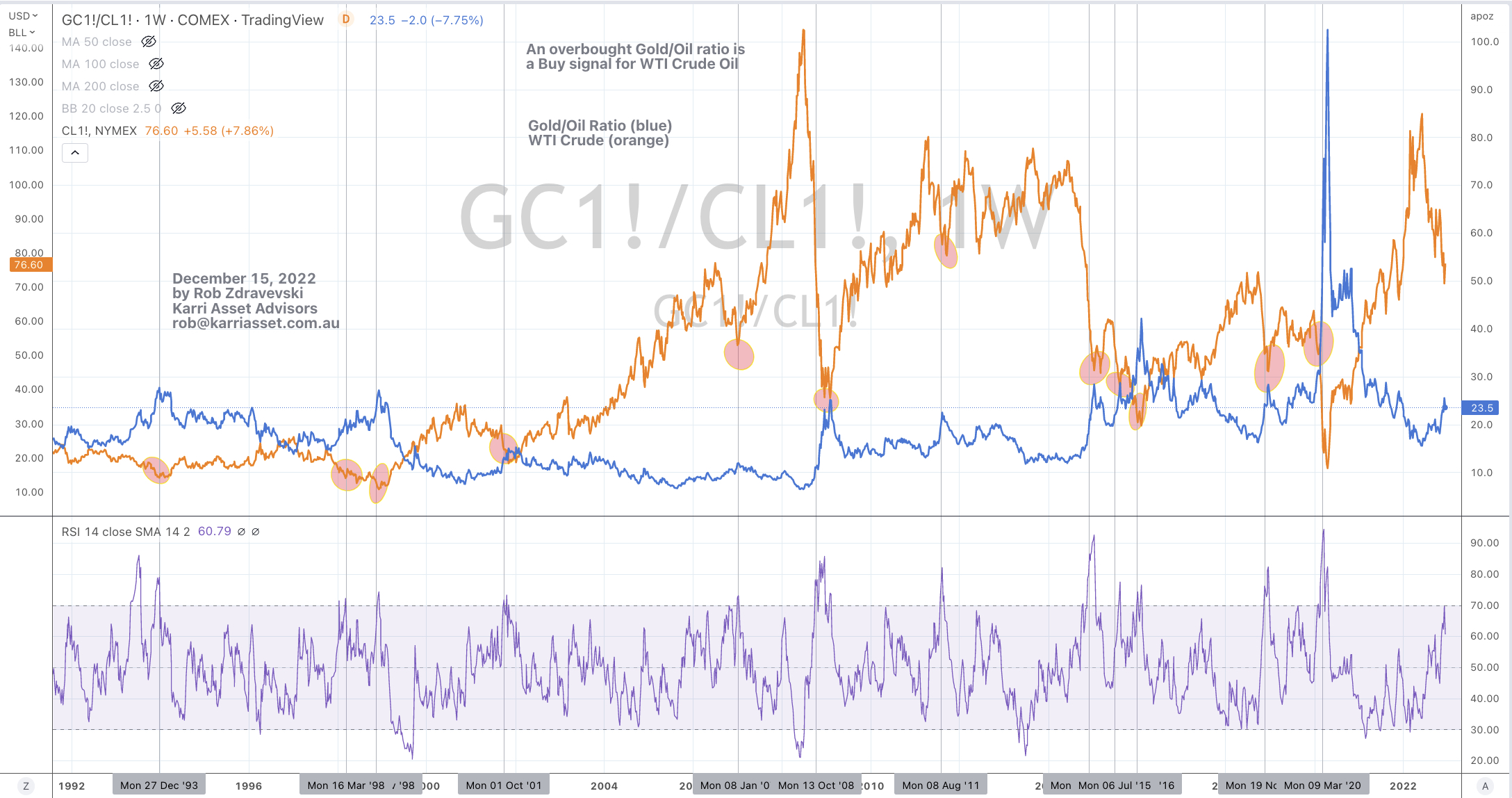

and for something acutely related to the Gold/Oil ratio…..

when we find the Gold/Oil ratio at overbought levels on a weekly basis, this suggests that the price of WTI Crude Oil is in buying territory.

