This is when gold producers should be locking in their selling prices.

Perhaps to offer their equity as currency to acquire non-profitable mines.

Some companies may even ‘trick’ investors (and reward bankers) by raising capital at this moment.

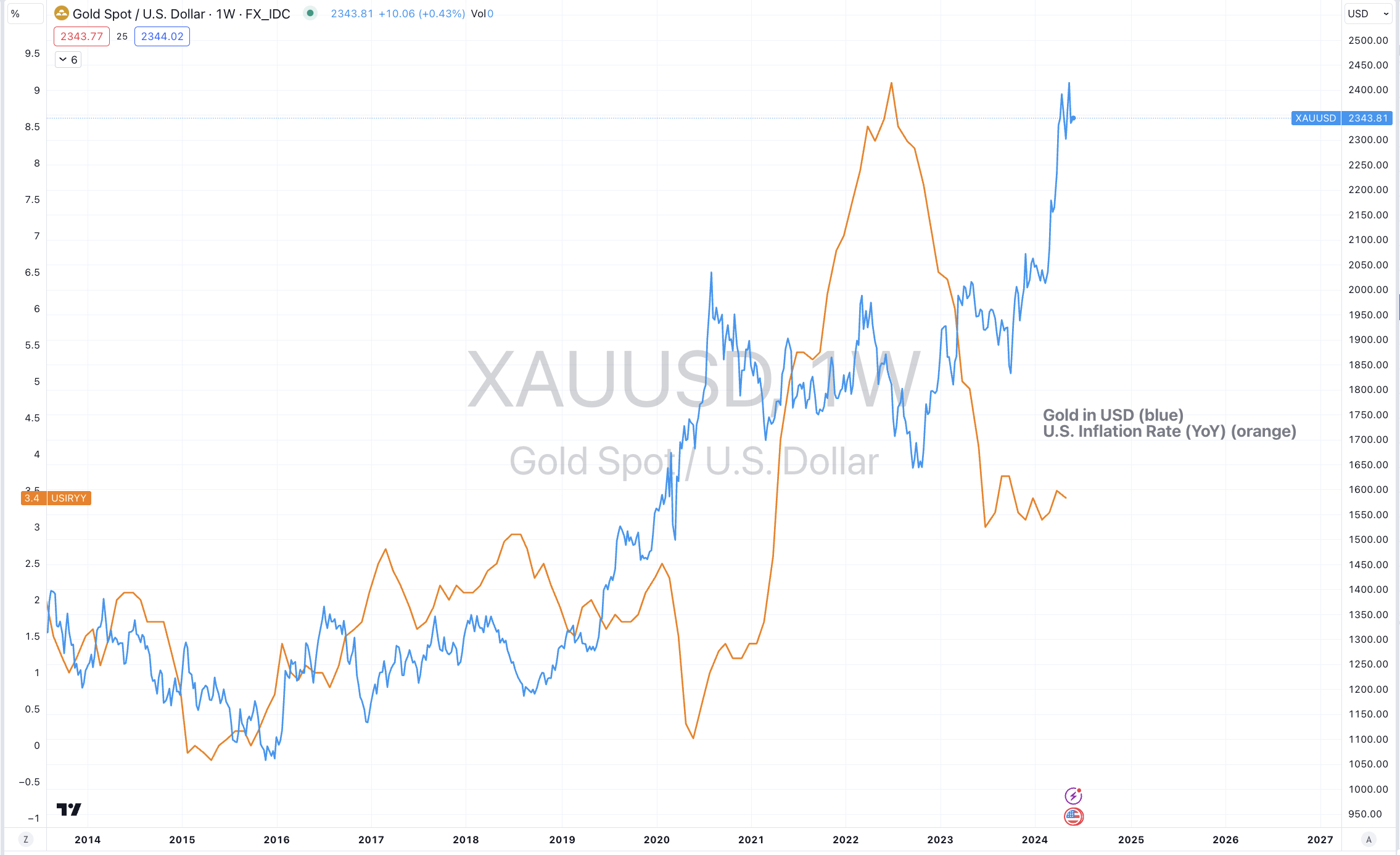

Gold prices are resembling parabolas,

and the study below can’t convince me towards the probabilities of buying Gold ‘with new money’ today or tomorrow.

While animal spirits are absent and prices can become giddy, mean reversion should be respected.

But not all the equity prices of gold producers are hitting all-time highs.

Why?

Because profitable mining projects remain difficult.

