A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations)

Chinese 10 year government bond yield

Australian Coking Coal

Tin

Sugar

CSI 300

U.S. KBW Banking Index

Dow Jones Industrials

Nasdaq Composite and 100

Russell 2000

SOX

Overbought (RSI > 70)

German 2 year government bond yields

Cattle

CAC, DAX, MIB and IBEX equity indices

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

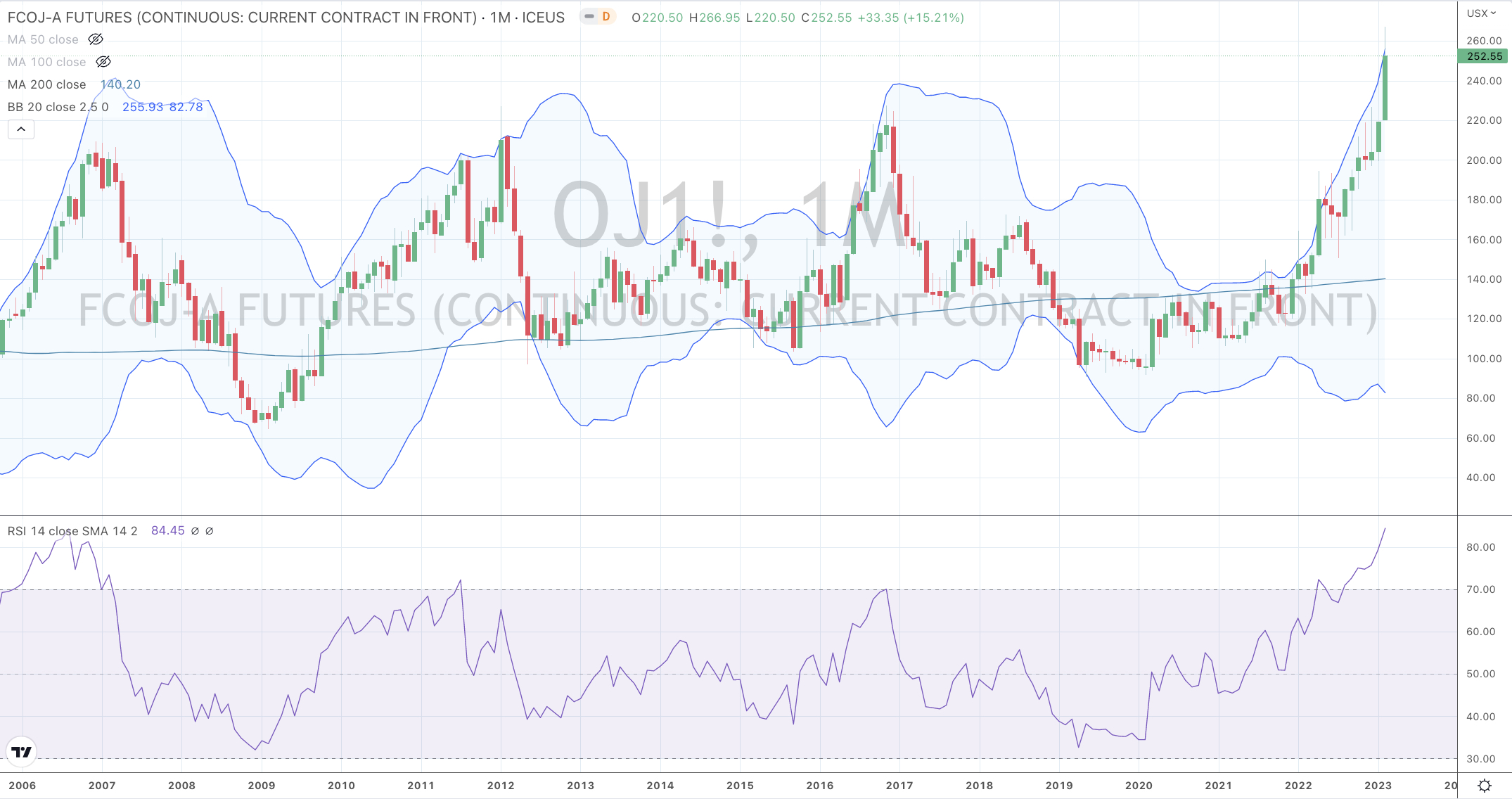

Orange Juice

Extremes “below” the Mean (at least 2.5 standard deviations)

Bloomberg Commodity Index

USD/BRL

Oversold (RSI < 30)

U.S. 5 year yield minus U.S. 3 month bill yield spread

Natural Gas

Urea (U.S. Gulf)

Urea (Middle East)

Baltic Dry Index

The Oversold Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

None

Notes & Ideas:

It’s a very interesting list of entries featured amongst the ‘extremes’.

