When Private Equity firms, themselves, go public.

April 16, 2024 Leave a comment

It all started when Fortress Investment Group went public on February 9, 2007, and the IPO was priced at $18.50 per share.

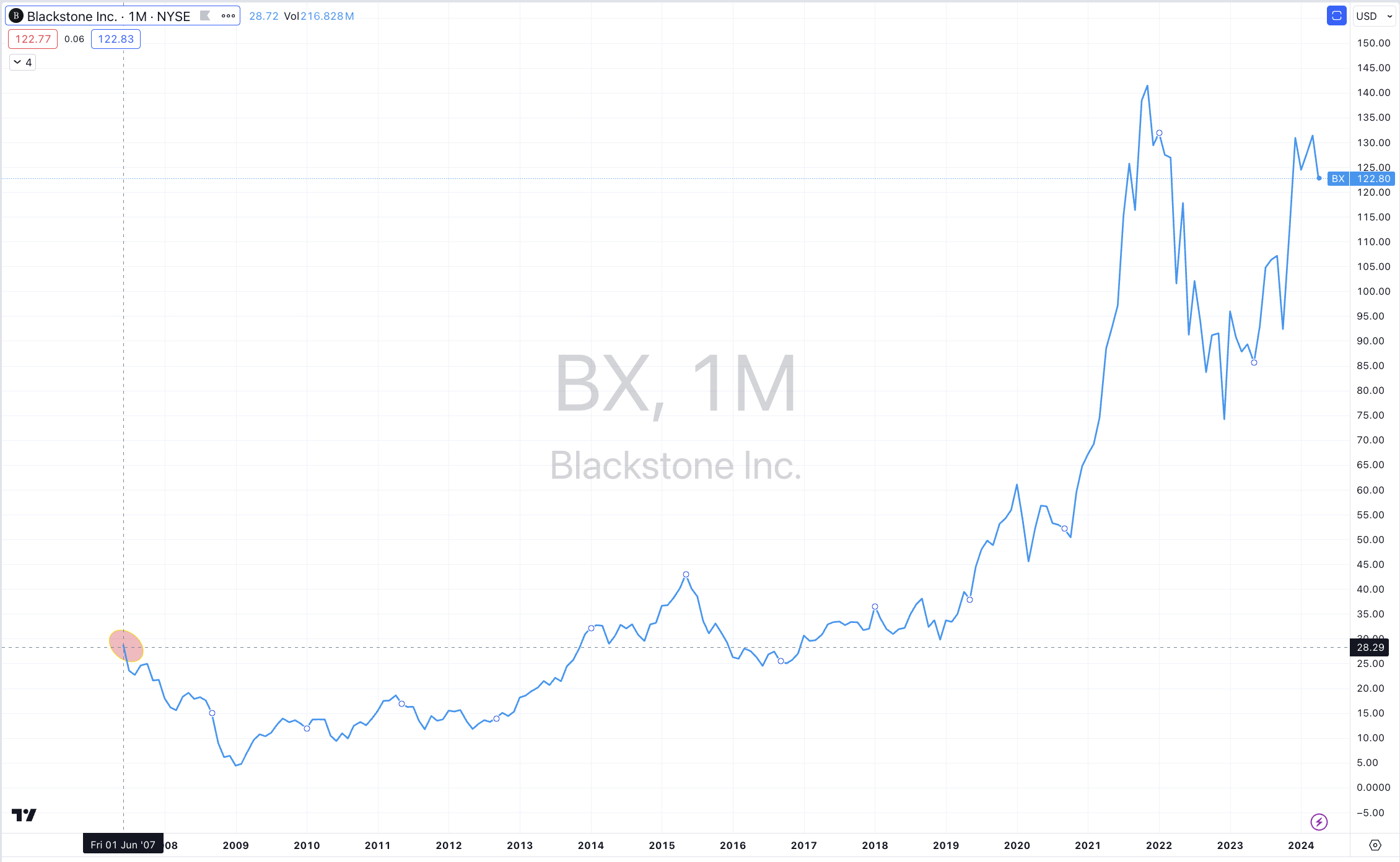

Next, Blackstone went public in June 2007 when its IPO was priced at $31.

KKR priced its IPO at $10 in July 2010.

At the time of KKR going public, shares in Blackstone Group (BX) and Fortress Investment Group (FIG) had fallen by 71% and 87% respectively since their market debuts in 2007.