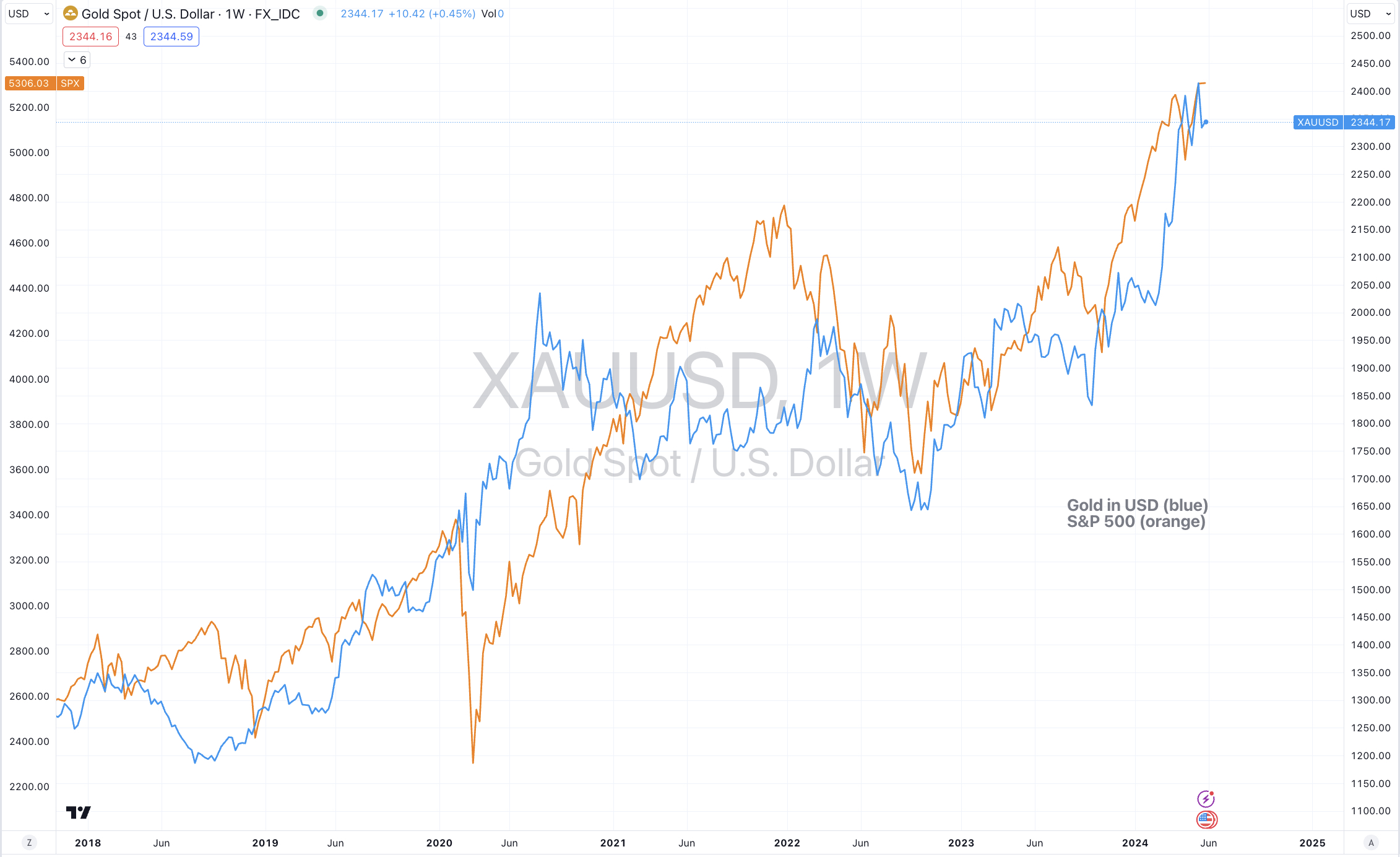

p.s. for some perspective, Gold (as priced in USD) has risen 14% over the past 3 months (I just chose an arbitrary starting point)……many things have had similar returns including the S&P 500 and the price of Lean Hogs.

“It’s unlikely that automobile manufacturers will walk away from the capital expenditure spent on engine development and assembly, while synthetic fuels are making ICE’s even more cleaner.

Commensurate to introducing electric vehicles into their stable, auto companies have also made statements that they still expect the ICE to be part of their business for the next 30 years.

The note also observed Palladium’s premium above the price of Platinum (implying that the gap is narrowed as Palladium declines and Platinum rises) along with my expectation of mean reversion/convergence in the Gold price.

Gold did mean revert, Platinum rose and Palladium’s premium collapsed.

Since that note was published, both Platinum and Gold have risen 11%.

And Palladium is now cheaper than Platinum.

Now, Mercedes Benz has said it will continue to make combustion-engine and hybrid vehicles “well into the 2030s,” if demand is there.

For buyers of buying gold related equities at current levels, probability isn’t stacked your way.

“They” are closer to being a sell, than a buy.

If expressed in the form of the GDXJ (Van Eck Junior Gold Miners ETF), I think I’ll be able to buy it 25% cheaper than todays $42.67.

And be careful of historical charts showing where prices “once came from” and phrases such as ‘breakouts’ and “resistance lines”, whether its monthly or weekly or daily or hourly………

The date of that note (September 22, 2023) are highlighted within the charts below.

Also in that note, I was looking for the price of #Newmont (NEM:US) to trade down to $32.50.

It has now done so…..but I don’t think it has bottomed.

I’ll look for lower prices in Newmont stock before becoming interested.

As for the gold price, AUD gold is becoming ‘full’ and while CAD and USD Gold may trend higher, this is not an entry point for me, but merely a mid to late stage participatory trend.

You don’t have to be there because there are other #commodities to consider.