We are potentially approaching the 14th time (over the past 30 years) that this buying signal will occur.

Keep in mind, I’m talking about the price of Oil.

Logically, oil related equities should also prosper and have the ability to deliver operational leverage, however you’d need to do the research on any specific companies numbers such as their debt, interest expenses, free cash flows, contracted or forward delivery prices etc etc.

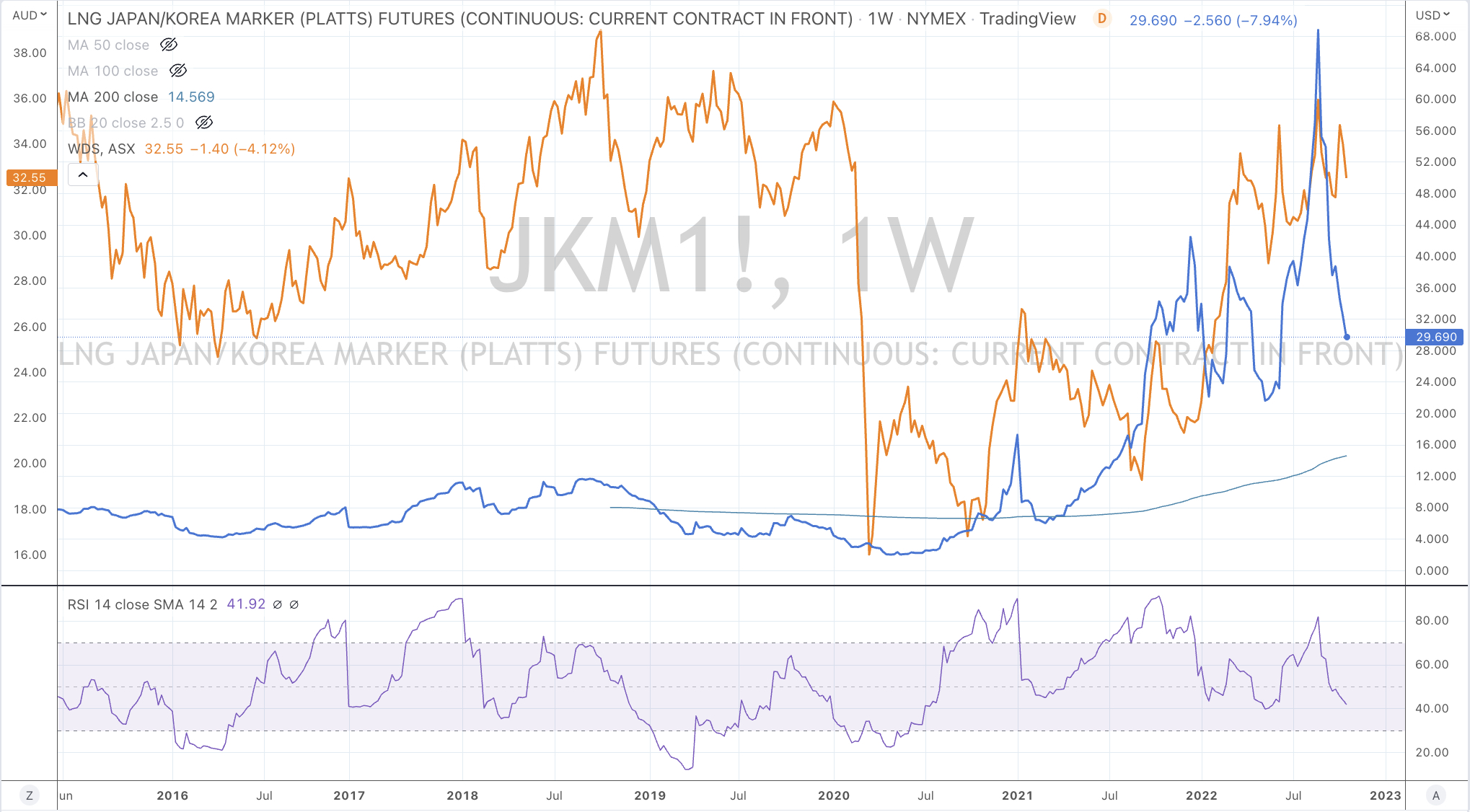

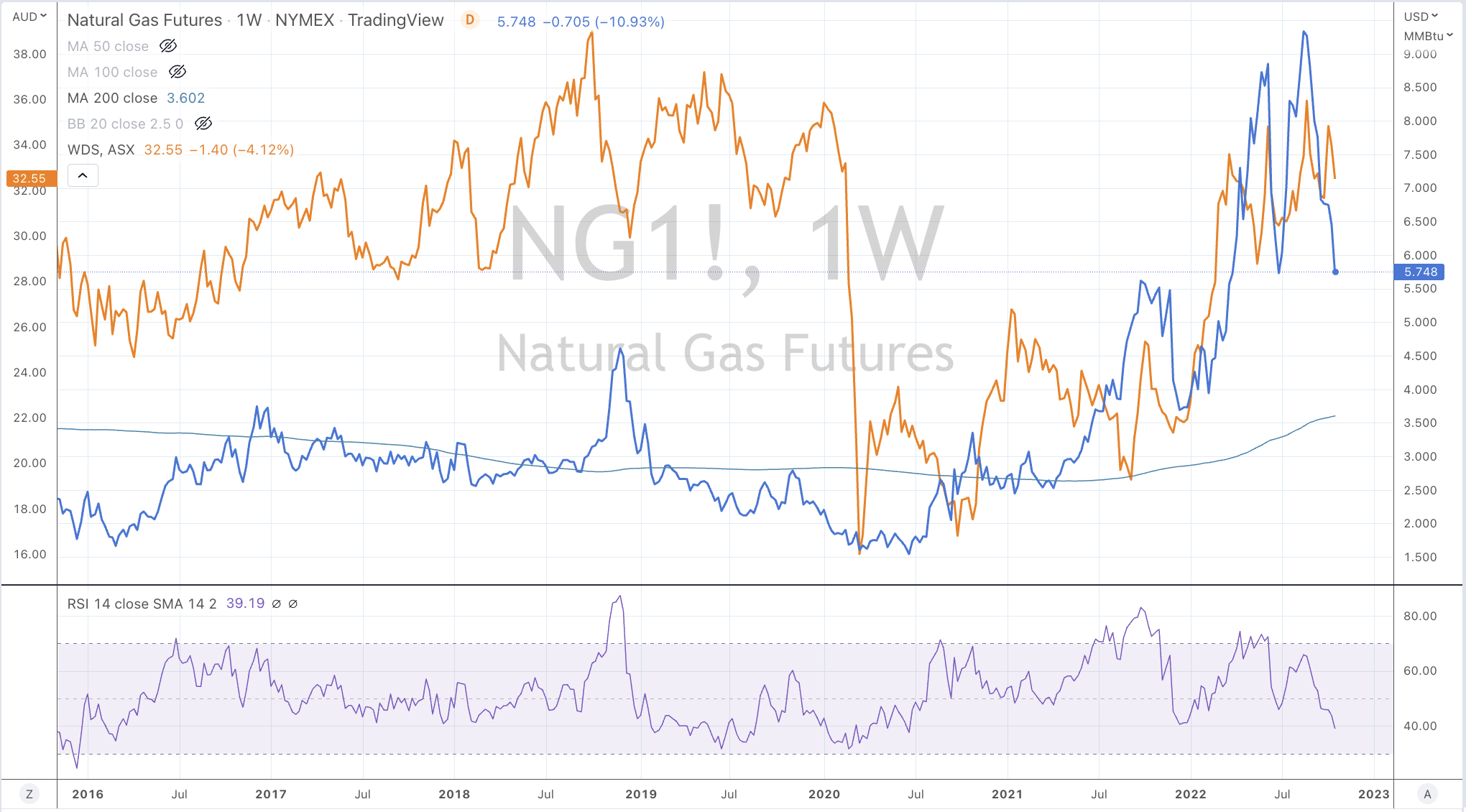

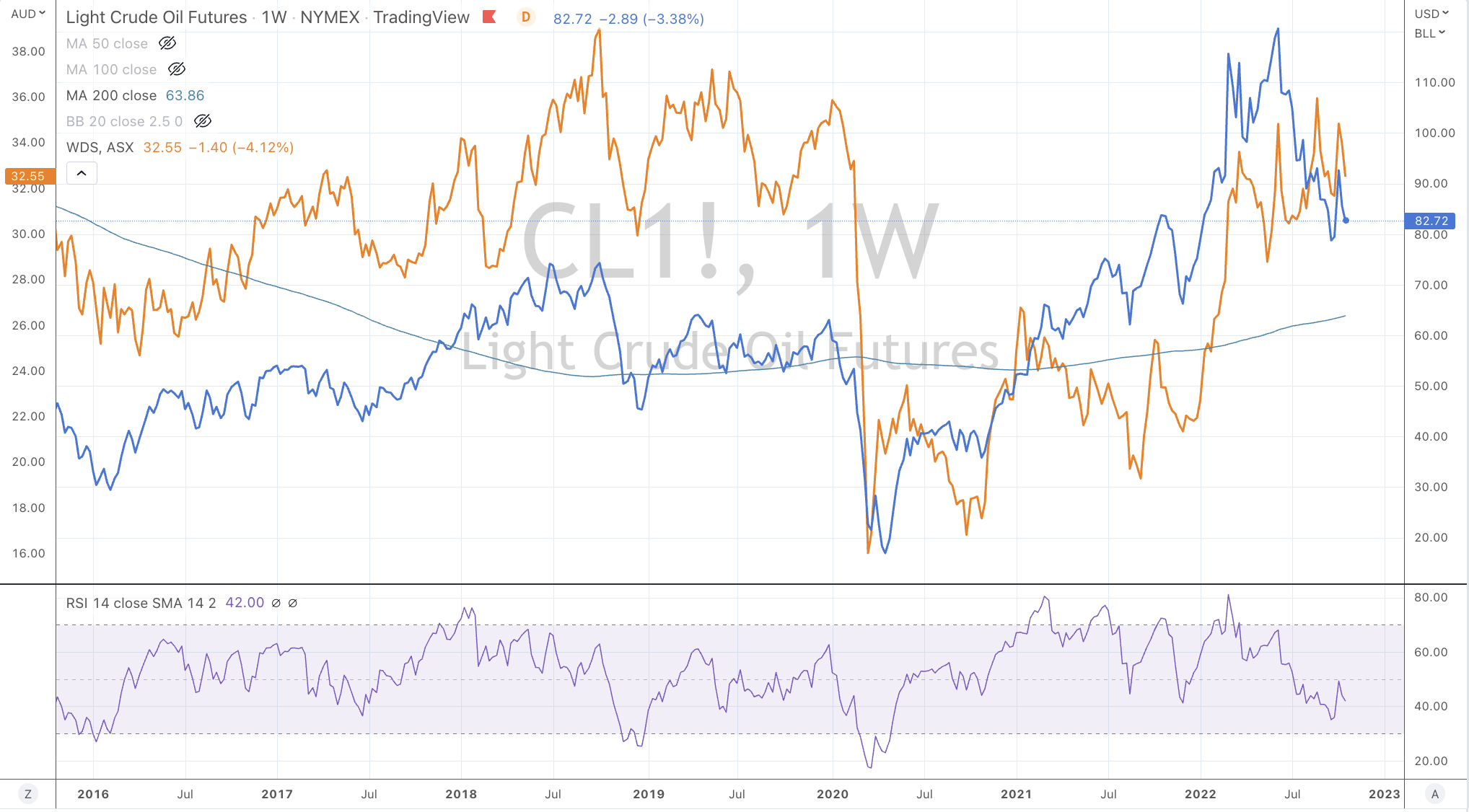