We are seeing the return on equity indices and some commodities back into the list.

Amongst bonds, yields generally fell, especially along at the long end. It’s worth watching the bearish outside weeks that bond yields had, which adds to their case of edging lower.

Those bearish outside weeks were seen amongst Spanish, German, French, Greek, Italian, Korean and Portuguese 10’s.

While yields fell globally, that wasn’t the case in U.S. debt.

As bond yield work or meander their way lower (toward their longer term means), it would inversely suggest that ‘tech stocks’ will continue to rally.

While some ‘tech’ indices are hitting Overbought extremes this past week, keep in mind that prices often stay ‘Overbought’ for a longer time than they stay ‘Oversold’.

And for cross referencing, bond yields aren’t commensurately nor correspondingly registering Oversold readings.

Indices such as the Nasdaq 100 can do much more ‘damage’ by rallying further but don’t confuse momentum with value.

In commodities, energy prices resume/continue to fall along with precious metals. The latter would be a surprise to many.

The Japan Korea LNG Marker (JKM) touched its lowest price since September 7th, 2021.

Natural Gas saw its 7th consecutive losing week and simultaneously touched Oversold extremes…..

JKM, Platinum, Dutch TTF Gas, Brent Crude and Rotterdam delivered Coal continue to edge their way lower towards their 200 week moving average.

Shipping Rates weakened further. The Baltic Dry Index is now Oversold and has slumped 81% in the past 5 weeks.

Following this week’s declines, last week’s Overbought Gold entries are no longer so.

While Orange Juice was the massive upwards mover for the week with current prices now suggesting a Sell signal for speculators and producers.

In currencies, the AUD was down 2% against everyone, everywhere.

In equities, we mainly saw U.S. indices pop into Overbought territory with some major Europeans also mimicking.

Although it is worthy to note that the Dow Jones Industrials fell 0.2% for the week, the Nasdaq Biotech Index declined 1% while Toronto’s TSX and the ASX 200 rose 0.2% and 0.9% respectively.

And last week, I prompted thought about the odds of an extended rally in Chinese equites. This past week, Chinese equity indices were the noticeable losers.

Lastly, this past week saw ‘outside bearish reversal weeks’ in Cocoa, Silver in USD, Gold in USD and in the AUD/USD.

The larger advancers over the past week comprised of;

Australian Coking Coal 9.8%, Hot Rolled Coil Steel 2.8%, Cattle 2.3%, Orange Juice 17.5%, Dutch TTF Gas 4.4%, AEX 1.8%, KBW Banking Index 2.2%, CAC 1.9%, DAX 2.2%, DJ Transports 7.2%, MIB 2%, IBEX 1.8%, Nasdaq Composite 3.3%, S&P MidCap 400 3.4%, Nasdaq 100 3.3%, Copenhagen 4.5%, Stockholm 4.4%, Russell 2000 3.9%, Sensex 2.6%, S&P SmallCap 600 5.2%, SOX 4.7%, S&P 500 1.6%, TAIEX 4.5%, FTSE 100 1.8% and Argentina’s MERVAL rose 5.1%.

The group of decliners included;

Aluminium (3.4%), Bloomberg Commodity Index (4.1%), Baltic Dry Index (8.1%), Cocoa (2.2%), China Coal (6.4%), WTI Crude (7.9%), Gasoil (12.7%), Copper (3.9%), Heating Oil (15%), JKM LNG (5%), Tin (4.4%), Natural Gas (15.4%), Platinum (3.6%), Gasoline (10.5%), Urea U.S. Gulf (4.1%), Brent Crude (7.3%), Silver AUD (2.7%), Silver (5.3%), Gold (3.2%), Gold in CAD (2.6%), Rice (3.1%), AUD/USD (2.6%), HSCEI (5%), HSI (4.5%), BOVESPA (3.4%) and Istanbul’s BIST fell 3.7%.

February 5, 2023

by Rob Zdravevski

rob@karriasset.com.au