Macro Extremes (week ending December 30, 2022)

December 31, 2022 Leave a comment

A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities

The following assets (on a weekly timeframe) registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations)

Cocoa

Overbought (RSI > 70)

German 2 and 5 year government bond yields

Cattle

Istanbul’s BIST Index

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Japanese 10 year bond yield

Extremes “below” the Mean (at least 2.5 standard deviations)

U.S. 10 year bond yield minus German 10 year bond yield spread

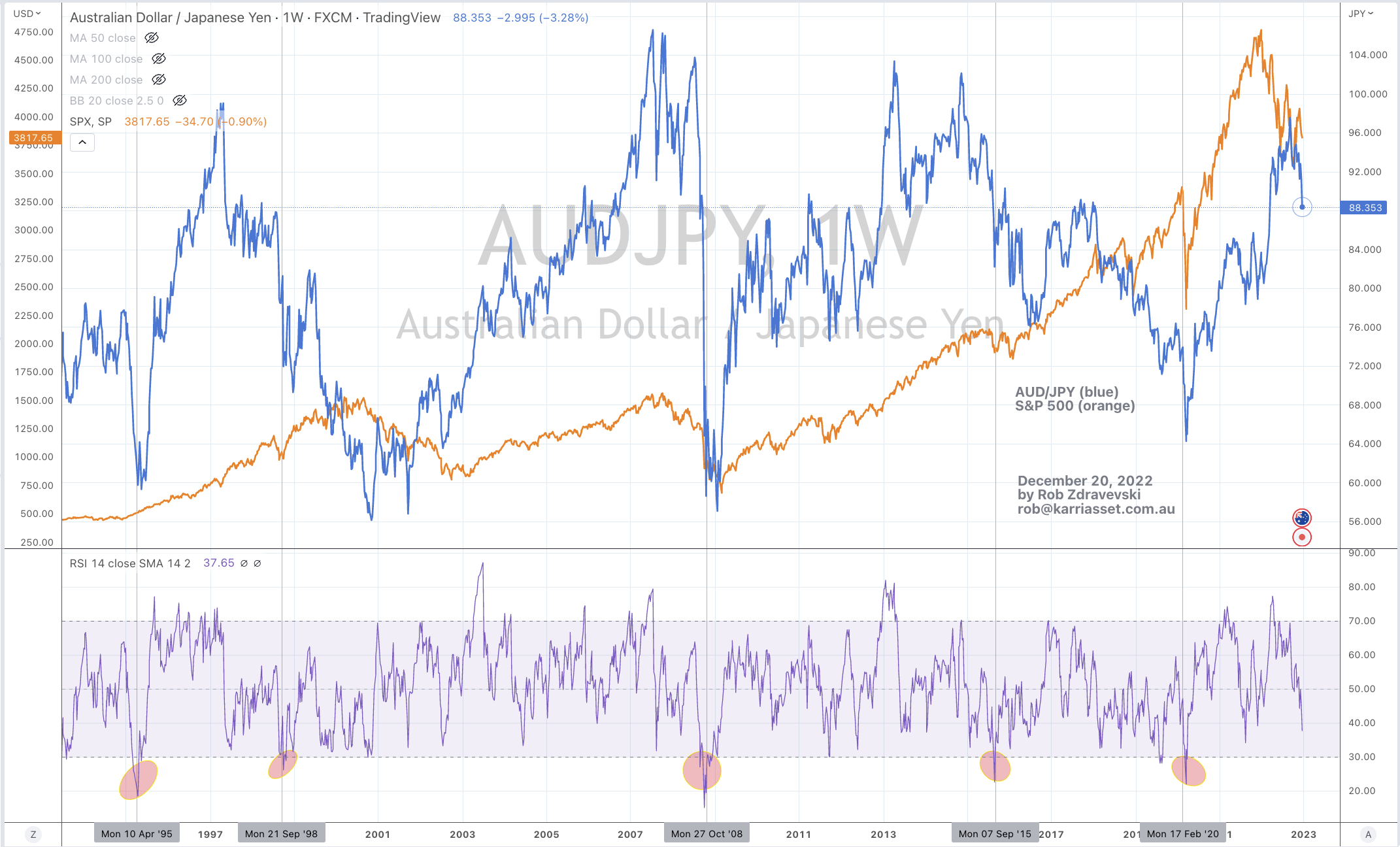

AUD/JPY

Oversold (RSI < 30)

Chilean and Turkish 10 year government bond yields

The Oversold Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

None

Notes & Ideas:

’twas the week following Christmas and equities had a benign and solemn week.

The Dow Jones Industrials, S&P MidCap 400, Nasdaq Biotech, SOX and S&P 500 all fell either 0.1% or 0.2% for the week.

Once again, Bond yields mainly rose and overall they remain notably above their 200 week moving average.

This includes the widow-maker Japanese 10 year bond yield.

Amongst currencies, the AUD/EUR jean reverted to its 200 week moving average, while generally the AUD strengthened against all FX crosses.

Last week, I highlighted that the AUD/GBP posted a bullish outside reversal week. It rose 1% this past week.

The USD continues to weaken against currencies such as the Yen, the Won and many others as it moves towards the other side of the extreme pendulum along with the gravitational pull of the 200 week moving average.

In commodities, the larger moves were seen amongst the Platinum group of metals. Readers will recall that Palladium was mentioned in the last 2 editions of ‘extremes’ as visiting the lower end of its range along with registering new 52 week lows.

Those gas prices (Henry Hub and Dutch TTF) continue to decline and mean revert. More on those later.

While the biggest news was that U.S. Midwest Hot Rolled Coil Steel rose 13% and is no longer Oversold.

The larger advancers over the past week comprised of;

Australia Coking Coal 10.2%, Hot Rolled Coil Steel 12.6%, JKM LNG 5%, Nickel 5%, Palladium 3.8%, Platinum 5.2%, Gasoline 4%, Corn 1.8%, Wheat 2.1%, KBW Banking Index 1.6% and India’s Sensex rose 1.7%.

The group of decliners included;

Rotterdam Coal (19.5%), Baltic Dry Index (2.9%), Coffee (2.7%), Natural Gas (11.9%), Sugar (4.5%), Cotton (2.2%), Dutch TTF (8%), AEX (1.7%), KOSPI (3.3%), while Australia’s ASX 200 fell 1%.

Incidentally, the ASX 200, the S&P 500 and the Nasdaq 100 & Composite have all fallen now for 4 consecutive weeks. Albeit, this past week was quiet, they have declined a respective 3.7%, 5.8%, 9.1% and 9% over the past 4 weeks.

I wish readers of my notes, a wonderful 2023.

December 31, 2022

by Rob Zdravevski

rob@karriasset.com.au