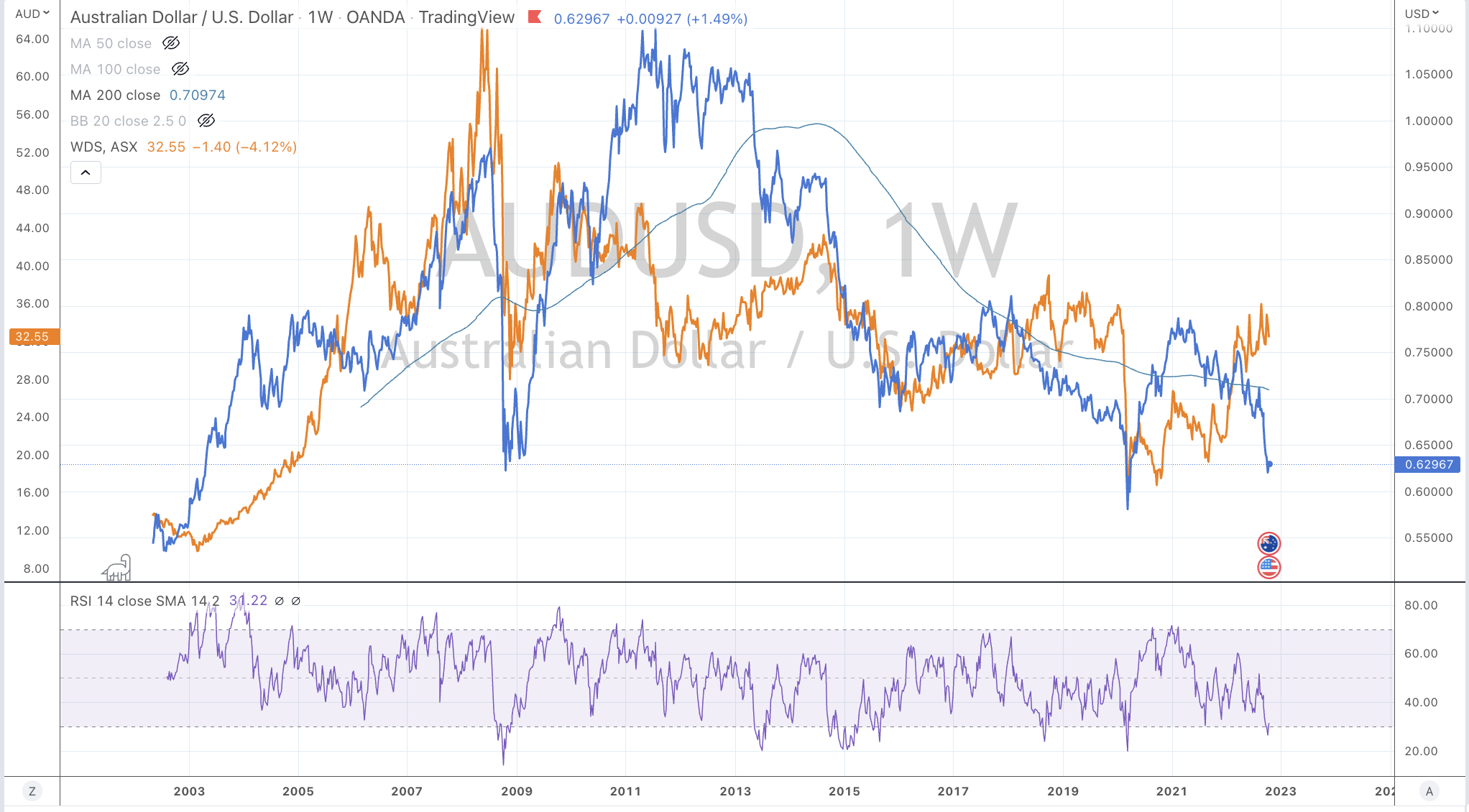

The next directional move in Woodside shares hinge on the direction in and or a combination of the Japan/Korea LNG Marker, the U.S. Natural Gas price, the West Texas Intermediate (WTI) Crude Oil prices along with the AUD/USD.

The charts below show the various correlations between Woodside shares and those assets.

My analysis of Woodside shares suggests that has a further 15% downside risk to $28, which is where I will be a buyer.

I may perform this exercise across other energy related equities.

