Macro Extremes (week ending December 8, 2023)

December 10, 2023 Leave a comment

A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) either registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations

SHY – 1-3 year Treasury ETF

Baltic Dry Index

Coffee

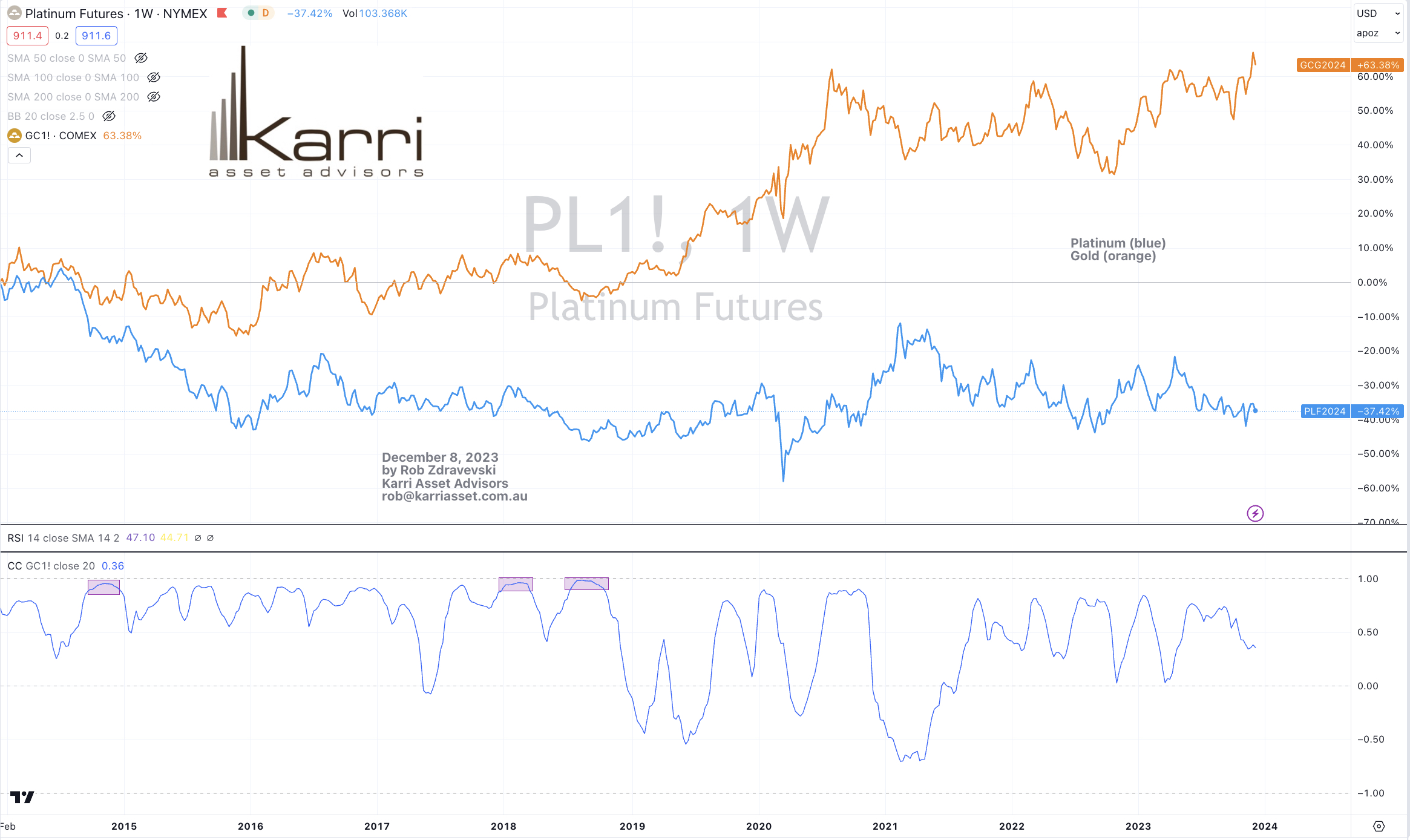

Silver

Gold

IBEX

Overbought (RSI > 70)

Cocoa

Iron Ore

Uranium

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

U.S. Midwest Hot Rolled Coil Steel

India’s NIFTY and SENSEX equity indices

Extremes “below” the Mean (at least 2.5 standard deviations)

German and U.S. 2 year government bond yields

German 5 year government bond yield

British, French, Greek, German, Spanish, Swiss and Portuguese 10 year government bond yields

U.S. 10 year break-even inflation yield rate

Bloomberg Commodity Index

S&P Goldman Sachs Commodity Index

Thomson Reuters CRB Index

Cattle

Natural Gas

Brent Crude Oil

EUR/JPY

GBP/JPY

Oversold (RSI < 30)

Chilean 2 year government bond yield

Lithium Hydroxide

Palladium

CSI 300 Index

The Oversold Quinella – Both Oversold and Traded at < 2.5 standard deviations below the weekly mean)

JKM LNG

Notes & Ideas:

Government bond yields again fell everywhere, with the exception of British 2’s and 3’s, Japanese bond yields and U.S. ‘shorter’ duration collection of the 2’s, 5’s, 7’s and 10’s.