Apollo Global Management was next to list their shares, when on March 30, 2011 their IPO was priced at $19

The Carlyle Group went public on May 3, 2012, and the IPO was priced at $22 per unit.

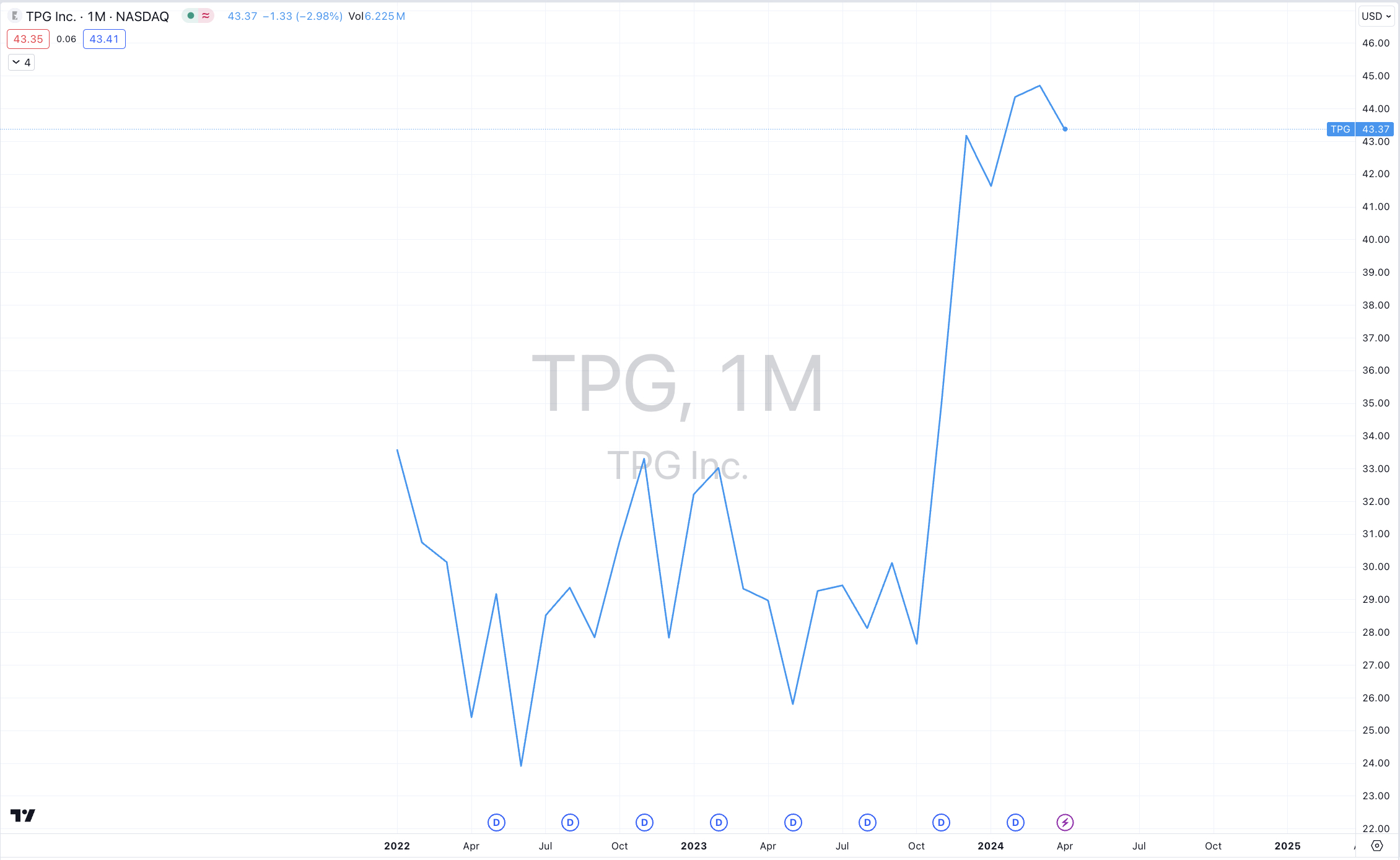

More recently, TPG went public on January 13, 2022, and the IPO was priced at $29.50 per share.

Everyone’s charts are below except for Fortress (FIG) because in Q1 of 2017, Softbank acquired them for $8.08 per share.

Today, CVC announced their interest in going public.

Over a 10-15 year timeframe, it’s not clear cut whether there is merit backing the ‘sponsor’ in every case.

April 15, 2024

by Rob Zdravevski

rob@karriasset.com.au