JKM LNG Marker (in blue) versus WoodsideHenry Hub Natural Gas (in blue) versus WoodsideWTI Crude Oil (in blue) versus Woodside AUD/USD (in blue) versus Woodside

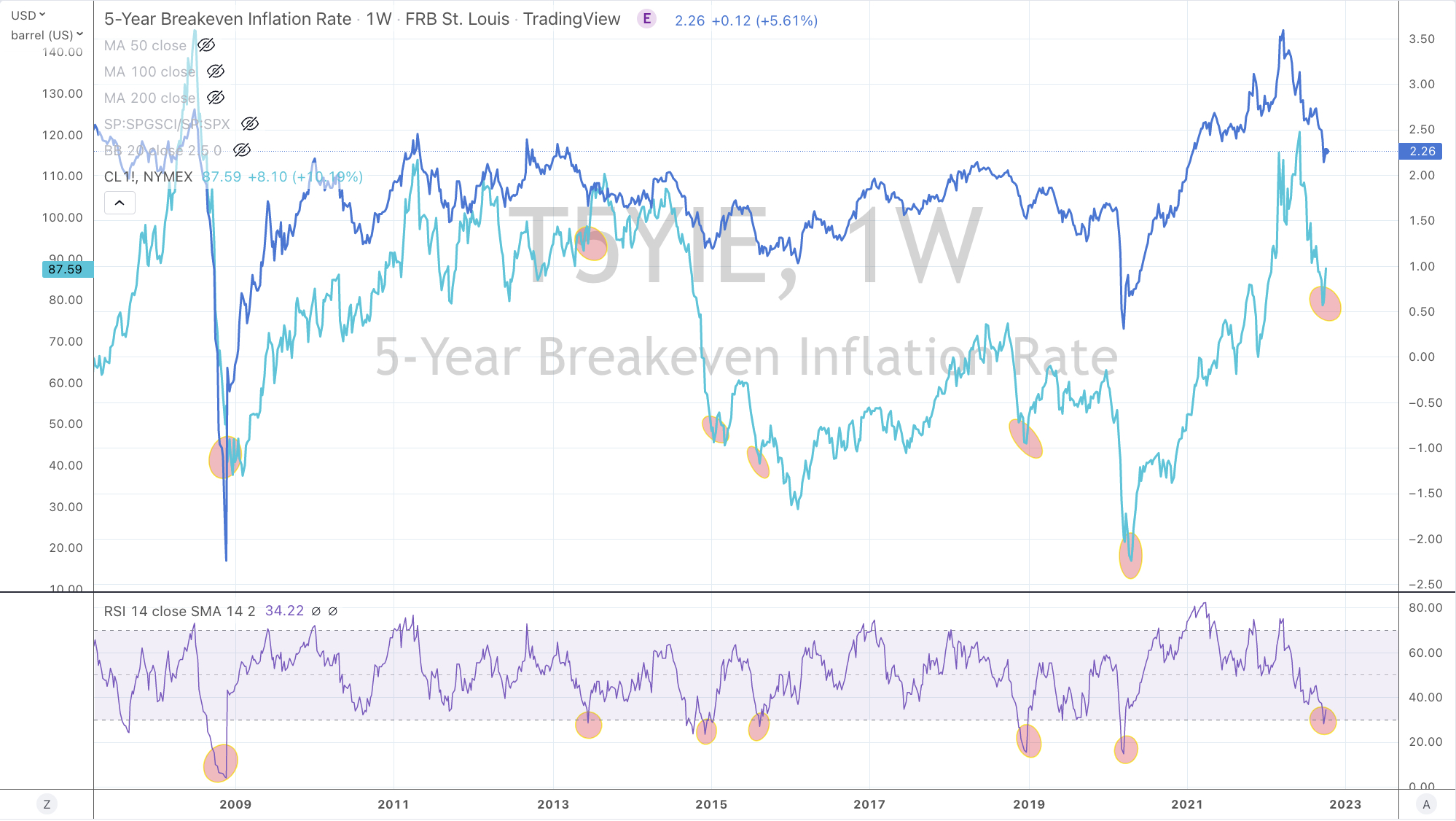

Here is a lovely chart showing the price of WTI Crude compared to U.S. 5 year break-even inflation rate.

To which the St. Louis Fed says about the latter, ‘the value implies what market participants expect inflation to be in the next 5 years, on average.’

Each value dance wonderfully together.

The better part of the chart is the lower bit where the RSI (Overbought/Oversold) indicator appears.

Whenever the 5 year breakeven inflation rate is Oversold (as this weekly chart shows), the WTI Crude Oil price finds a floor from which to advance.