The U.S. 20’s and 30 year bond yields fell. Not long ago, the consensus called yields ‘higher for longer’ but only when they reached the 5% level.

You kinda wish they could make that call when yields were marching higher through the 2% mark.

The TLT (20+ year) ETF stock price has risen 13.4% over the past 7 weeks. Prior to this advance, that ETF appeared as an ‘oversold extreme’.

The BoA 5-7 year corporate bond yield is hovering at the same yield as July 24, 2023.

The Canadian 10’s are yield at their lowest level since July 10, 2023, British 10’s are back to May 2022 levels and German 10’s are at their lowest since April 10, 2023.

Japanese 10’s had a bullish outside reversal week.

Chilean 2 year yields have fallen for 6 consecutive weeks, while South Korean 10’s have declined for 7 straight weeks.

Equities were mainly higher for the week extending most gains from the preceding 2 weeks.

Most indices end the week with return of between 1% – 1.6%.

U.S. Banks had another big week.

The KRE Regional Banks index has risen 23% over the last 6 weeks.

Chinese indices dominated the losers for the week, again with the CSI 300 appearing in this week’s oversold list and now at the same price as seen in February 11, 2019.

The Hang Seng is at its lowest price since July 10, 2023

Germany’s DAX is at an all-time high but not yet overbought.

The following indices have risen for 6 consecutive weeks; AEX, DAX, DJ Industrials, Nasdaq Composite and Nasdaq 100, KOSPI, Sensex, Copenhagen and the S&P 500

India’s SENSEX seems to be amongst the most extended of bourses, as it trades at 31% above its 200 week moving average.

Brazil’s BOVESPA broke its 6 winning streak while the TAEIX’s 5 consecutive weeks of advance came to an end.

And Mexico’s IPC Index extends its weekly winning streak to 7.

Commodities were mostly lower. The major losers over the week are listed below.

Coal, Steel, Tin, Cocoa and Wheat were the few which rose.

In fact, Newcastle Coal has risen 18% in the past fortnight.

U.S. MidWest Hot Rolled Coil Steel added to recent gains.

The Baltic Dry Index took a breather from its massive rally.

During its 7 week losing streak, WTI Crude Oil has sunken 19%.

Brent Crude reached an oversold extreme this week for the first time since March 2023.

Heating Oil has declined 6.5% in the past 2 weeks.

Dutch TTF Gas has fallen 32% over the past 6 weeks.

Natural Gas has slumped 30% over the past 5 weeks.

This week, the broader commodity indices reached an oversold extreme.

And relatively versus equities they are too.

Gold eased following last week’s media and LinkedIn hype

Silver, dramatically more so.

Following last week’s registration of an overbought extreme, Gold in USD fell 3.3% for the week. Silver as priced in USD tanked 10%. Not exactly the attributes of something being a store of value.

Mean reversing beckons for some commodity prices.

Orange Juice has fallen 10% in the past 2 weeks.

Uranium remains overbought for a 17th consecutive week.

Lithium Hydroxide prices are now oversold for 22 consecutive weeks.

Iron Ore broke its 7 winning streak as it fell 0.2% for the week.

While Cocoa has locked in weekly gains in 9 of its past 10, rising 25% over that time.

Amongst currencies, the Australian Dollar lower, taking a break from recent advances.

The Loonie was mostly higher against its pairs, the Euro was mixed and the GBP was weaker.

The USD was former everywhere except against the Yen,

Because the Japanese Yen rose strongly against all others.

#riskoff

The larger advancers over the past week comprised of;

Rotterdam Coal 2.7%, Cocoa 1.7%, Cotton 2.5%, HRC 4.1%, Tin 2.2%, Newcastle Coal 14.2%, Rubber 2.1%, Wheat 4.8%, DAX 2.2%, KRE Regional Bank Index 3.2%, FTSE 260 1.6%, NIFTY 3.5%, Stockholm 2.8%, SENSEX 3%, SMI 1.7%, ASX Materials 2% and the ASX 200 rose 1.7%.

For some other comparisons for the week, , the S&P Small Cap 600 advanced 1.3%, Russell 2000 climbed 1%, Nasdaq Composite rose 0.7% and S&P 500 closed 0.2% higher.

The group of decliners included;

Aluminium (3%), Bloomberg Commodity Index (3.6%), Baltic Dry Index (21.9%), WTI Crude (4.2%), Copper (2.2%), Heating Oil (3.2%), JKM LNG (1.7%), Coffee (3.9%), Cattle (2.3%), Lithium (4.9%), Natural Gas (8.3%), Nickel (1.6%), Orange Juice (5.8%), Palladium (5.8%), Platinum (1.7%), Gasoline (3.4%), Sugar (6.9%), SPGSCI (3.1%), CRB (2.9%), Dutch TTF Gas (11.3%), Brent Crude (4.1%), Gasoil (4%), Silver in AUD 8.3%), Silver in USD (9.7%), Gold in AUD (1.8%), Gold in CAD (2.6%), Gold in USD (3.3%), Oats (7.6%), Soybeans (1.6%), Shanghai (2.2%), CSI 300 (2.4%), China A50 (2.7%), DJ Transports (1.6%), HSCEI (2.8%), Hang Seng (3%) and the Nikkei 225 fell 3.4%

December 10, 2023

by Rob Zdravevski

rob@karriasset.com.au