold companies who have a proven resource.

Often, the best thing such a company can do, is to leave the gold in the ground rather than spending hundreds of millions of dollars trying to extract it.

Management who think that success is measured by how much gold they “pour” can prove to be a handicap for its company’s share price, especially when capital is scarce.