We saw an Oversold 5 year b/e rate last week.

This week’s OPEC production cut announcement wasn’t a surprise because this Oversold moment in the U.S. 5 year break-even inflation rate tends to coincide with OPEC announcing production cuts.

Of course, Biden isn’t happy that OPEC have cut production.

Furthermore, Biden has virtually released all of the nation’s Special Petroleum Reserves. While he probably thinks it was his strategy sending Gasoline prices lower, when it was in fact a combination of other falling commodity prices (which is deflationary), mean reversion in the oil price and rising credit forces at work.

No to mention the importance of Biden needing lower domestic petroleum prices to aide his mid-term election hopes.

OPEC’s production cut may seem to be mathematically synchronised to the United State’s own inflation break-even rates but I think it is equally loaded with a little political payback.

Funnily, the U.S. isn’t pleased with this announcement and have passed on their views but it’s difficult to have a say into a club of which you’re not a member of.

Keep in mind, this study doesn’t assist the decision of when to sell your Oil.

So, I’ll watch for how the AUD/USD and WTI Crude symbiotically test their next respective levels of 0.6464 and $77.50, as neither ‘daily’ downtrends are confirming continuing strength.

Hint: probability is rising that we are at the tail-end (+/- 3%-6%) of the downdraft in both assets.

Here are some WTI Crude Oil trend lines I’m watching.

The downward trend remains intact, however on a daily basis it’ll need a quick drop of $2-$3 in order to add some strength to this trend, otherwise we can kiss a visit to $77.50 and any notion of ~ $65 good bye for the time being.

Should this trend wane, it will correspond with the AUD/USD and the CRB Index finding a floor.

It’s an important coming day or two in Brent Crude Oil trading.

I’m watching if it trades above $86.68.

Friday’s high was $86.52.

That means it makes a ‘higher high’ seen on October 25, 2021.

Albeit, a ‘higher high’ while also recent making a ‘lower low’ portends for an extension of the current rally, on a Daily basis, Brent is now in Overbought territory and 2 standard deviations above its mean.

Whilst the chart below is current, it has notes on it from a post on November 5th, 2021, which also shows the previous high in Brent at $86.71 from October 3, 2018.

We say ‘Don’t fight the Fed’, Perhaps Biden shouldn’t fight OPEC? What a terrible politically motivated decision especially when the SPR is normally kept for emergency supply disruptions such as in case of a hurricane etc.

And he asks or even persuades other nations to join him in their own ‘release’.

Such ad-hoc ‘band-aids’ seldom solve and this releases will be soon forgotten.

Alas, the oil price rose 3% today. Maybe short covering played a part as speculators bet on a larger dumping.

Biden just added supply this hurting his own U.S. drillers. With this type of decision, drillers are hardly about to make capex decisions to drill more.

This story also mentions how the replenishing costs may be detrimental to refiners.

Lo and behold, pending OPEC’s response in the coming months, the reflexivity of this scenario means oil prices make their way lower due to inflationary pressures crimping GDP growth.

Furthermore, Biden becoming worse at international diplomacy. His relationship with Saudi Arabia is dreadful (interesting Saudi and China) are close allies.

His relationship with Russia is awful. (And Russian troops gather around Biden’s mates in the Ukraine)

And China and Russia definantly cooperate.

To understand Oil, it’s worthy to watch how the world works.

When you’re not a member of a member based organisation, how can you expect to have your requests (demands) actioned?

Secondly, the irony of Biden asking OPEC to pump more oil (so to ease U.S. domestic gasoline prices) while he is attending COP26 in Glasgow is comical.

Thirdly, he seems to be targeting blame at the Saudi’s for not increasing their output. There are other nations which make up OPEC and OPEC+.

Biden is proving to be a poor manager of geopolitical nuances.

But there any many more angles to this story;

Imagine if the U.S. was still a net exporter of oil?

A lower oil price may make their shale market uneconomical?

The U.S. can always lift sanctions on Iranian oil, allowing it to hit the market?

p.s. In my view, the decline in Crude was expected once OPEC said they won’t be increasing output. Why? Because, we will be closer to output being increased at the next meeting……Markets price in the probability of next move quickly.